I’m tracking a growing Google Business Profile issue after several days of complaints from businesses that say reviews have disappeared from their local listings. Google has now confirmed that it is investigating the reports, and in some cases, review submissions on affected profiles appear to be paused.

What Google said. Google told us that when its systems detect suspicious review activity, it may take several actions, including removing reviews and temporarily pausing reviews on a profile to prevent further abuse. Google also said it is investigating the issue and will restore any reviews that were incorrectly removed.

What I’m seeing. As I documented on the Search Engine Roundtable, there are dozens of complaints in the Google Business Profile Forums from business owners and local SEOs who say their reviews have mysteriously vanished. In some cases, businesses are also unable to receive new reviews on their local listings.

From what I can tell, Google’s review spam detection systems may be identifying certain patterns and aggressively removing or blocking reviews on suspected Google Business Profiles. What remains unclear is whether this is tied to spammers abusing some profiles, a recent algorithmic adjustment, or Google’s systems becoming overly sensitive.

More details. Amy Toman, a volunteer Google Product Expert for Google Business Profiles, shared on LinkedIn that businesses or clients affected by this issue can post in the forum if they want to, but Google is already aware of the problem and working on it. She also noted that no timeline for a resolution has been provided yet.

She said she is seeing a new pattern where, after fake or spam reviews are reported, some Google listings receive a review block and all reviews are hidden. In at least one case, she said the rating was reduced to 0.

Why I care. If I noticed a sudden drop in reviews or stopped receiving new reviews this week, I would consider this issue a likely explanation. For local businesses, reviews can directly affect trust, visibility, and customer decisions, so even a temporary review disruption can be frustrating.

Google is investigating, and I’m watching to see whether missing reviews are restored and whether affected Google Business Profiles can begin receiving new reviews again.

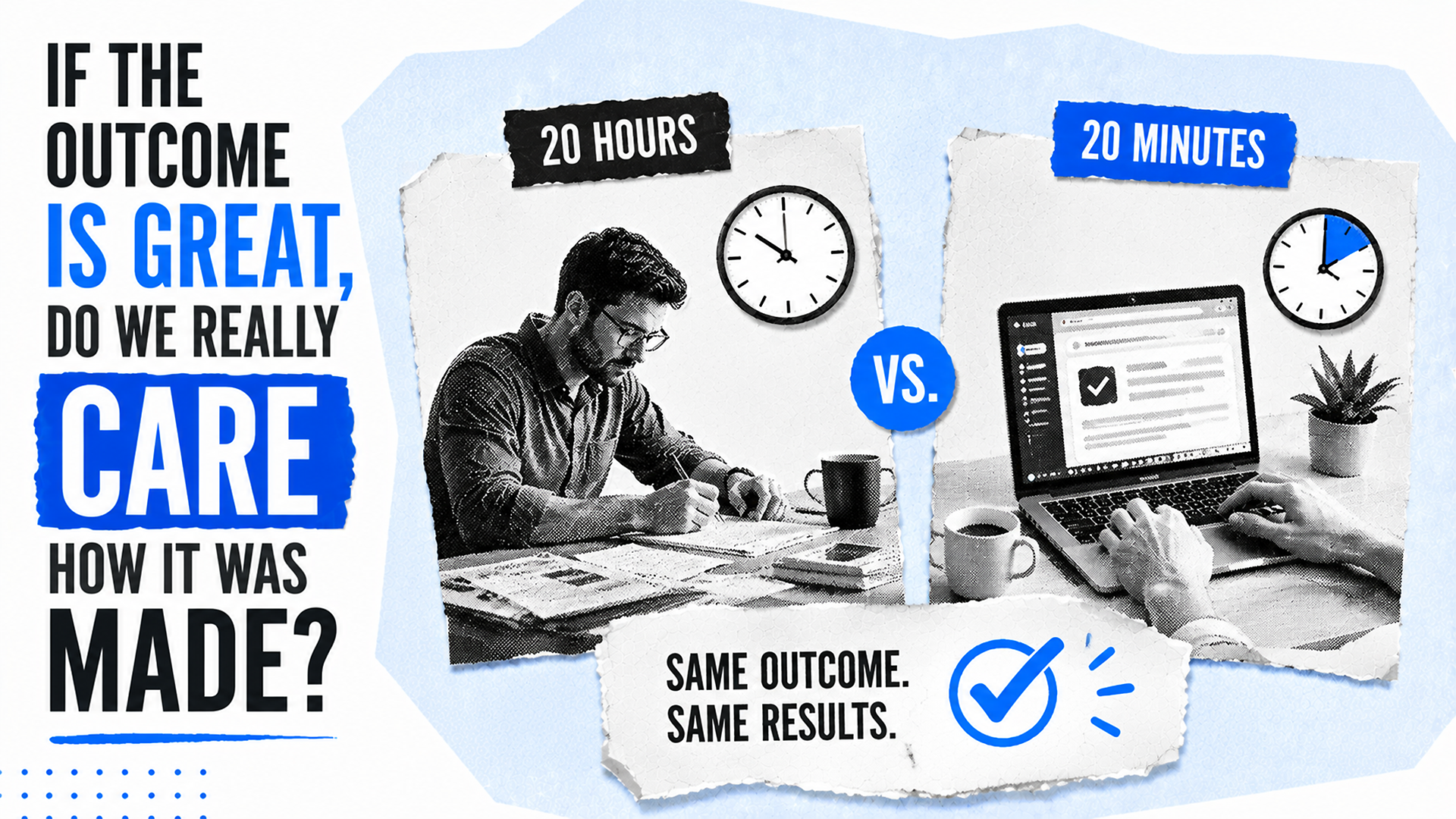

When I think about AI deliverables, I keep coming back to a simple scenario: a client receives two pieces of work.

Both deliverables solve the problem they were hired to solve. Both are accurate, useful, and tied to the same business outcome. The client is happy, and from the outside, there is no meaningful difference in the results.

Then the client learns that one took 20 hours to create, while the other took 20 minutes. That is when the uncomfortable questions begin.

Was AI involved? Should the faster deliverable cost less? Is the person who completed it less skilled because they found a faster, more efficient way to reach the same result?

What I find most interesting is how differently many of us react to AI depending on which side of the transaction we are on. I love using AI when it saves me time, but I also understand why customers can feel uneasy when they discover AI helped create something they paid for.

I recently ran a LinkedIn poll asking a simple question: if the outcome is great, do we really care how it was made?

The responses reinforced something I have been thinking about for a while. Many of the strongest objections people have to AI are not really about quality at all.

The Time vs. Value Fallacy

I think part of the discomfort comes from the fact that we have spent decades tying value to effort.

Long hours feel valuable. Fast work feels suspicious. Struggle often gets mistaken for expertise.

The harder something appears to be, the easier it becomes to justify the price attached to it.

There is an old story about a ship engine that stopped working. After multiple failed attempts to repair it, the owners brought in an engineer with decades of experience. He inspected the engine, tapped it once with a small hammer, and the machine roared back to life.

His invoice was $10,000.

The owners were furious and demanded an itemized bill. The response was simple: hammer tap, $2. Knowing where to tap, $9,998.

People debate whether that story is true or just a useful tale for people like me who believe in value-based pricing. But whether it really happened almost does not matter. The lesson still holds.

People are not paying for the tap. They are paying for the expertise behind it.

That is what makes AI such an important topic for me. It forces us to confront a question many of us have avoided for years: are we paying for expertise, or are we paying for visible effort?

Those are not always the same thing.

The Objections That Actually Matter

To be clear, I do not think every objection to AI is unreasonable. I have shared plenty of my own concerns, and some of them are serious.

In fact, I think the strongest arguments against AI have very little to do with how quickly something was created.

Those are legitimate concerns. What stands out to me is that none of them has much to do with how long it took to create the deliverable.

They are questions of trust.

Can the output be trusted? Can the recommendation be defended? Can someone confidently stand behind the work if it is questioned six months from now?

Because when something goes wrong, nobody gets to blame the AI. The employee is accountable. The consultant is accountable. The company is accountable.

That is why I have always found the quality debate to be the least interesting part of the conversation. The more important question is not whether AI was involved. It is whether the outcome is trustworthy enough for someone to put their name behind it.

The Outcome Test

The more I think about AI, the less interested I become in whether it was used.

Instead, I find myself asking a different set of questions. Was the outcome accurate? Was it useful? Was it better than the alternative? Would I be willing to stand behind it with my name, reputation, and credentials on the line?

If the answer to all of those questions is yes, then I have a hard time arguing that the production method matters more than the result.

Ironically, this is also where humans become more important, not less.

The future is not machines versus humans. I know, "The Terminator" and "I, Robot" movies will never feel the same. The real shift is humans using AI versus humans who refuse to adapt.

AI can accelerate execution, but people still decide what should be built, what should be published, and what risks are acceptable. More importantly, people are still responsible for the outcome.

The people who lose to AI will not be the ones using it. They will be the ones still evaluating effort while everyone else is measuring outcomes.

This post first appeared on the author’s website and is republished here with permission.

I do not see search demand disappearing. I see it moving. In this analysis, 29% of high-volume search demand is declining, while nearly the same amount is growing somewhere else. Overall demand is essentially flat because people are redistributing how and where they search instead of abandoning search altogether.

That changes how I think about SEO strategy. I would not start by panicking over shrinking keywords. I would start by identifying which queries are losing volume, which ones are gaining momentum, and where a brand can build enough authority to appear in both traditional search results and AI-generated answers.

This study looks at where search demand is shifting, which industries are seeing the sharpest changes, and what those patterns mean for SEO teams trying to adapt to AI-driven discovery.

How I studied AI’s impact on search

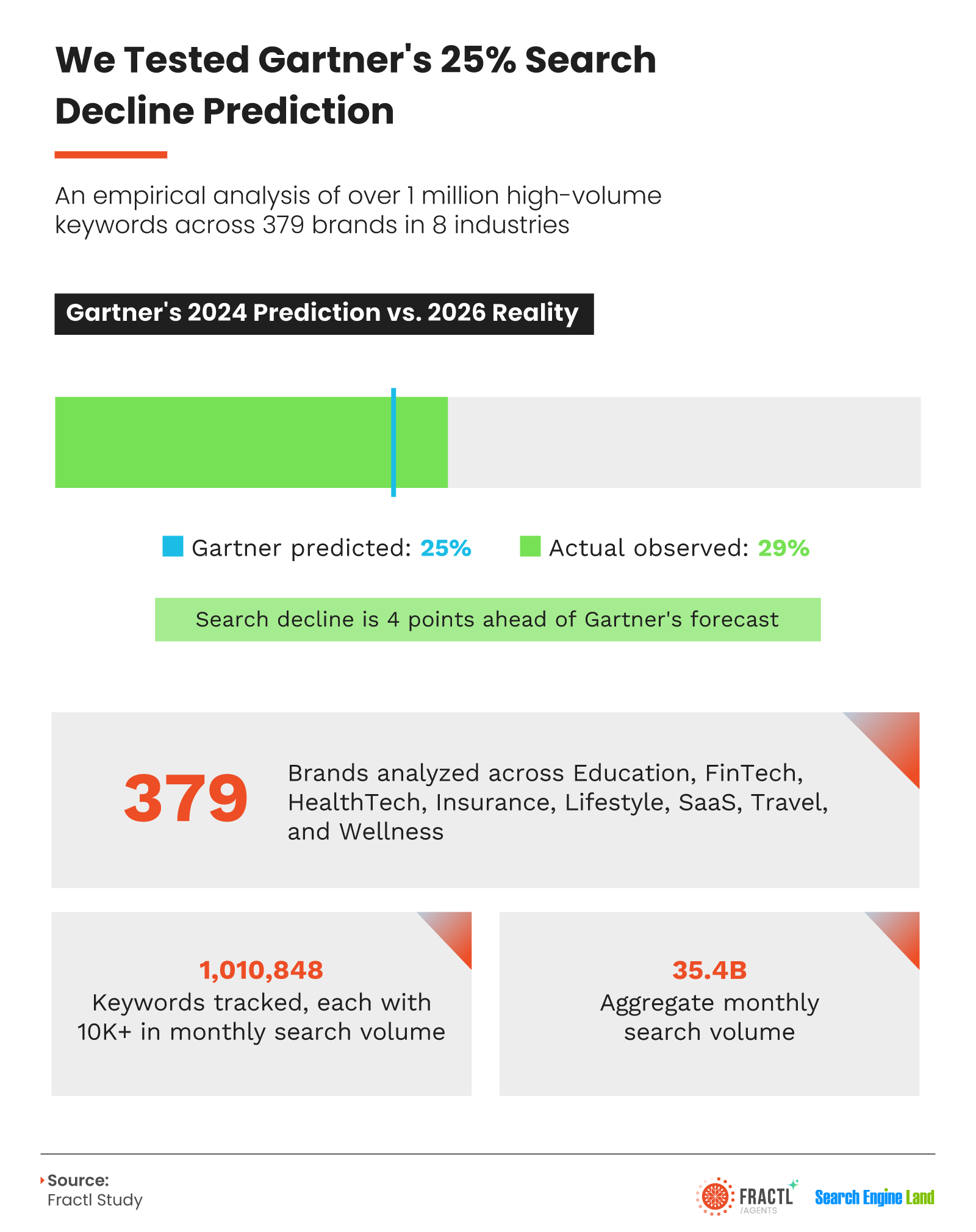

In 2024, Gartner predicted that traditional search engine volume would fall 25% by 2026 as consumers shifted to AI chatbots and virtual agents. Fractl and Search Engine Land set out to test that prediction. (Disclosure: I’m the co-founder of Fractl.)

I worked from Semrush data covering 1,010,848 high-volume keywords, each with at least 10,000 monthly searches, across 379 brands in eight verticals. I also looked at survey responses from 1,004 U.S. consumers to better understand how AI is changing the way people search.

The analysis measured which keywords gained or lost search volume over the past year, how those shifts differed by industry, and how consumer behavior is evolving as AI tools become part of everyday discovery.

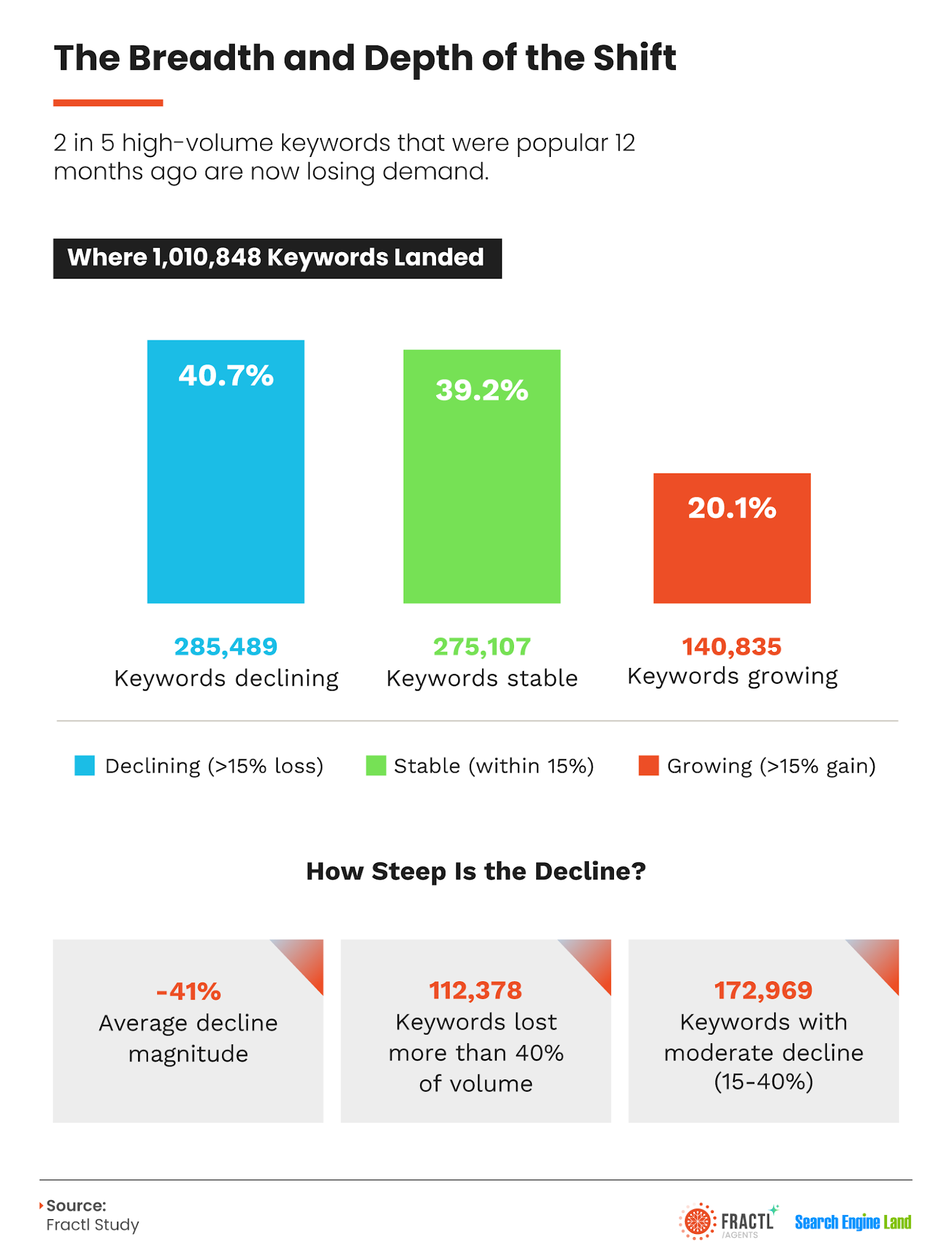

The 29% search decline is real, but it depends on the vertical

Across more than 1 million high-volume keywords, I found that 29% of search volume is in measurable decline. That is 4 percentage points above Gartner’s forecast. In a dataset representing 35.4 billion monthly searches, that difference represents a meaningful amount of search activity.

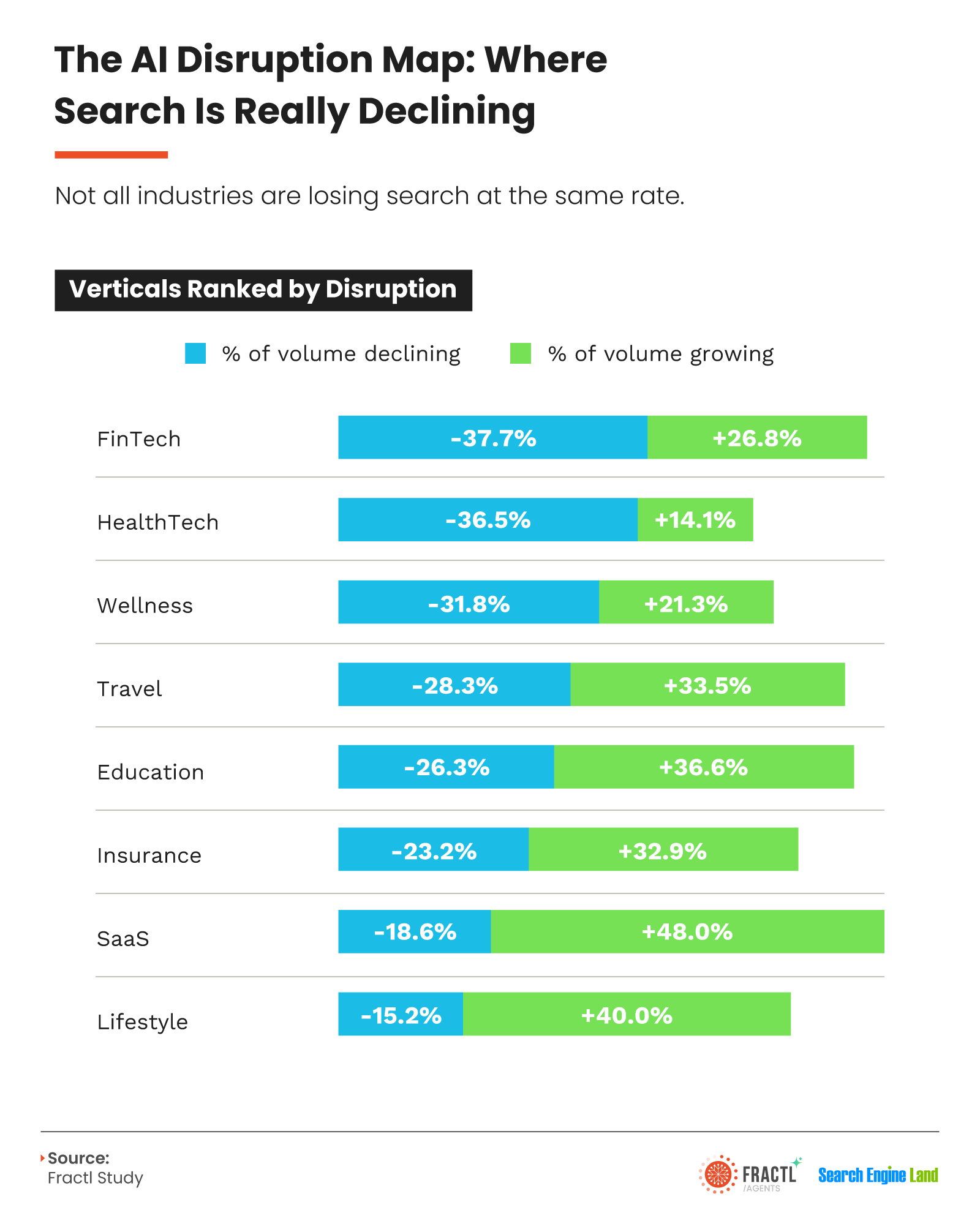

The impact is not evenly distributed. FinTech showed the largest decline at -37.7%, while Lifestyle saw the smallest decline at -15.2%. Only three of the eight verticals, Insurance, SaaS, and Lifestyle, came in below Gartner’s 25% threshold. FinTech, HealthTech, and Wellness were well above it.

The pattern makes sense when I look at how information-heavy each category is. When a chatbot can answer the question completely, such as summarizing drug interactions, explaining deductibles, or giving a quick overview of a fund, search volume is more likely to fall. When people need to compare prices, complete a transaction, or navigate to a specific site, search demand tends to hold up better.

That is why transactional verticals such as SaaS, Lifestyle, Insurance, and Travel are growing or staying close to flat. Information-heavy verticals such as HealthTech, FinTech, and Wellness are seeing the largest declines.

Before reacting to broad claims about AI-driven search decline, I would benchmark these findings against the specific vertical in question. HealthTech and FinTech teams should expect more exposure than the overall 29% decline suggests. SaaS and Lifestyle teams have more reason to challenge the idea that search demand is simply collapsing.

Search demand is being redistributed

The headline number gets attention, but the offset is just as important. Demand did not vanish. It moved to a different set of words, and those are the terms I would want to understand first.

Among the high-volume keywords tracked, 40.7% are in measurable decline, meaning they lost more than 15% of their volume over the past year. Within that group, the average decline is -41%, and 112,378 keywords lost more than 40% of their volume. For brands that depend on those terms, the impact is significant.

At the same time, 20.1% of keywords are growing by more than 15%. When I add up the volume on both sides, the decline and growth almost cancel each other out.

The 285,489 declining keywords represent roughly 10.29 billion monthly searches. The 140,835 growing keywords represent roughly 10.31 billion monthly searches. Across the entire dataset, the net change is +16.8 million searches per month.

Fewer keywords are growing than declining, but the growing keywords carry more volume each. That is why the totals balance out. In practical terms, I see demand relocating more than shrinking.

The vertical-level growth-to-decline ratios show where that new demand is landing. Lifestyle leads at 2.6x, with 40% of keywords growing versus 15% declining. SaaS follows closely at 2.5x, with 48% growing versus 19% declining. HealthTech sits at the other end with an inverted ratio of 0.4x, making it the most disrupted vertical in the set.

The first audit I would run is simple: pull the tracked keyword set, filter it by year-over-year volume change, and see which side of the ledger the portfolio sits on.

Non-branded queries are the most vulnerable

I see non-branded queries as the easiest ones for AI chatbots to replace. When a search term does not include a brand name, the user is not necessarily trying to reach a specific site or source. The full exchange can happen inside the chat window.

Across the dataset, 90% of all tracked search volume is non-branded. HealthTech, at 99.6%, and Wellness, at 98.5%, are the most exposed. Insurance, at 73.8%, and SaaS, at 82.0%, are less exposed, and both are growing overall. SaaS volume is up 48% year over year, while Lifestyle is up 40%.

If I wanted to identify the content most at risk, I would start with keyword patterns. They offer one of the clearest signals in the study.

The reason SaaS and Lifestyle can be heavily touched by AI and still grow comes down to what happens after the AI answer. If AI recommends a project management platform or a couch, many people still search for the specific brand, retailer, review, or product page before buying. The AI answer creates a downstream search.

HealthTech and FinTech often behave differently. A drug-interaction question or a “what is a deductible” query can be answered completely inside the chat window. There may be no next step that sends the user back to Google.

If a category produces complete AI answers with no natural next click, I would treat AI visibility as a core strategy, not an SEO side project. In those cases, showing up in the answer may be the entire opportunity.

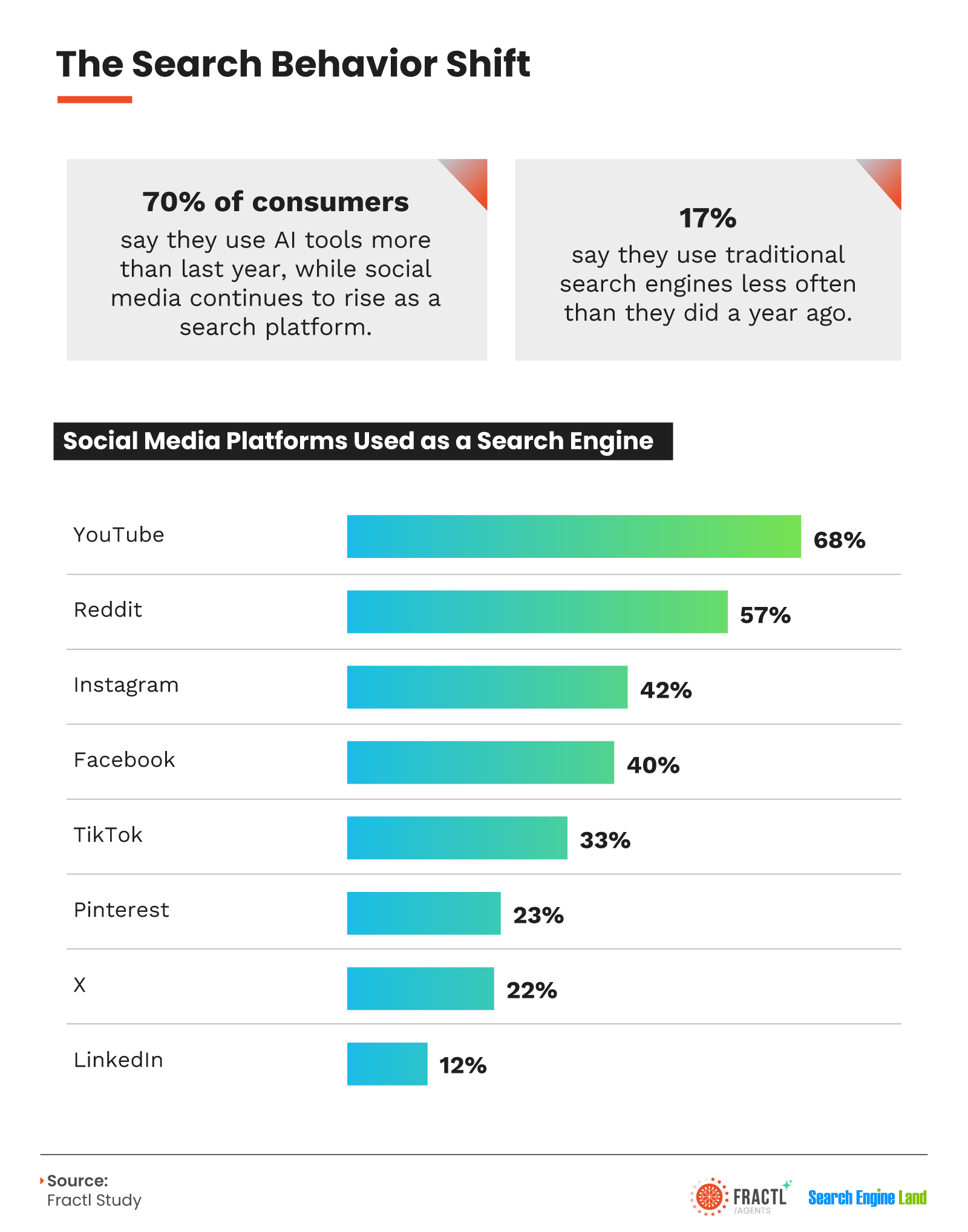

70% of consumers use AI more, but only 17% use search less

The keyword data shows what is happening in the index. The survey data shows what is happening in the minds of the people doing the searching.

Search behavior is spreading across more platforms. Many people are adding AI to their routines without giving up Google.

Social platforms are also acting like search engines in a way they did not a few years ago. YouTube leads at 68%, followed by Reddit at 57%, Instagram at 42%, Facebook at 40%, and TikTok at 33%.

If I had not already prioritized YouTube and Reddit, I would move them up the list. Both rank ahead of TikTok, Instagram, and Facebook as search destinations, and both can also surface in Google results, which gives visibility there a compounding effect.

What has actually moved from Google to AI

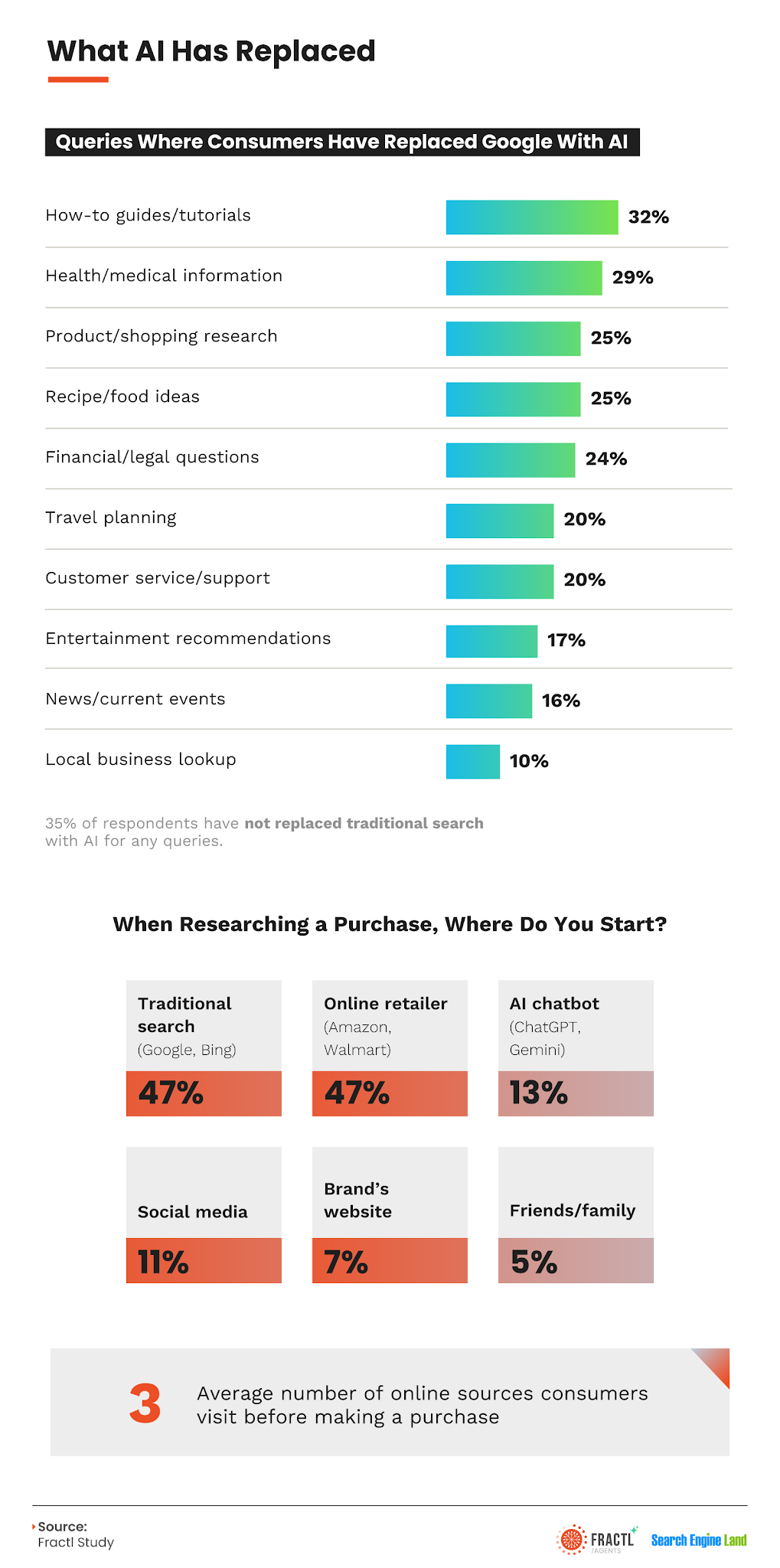

More than a third of respondents, 35%, say they have not replaced traditional search with AI for anything yet. Among those who have, how-to guides and tutorials have taken the biggest hit.

For purchase research, 47% of consumers start with a traditional search engine, tied with online retailers at 47%. Only 13% start with an AI chatbot, and shoppers check an average of three online sources before making a purchase.

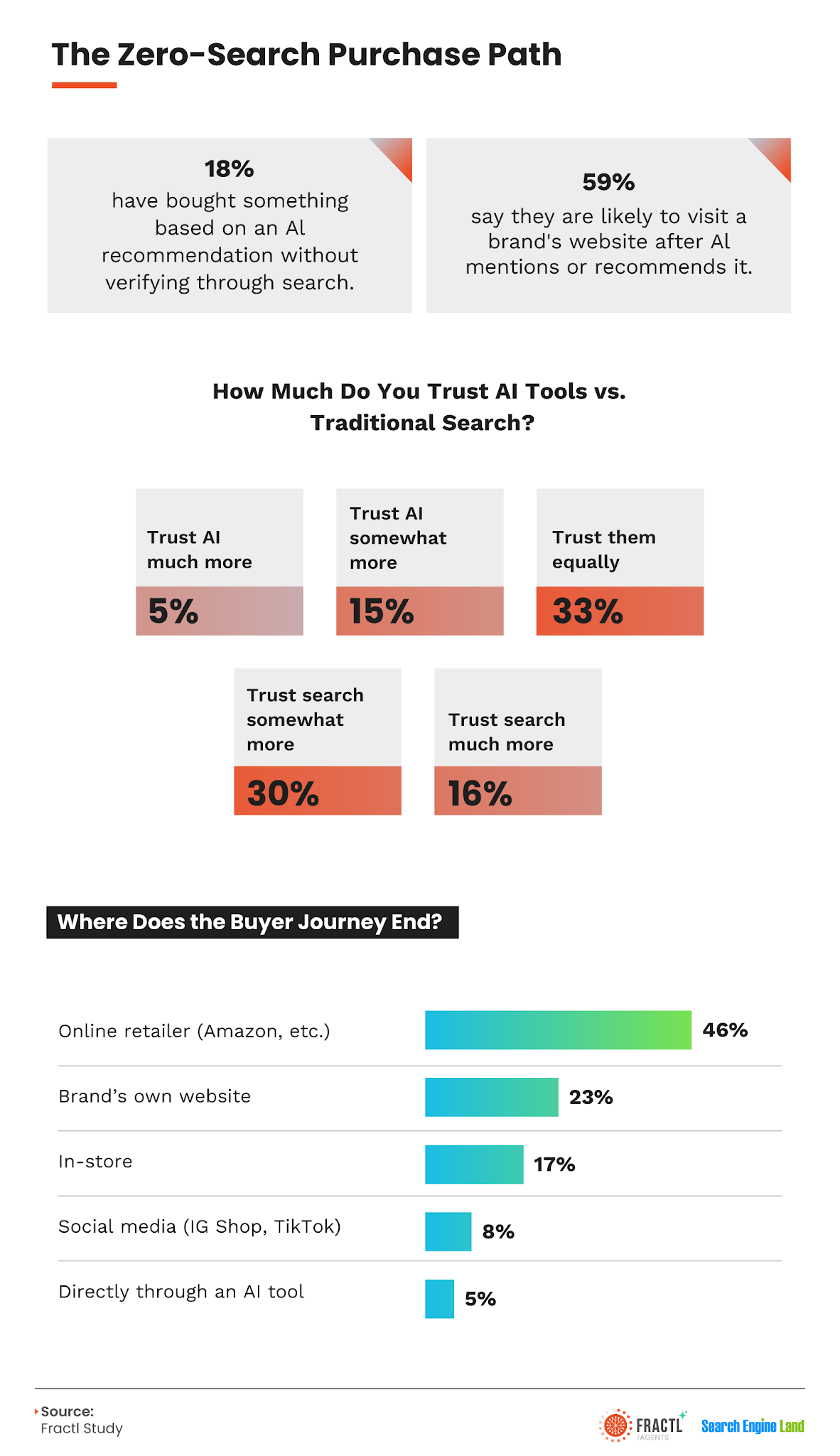

The number I would bring to a strategy meeting is this: nearly one in five consumers, 18%, have bought something based on an AI recommendation without checking it against a separate search.

That creates a different kind of buyer journey. In that path, the brand may never receive a search-driven touchpoint. To be considered, the brand has to be one of the names the chatbot returns.

Gen Z and millennials are 2.5x more likely than baby boomers to buy based on an unverified AI recommendation, at 20% versus 7%. Across all consumers, 59% say they are likely to visit a brand’s website after an AI chatbot mentions or recommends it.

That is the emerging conversion funnel I am watching closely. Brand mentions in AI answers are starting to function like rankings. Visits to a brand’s website after an AI mention are starting to look like the new click-throughs.

Trust is still mixed. In the survey, 33% of consumers trust AI and traditional search equally, 46% trust search more, and 20% trust AI more.

More than half of consumers, 56%, are at least somewhat skeptical of AI product recommendations. I read that as a sign that people are willing to let AI filter and shortlist options, but many still want to verify before they buy.

The 5-year outlook: Google is not going away, but the shift matters

When asked whether Google will still be their primary search tool in five years, 52% of consumers say yes, including 17% who say definitely and 35% who say probably. Another 27% are unsure, while 20% say probably or definitely not.

The top reasons people prefer AI over traditional search are better summaries across sources, at 21%; faster and more direct answers, at 20%; and the ability to ask conversational follow-up questions, at 19%. More personalized results and avoiding website click-throughs were much lower, at 6% and 4%.

When asked what would bring them back to traditional search, the top answer was AI giving unreliable answers, at 35%. That means much of this shift depends on whether AI maintains trust as adoption scales. More accurate search results followed at 29%, then a preference for multiple source links at 22%, and privacy concerns at 20%.

The 20% who expect to leave Google are not the majority, but I would not dismiss them. A strategy does not need to be rebuilt entirely around them today, but brands do need to appear where those users are already moving.

What this means for content and SEO strategy

I see Gartner’s 25% prediction as a useful directional warning. The real shift may be steeper, but calling it only a decline misses the more important story. Total search volume is basically flat. What has changed is which searches carry the demand.

AI visibility is not just a threat to manage. I see it as a distribution channel. With 59% of consumers saying they are likely to visit a brand’s website after an AI mention, GEO has become a meaningful part of brand discovery.

Earned media, credible third-party coverage, and strong entity signals all help brands appear in chatbot answers. That is why digital PR and GEO are becoming more closely connected.

Search is moving, not disappearing.

The brands that lose will be the ones still optimizing mainly for queries that AI now answers better. The brands that win will be the ones building enough authority to become the answer, whether that answer appears in Google or inside a chatbot.

Methodology

This study combined two data sources to test Gartner’s 2024 prediction that traditional search engine volume would fall 25% by 2026.

Fractl and Search Engine Land analyzed Semrush search volume data for 1,010,848 high-volume keywords with 10,000 or more monthly searches each, covering 379 brands across eight verticals: FinTech, HealthTech, Wellness, Travel, Education, Insurance, SaaS, and Lifestyle. The dataset represented 35.4 billion in aggregate monthly search volume. Keyword-level year-over-year volume change was measured as of April 2026 and classified as declining, meaning more than 15% loss; stable, meaning within 15%; or growing, meaning more than 15% gain. Query pattern groupings, including “What is X,” “Best X for Y,” “X vs. Y,” and “How to X,” were applied at the keyword level.

Fractl and Search Engine Land also surveyed 1,004 U.S. consumers about their search habits, AI tool adoption, and purchase research behavior. The sample was 52% women, 46% men, and 1% nonbinary, with 49% millennials, 26% Gen X, 16% Gen Z, and 9% boomers. The median respondent age was 41, with a range of 18 to 82.

SMX Next returns online Nov. 18, and I’m excited to help shape a program focused on today’s complex search landscape and the tactics that will define success in 2027 and beyond.

Search marketing isn’t just changing. From my perspective, it has become an entirely new kind of challenge, and that is exactly why fresh voices and practical expertise matter so much right now.

In SEO, I’m seeing the field shift toward AI Overviews, search everywhere optimization, and the rise of autonomous AI agents that browse on behalf of users. Trustworthiness, digital authority, and precise alignment with user intent are no longer nice-to-have ideas. They are becoming essential.

On the PPC side, generative AI and deep automation are creating new levels of personalization. At the same time, they are raising urgent questions for marketers: How do we keep strategic control, protect data privacy, and avoid wasted spend?

If you’re an enthusiastic search marketer with a passion for sharing what you know, I hope you’ll consider submitting a session pitch for SMX Next. I’m looking for subject matter experts who can share insights, strategies, and tactics that help SEO and PPC marketers thrive in 2027.

Whether you’ve been speaking for years or you’re a practitioner ready to share something new you’ve developed, I want to hear from you. I’m especially interested in new speakers with diverse points of view and real-world experience.

The deadline for SMX Next pitches is Aug. 7.

When I review session proposals, I’m looking for ideas that feel original, specific, and useful. Advanced, forward-thinking topics or unique frameworks that aren’t already common at other search events will stand out.

I also want to see actionability. Be clear about what attendees will be able to do better, faster, or differently after your session.

Bring the data whenever you can. A case study, concrete example, or tested approach makes your pitch stronger, especially when you explain how the lesson can scale across different types of organizations.

Keep the scope focused. A 30-minute session works best when it goes deep on a narrow or specialized topic instead of trying to cover too much at once.

Most importantly, give attendees something tangible to take with them. I’m looking for sessions that leave people with a clear action plan, framework, or process they can put to work right away.

Visit this page for more details on how to submit a session idea, or go directly to this page to create your profile and submit your pitch.

If you have questions, feel free to contact me directly at kathy.bushman@semrush.com. I’m looking forward to reading your proposals!

When I want a page to feel genuinely original, I start with original numbers. They are still one of the most reliable ways to make content stand apart, especially when those numbers come from the business itself instead of a one-off study created just to fill a content calendar.

The old approach was to pay a PR or research firm for a loosely related survey, like a car insurance FinTech commissioning road-trip research to earn a mention in Yahoo. I see that play as increasingly outdated. Almost every product now creates data worth publishing, and extracting that data is easier than it has ever been.

I do not need a full research department to compete here. The bar for standing out is lower than many teams assume.

First-party data: The strongest correlation of originality

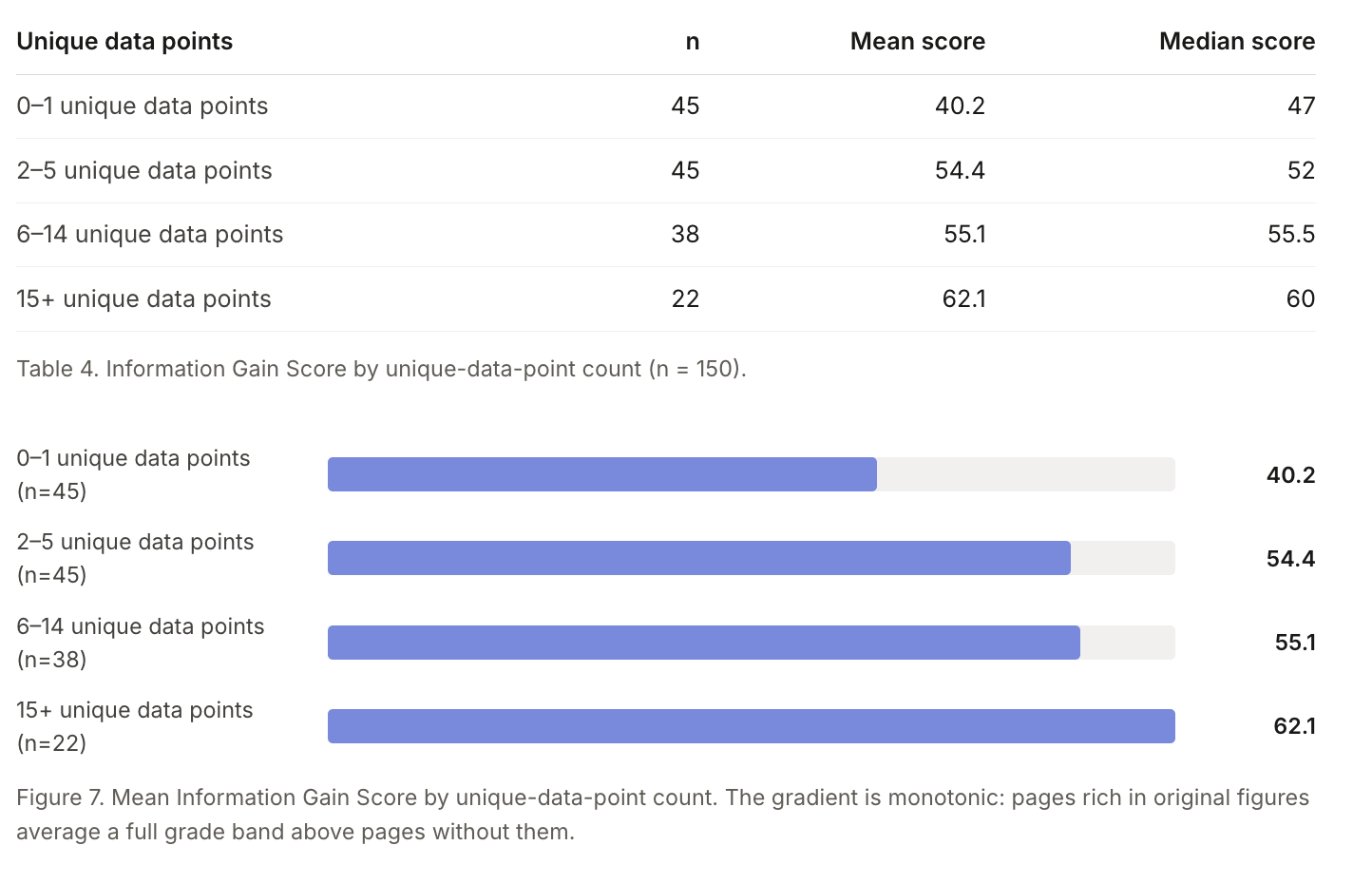

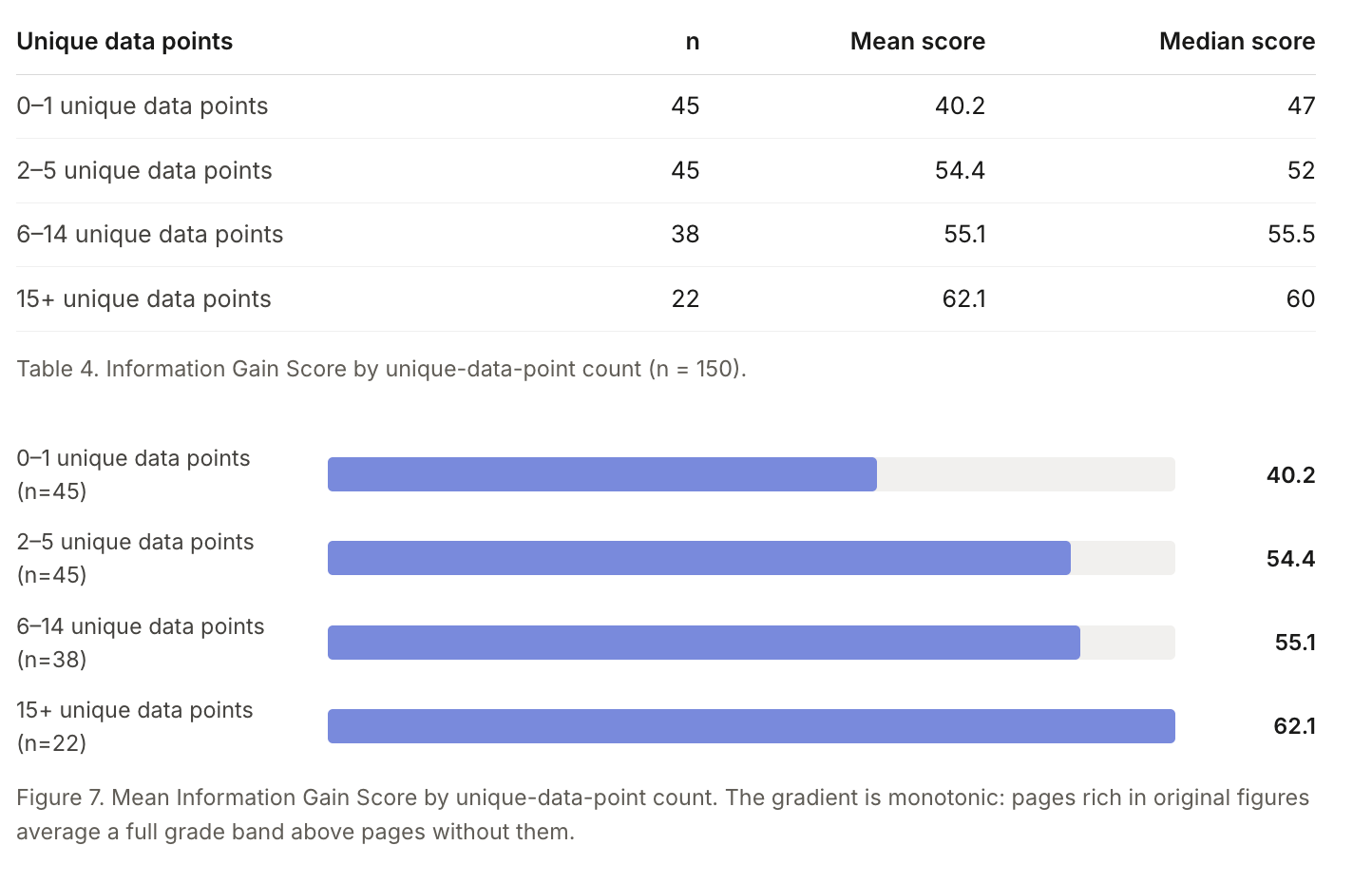

On-Page.ai’s recent information gain study scored 150 top-3 Google pages across 50 keywords and 10 verticals. The study looked at how much each page added beyond the rest of its ranking cohort, grading contribution from 0 to 100 by meaning rather than wording.

The median page scored 52. More importantly, original data correlated with that score more strongly than any other page-level trait, including content length.

Pages with at most 1 unique figure averaged an information gain score of 40.2. Pages with 15 or more unique figures averaged 62.1, and the score increased steadily at every step in between.

The good news is that the bar is not especially high. The study found that top organic results usually include only 4 unique data points on average. If I publish a page with more than 4 real original claims, figures, or answers, I create another lever for earning visibility in increasingly competitive organic search.

The analysis also found that almost every search leaves adjacent questions unanswered. On-Page used synthetic reader questions, meaning plausible related questions generated for the study, and found room for new pages to answer those questions more completely. That immediately reminds me of query fan-out.

I saw a similar pattern in an analysis of ChatGPT citations.

“A single evergreen page covering 10+ query intents is worth more in AI citation reach than 10 single-intent pages. The ROI of comprehensive content is front-loaded: one well-built page compounds citation reach over time. The long tail exists, but the top 5% of pages capture a disproportionate share of ongoing citation activity.” – The science of how AI picks its sources

That is why I believe high-intent prompts should be monitored across the full buyer journey. I would map them across the five stages from Reasoning Lift: Problem, Exploration, Comparison, Validation, and Selection. I would also use more accurate AI prompt tracking to understand where those questions emerge, then answer them with the kind of knowledge only the brand can provide.

My main takeaway is simple: most pages are only middling on originality, genuinely original pages are still a minority, and scoring high enough to stand out is achievable without an extraordinary lift.

The limitation is just as important. This study focuses on classic search visibility and rankings, which makes sense because the SEO concept of information gain comes from Google patent language. It does not analyze AI citations or mentions, and it does not appear to include AI Mode or AI Overviews.

Caveat: Being the primary source may not win the citation

This is the part of proprietary data advice I think gets skipped too often. Everyone says to publish original research. Far fewer people test whether AI rewards the brand that created the number or the page that presents it in the clearest, most extractable way.

More data analysis is still coming, but based on analyses completed at Growth Memo over the last year, I already see two patterns worth paying attention to.

The entity types that predict ChatGPT citations the most are DATE and NUMBER (from The science of what AI actually rewards). Highly cited pages tend to be dense with specific entities, such as a particular methodology, a precise statistic, or a named comparison. Even when another source picks up my proprietary findings and gets cited instead, those external third-party authority signals can still build over time.

Entity-richness and balanced sentiment matter (from The science of how AI pays attention). Generic advice is vague and risky. Specific entities are grounded and verifiable. Proprietary data can produce, verify, validate, and create entity-rich content at the same time. I can explain why a feature saves a certain percentage of dollars, how many hours clients save, or how performance compares with previous vendors. When I add balanced sentiment to the analysis and explanation, I get a stronger tactic from the same asset.

If the hypothesis holds that first-party data is crucial in the era of AI search, then publishing proprietary data is necessary, but it is not enough. LLM extraction structure, along with the sites AI search engines already trust for a topic, helps decide who actually earns the citation, even when the brand owns the data.

That is the frustrating part: an aggregator can repackage my benchmark into a cleaner, answer-ready page and collect the citation my research earned.

Who wins: Brands that already have proprietary product, usage, or pricing data and also structure that data for extraction while continuing to build organic brand authority. This connects directly to How to build an AI SEO strategy that outlasts tactics.

Who loses: Brands publishing opinion content that any tool can replicate, brands ignoring off-site authority, and primary sources that bury their own numbers inside narrative instead of surfacing them clearly.

I do not yet know whether some verticals reward data content more than others. The science series found that citation signals vary sharply by vertical, so I would be surprised by a uniform payoff. Still, I would not claim a pattern without data.

How to structure data for extraction

Owning the data gets me into the visibility race. How I structure that data may decide whether I win the citation.

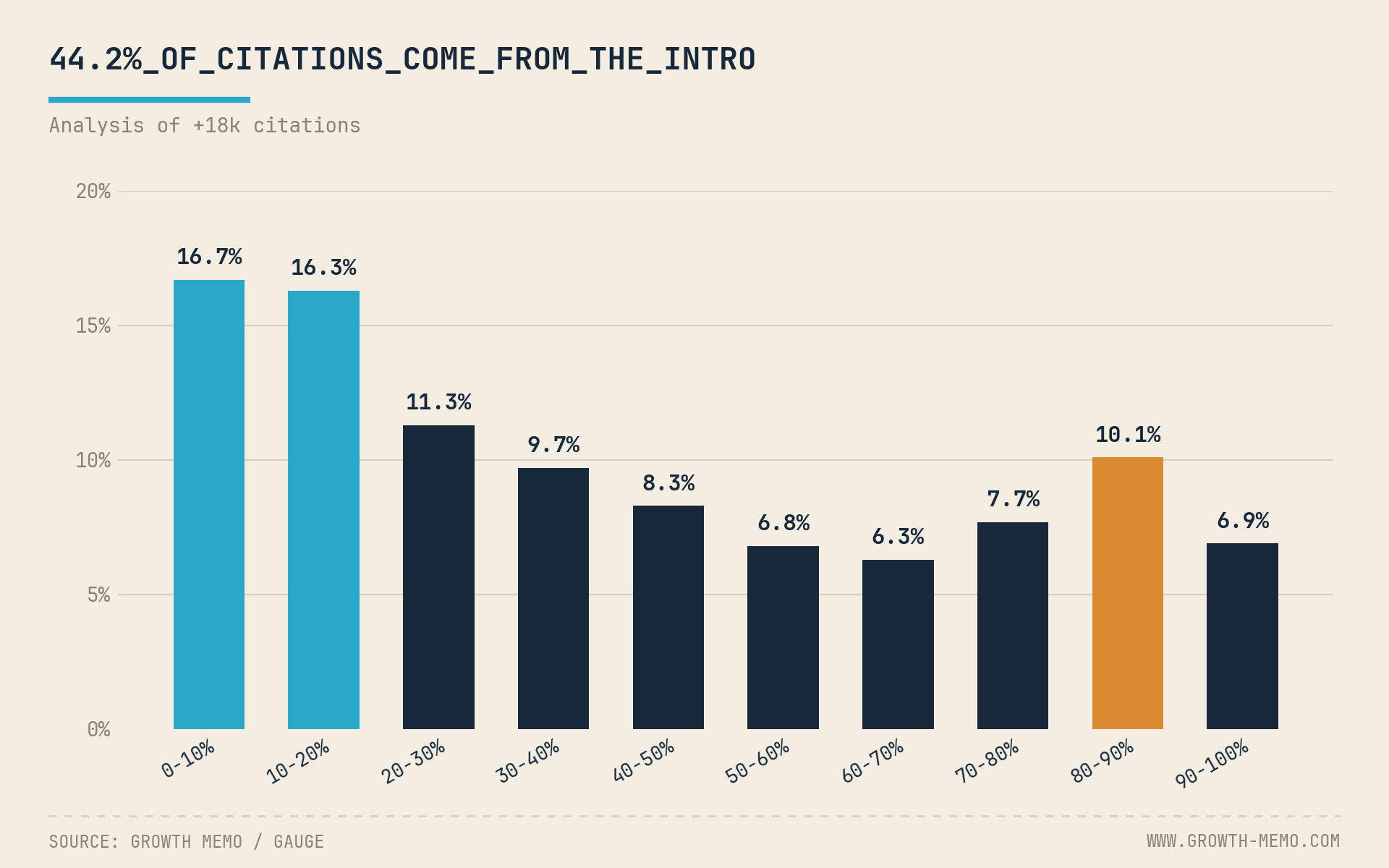

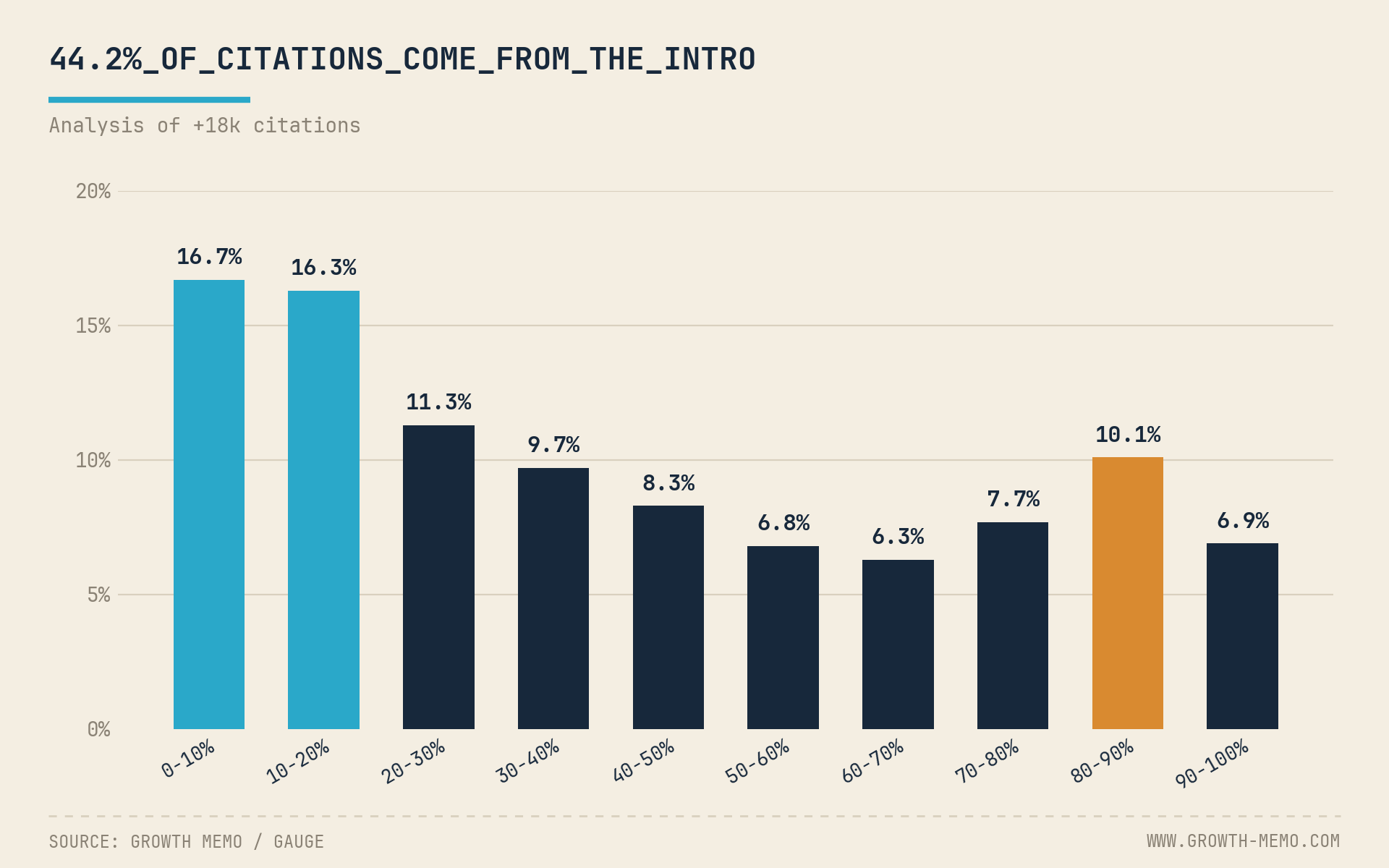

In an analysis of 18,012 verified ChatGPT citations, we found a ski-ramp distribution: 44.2% of all citations came from the first 30% of a page. The middle 30-70% earned 31.1%, and content buried deep in a long post was roughly 2.5x less likely to be cited.

The follow-up analysis across 7 verticals made the target even clearer. The 10-20% band of a page is where AI reads hardest in every vertical, while the first 10% is usually navigation and intro filler that AI skips. The bottom 10% of any page earns only 2.4-4.4% of citations regardless of vertical.

When I apply that to a data study, the structure becomes straightforward.

I lead with the headline statistic. My strongest number belongs in the first 30% of the page, ideally right after the title block where the 10-20% band begins. I want the number, the comparison, and the implication visible quickly.

I define the metric immediately. I include one sentence explaining what the number measures and which population it covers. An undefined statistic is harder to extract with confidence.

I box the methodology. I make the sample size, time window, and collection method easy to find in a short labeled block. Attribution confidence is part of what makes a number citable.

I front-load every secondary finding. I rank findings by strength, with the strongest first. A 20-paragraph narrative buildup may help human suspense, but it can cost machine citations.

I skip the suspense close. AI reads more like a busy editor than a patient student. The payoff-at-the-end structure that worked for ultimate guides often works against extraction.

This post first appeared on the author’s website and is republished here with permission.

My heart sank when I learned that Bruce Clay had passed away. I knew he had been in the hospital, but my mind went straight to the two long conversations we had last fall: one simply to catch up, and one for what would become a deeply meaningful podcast interview.

I first reached out to Bruce nearly 25 years ago. I had emailed him cold to ask whether I could republish some of his industry writing about ethics. He said yes. Somehow, the article I cited unintentionally ranked No. 2 on Google for “Bruce Clay” for years. I joked with him about that more than once, and he always seemed both amused and slightly annoyed, probably because I had done it with his own content and his own blessing.

A few years later, I worked with Bruce and many other search professionals on the board of the Search Engine Marketing Professionals Organization, better known as SEMPO. It was a business nonprofit built to support and legitimize the then-new search industry. We promoted best practices, helped make the business case for search, and later became involved in U.S. Internet policy work in the early 2010s.

SEMPO brought together board members from around the world, and in a very literal way, it took some of us around the world. That work is where I really got to know Bruce. Later, we would run into each other at conferences, sometimes even on the same panels. We were doing serious work, but we also had a great time doing it. The organization lasted about 15 years, and if I remember correctly, Bruce was one of its founding members around 2000 or 2001.

One memory of Bruce has stayed with me vividly. A group of us from the SEMPO board were walking back to our hotel on the east side of Midtown Manhattan after dinner. A snowstorm had just begun, one that would leave several feet of snow by the next day. The usual roar of traffic had been softened by the weather and the empty streets. It was eerie, but almost joyously quiet. The city that never sleeps seemed to be taking a nap under a blanket of snow.

Then something happened that I had never seen before, and have never seen since.

As snow poured silently into the streets, a massive lightning strike hit just a few blocks away, over Bruce’s shoulder. I do not know whether he saw it directly. It felt like an explosion. We stood there for several minutes trying to understand the contrast: a shattering bolt of lightning between skyscrapers, in the middle of a torrent of snowflakes, with not a drop of rain.

None of us knew what to call it. I believe Bruce called it “thunder snow,” and the name stuck. In that moment, his naming streak continued.

Bruce was, and remains, the real deal in search. His legacy was never only about coining a term. He pushed the field forward, taught others generously, and stayed deeply connected to the people he cared about. Like many of the earliest professionals in search, he helped shape practices that still feel foundational today. Through his writing, interviews, books, tools, and hundreds of industry events, he became one of the people the industry looked to for clarity. For many who remember the beginning, and for many who still followed him closely, Bruce was the GOAT.

I always felt that Bruce approached search intellectually. I do not think he saw it only as a job. It was exciting, unfinished, and new. Very few people get to help invent an entirely new discipline, and Bruce understood what that meant. He also recognized that AI is one of those moments now, and he approached it with the same curiosity, energy, and insight he brought to early search. Many people in the industry may only now be realizing that Bruce pioneered things they do every day. They feel obvious now, but they were not obvious then. Even the basics had to be debated and established.

He was not only passionate about search. He was passionate and generous toward the people in search. If you cared about the work, you were part of his tribe. That was true for thousands of people in the industry, myself included.

With Bruce, I could get deep into the weeds of the trade and still talk broadly about where everything was headed. He was an engineer with an MBA, and that combination came through in his leadership, expertise, and authority. He understood the work from top to bottom, and then back to the top again.

He was also genuinely kind. He had friends around the world. In our last conversations, I sensed that he was content with his life and accomplishments, and that he felt blessed by the path life had given him. He had nothing left to prove.

In the podcast interview, Bruce was as sharp and insightful as ever. He offered some of the most sensible thinking I have heard about where search is going in the world of LLMs. He was still innovating, just as he had been when search first began taking shape nearly 30 years ago.

Because search is so closely tied to language, I have been especially interested in how we think about, and what we call, this “new” thing. Bruce’s perspective helped crystallize my own research. Over the last year, I have watched much of the industry move toward the same conclusion he shared in our discussion.

If you are one of the many thousands of people who talked shop with Bruce over the years, I think you will recognize him in the ideas that follow. You may even relive some of your own conversations with him.

As I reviewed the podcast transcript, I realized we had recorded hours of conversation beyond search, including cars and all kinds of other subjects. At the end of our first conversation, he said goodbye with great love and care. That was Bruce. Those words land differently with me now, and they always will.

Rest in peace, Bruce. I miss you already.

What Bruce taught me in our final industry conversation

When I asked Bruce to talk about how he got started in the 1990s, he took us back to 1996. He had been working in corporate roles and wanted to become a consultant. His background was in math, programming, mainframes, PCs, networking, and optimization. When the Internet began moving into the mainstream, he saw something that matched both sides of his skill set: marketing and technical work.

He started studying search engines because that was where the opportunity was. He experimented with what they wanted, adjusted web pages, and watched rankings appear. Then people began calling him and paying him. What he thought might become a one-person consulting business grew quickly into something global, with offices and work across Japan, Australia, Asia, Europe, India, and beyond. Bruce told me he never would have predicted it would take off the way it did.

I reminded him how small the field was in those days. There were literally only tens of people doing this early on. Bruce was one of the first to build a legitimate service for businesses that needed to rank for their own brand names and for broader generic terms, while other corners of the field were still experimenting with black-hat tactics.

Bruce pointed out that this was three years before Google. Search was a wild west. There were more than 20 major search engines, and many of them were taking data from one another. At the first SEO conference he remembered attending, all of the leading people in the field sat together at one round table in a bar. He joked that if a natural disaster had happened there, the whole industry might have disappeared.

We talked about Danny Sullivan, Search Engine Watch, Search Engine Strategies, and the early vocabulary of the industry. Bruce had long been credited with helping coin the term “SEO,” though he was careful to say that no one can know who said something first. What he did know was that only a handful of people were in the room when the term started to take hold.

At the time, other terms were in play, including “search engine positioning” and “ranking.” Bruce believed “optimization” won because it sounded technical, valuable, and precise. It was like fine-tuning a race engine. People could see themselves building a profession around it. Once the industry attached itself to that word, the term spread quickly around the world.

That led us into the newer terms now being proposed around AI, including AIO, GEO, and AEO. I have been writing about how many of these terms still depend on the word “optimization.” Bruce’s view was clear: search engine optimization was never limited to organic blue links. It was about optimizing for anything a search engine produces that can drive business and traffic.

In Bruce’s view, if AI appears inside search and influences discovery, citations, visibility, or traffic, then it belongs under SEO. GEO and AIO were not separate disciplines to him. They were extensions, just like link building or on-page optimization. He warned that many new terms are marketing labels more than practical new fields. If the work required to appear in AI results is still mentions, links, schema, authority, content structure, and rankings, then the work is still SEO.

That point stayed with me. Bruce said that if someone claims you no longer need SEO and only need AI optimization, you should watch closely, because either they are going to do SEO under a different name or they do not understand what they are doing. He believed ranking in AI was possible, but the method was deeper and more complex than traditional SEO. To him, it was still SEO, just several levels more advanced.

We also discussed whether AI feels like search did in the late 1990s. Bruce believed it does in important ways. AI depends heavily on search engines because search engines have spent decades fighting spam and building trust signals. AI systems do not yet have that same history, so they rely on what search engines have already learned to filter, evaluate, and rank.

Bruce also believed AI could still be gamed at the content level. If enough pages repeat a false idea, an AI system may begin to treat it as true. He had already seen examples of people trying to influence AI answers by placing their names into “best SEO” lists across enough sources. To him, this was a sign that AI would need its own version of the spam fight search engines have been having for decades.

One of the most important parts of our conversation was Bruce’s explanation of Google AI Mode and how it changes the way SEOs should think about structure. He described how a query can produce an overview, followed by sections and subsections that allow users to drill into narrower parts of a topic. When a user clicks into a section, the supporting sites can change to match that specific subtopic.

That means content cannot simply be built around one broad keyword anymore. Bruce believed pages need to be structured so each section can stand on its own as an expert answer. A page should support a topic, but every H2-level section may need its own clarity, completeness, and internal logic. In his view, this raises the importance of siloing across a site and within a page.

I framed this as a shift from keyword-led thinking to context-led thinking. Bruce agreed and connected it to entities, fan-outs, references, and cross-links. Keywords helped build the industry, but he believed the future depends on understanding entities in context. If content cannot answer the question clearly, it fails the core purpose of AI-assisted search.

Bruce described the long-term target as something like the Star Trek computer: no matter what question someone asks, the system provides the answer. We are not there yet, but that is the direction. For websites, he believed the future architecture is question-centered, highly usable, structured into sub-silos, and able to answer and refer within a page while also fanning out to supporting pages.

That naturally led us to content. Bruce said that for years SEO treated content like a stepchild, but now content is a peer. If SEO teams and content teams do not share the same goal, they will keep writing the way they did 20 years ago and fail in the AI search environment. He was already being hired to train content teams, even though he did not consider himself a “content guy” in the traditional sense.

He believed the industry still suffers because SEO and content do not cross-pollinate enough. Content marketers may not attend SEO conferences, and SEOs may not spend enough time learning how content teams actually work. That separation matters more now because the structure of a page, the expertise of each section, and the way a topic is divided all affect visibility in AI-driven search experiences.

Bruce’s advice was direct: stop spreading one keyword across a page and calling that optimization. Instead, build each section as if it were a standalone expert answer. If the sections belong to the same theme, they should support one another, but each needs to carry its own weight. In his words, the hierarchy is no longer only the page. The hierarchy is also the section of the page.

When I asked Bruce about AI-generated content, he made an important distinction. AI is a tool, not a solution. He did not believe businesses should simply generate content, read it once, and publish it. Detection tools are inconsistent, and search engines may not reliably identify every AI-generated page. But that does not make low-effort AI content a good strategy.

Bruce believed AI is strongest as a research assistant. His own Pre-Writer product was built around that idea: gather deep research and give a human writer a stronger starting point. The writer still finishes the work, adds style, voice, judgment, compliance, and business understanding. For Bruce, reducing a four- or five-hour writing project to two hours was a win. Replacing the writer entirely was not.

He was especially clear that writers are artists. AI does not know a business the way its people do, and it does not bring the same finesse or judgment. The future, in Bruce’s view, requires writers, SEOs, and AI workflows to be integrated around shared goals. Without that maturity, teams will keep producing pages that look like they were built for search 10 years ago, and those pages will be ignored.

We ended by talking about tools. Bruce reminded me that in the beginning, he wrote tools because none existed. He built one of the first page analyzers, including what he once called a keyword density analyzer. He later received a patent related to that kind of technology. His tools were never meant to replace large platforms like Semrush, Ahrefs, or Surfer. They were meant to extend them by analyzing things those platforms did not.

Bruce pointed people to seotools.com and described the tools as inexpensive power tools, not products designed for the masses. Some users did not understand them at first, but came back later when they saw the value. He was still building, still solving problems, and still thinking about what the industry needed next.

Near the end, Bruce mentioned a newer tool designed to show traffic loss through Search Console data over time, helping site owners see whether they had fallen off a cliff or declined gradually. It struck me as classic Bruce: while others complained that something should exist, he was building it.

I thanked him for the conversation, and he answered with warmth: he was glad I had him on, and he loved talking with me. I hear those words differently now. I am grateful we had that final conversation, and I am grateful for everything Bruce gave to search, to this industry, and to the people inside it.

I see ChatGPT’s high-reasoning mode acting like a very different search surface for brand visibility. In a Semrush analysis with Kevin Indig, ChatGPT cited different domains than it did in minimal reasoning mode and ran nearly five times as many web searches before answering.

By the numbers, the shift is hard to ignore. Only 25.6% of cited domains overlapped between minimal and high reasoning for the same prompts. That means nearly three in four sources changed when ChatGPT moved from Instant-style answers to Thinking-style answers.

I also noticed that Thinking mode used more sources overall. Citation rates rose from 50% in minimal reasoning to 68% in high reasoning. When ChatGPT did cite sources, it used more of them too, increasing from 2.6 to 4.5 citations per response. Across the test set, high reasoning ran 1,130 web searches, compared with 245 for minimal reasoning.

Reddit lost ground in high-reasoning answers. Reddit’s citation share dropped from 15% to 7% when high reasoning was turned on. User-generated content and review sites also declined, falling from 14.3% to 6%.

At the same time, I saw more weight shift toward institutional and official sources. Government and academic sources rose from 1.9% to 8.8%, while official documentation and support pages grew from 12.4% to 17.5%.

Comparison prompts drove the most search activity. At the comparison stage, high reasoning averaged 24 sub-queries per prompt, compared with 5.5 for minimal reasoning. Average citations also peaked there, reaching 9.8 per high-reasoning response versus 5.8 for minimal reasoning.

For example, I would expect a CRM comparison to trigger separate searches for pricing, integrations, security, support pages, and documentation before ChatGPT forms its final answer.

Early citations also appeared to last longer. High reasoning was more likely to carry a brand from early research into later buying questions. In four of the 20 journeys tested, a brand cited at the problem stage still appeared at the selection stage. Minimal reasoning showed no full-journey persistence, meaning no brand cited at the Problem stage survived through to the Selection stage of the same journey.

I also found the domain reuse pattern important. High reasoning reused the same domains more often within a single answer, with the same domain appearing multiple times in 51 of 100 high-reasoning responses. Minimal reasoning did this in 26 of 100 responses.

Finance saw the biggest citation jump. The lift varied by category, but finance had the largest increase, with citation rates rising 28 percentage points in high reasoning. Health and lifestyle rose 24 points, while B2B SaaS gained 16 points.

Consumer tech barely moved, rising only 4 points. Even though high reasoning ran more sub-queries for consumer tech prompts than for any other category, it often landed on the same brands and sources as minimal reasoning.

Why I care about this: content can appear in fast ChatGPT answers but disappear when users ask more complex questions. Visibility depends on whether my pages, documentation, and third-party references can surface across the smaller searches ChatGPT runs before it answers.

About the data: Semrush and Indig tested 100 prompts across 20 buyer journeys in B2B SaaS, finance, consumer tech, and health and lifestyle. Each prompt ran once in minimal reasoning and once in high reasoning. The analysis tracked citation rate, cited sources, and fan-out queries.

I’m tracking an important AMP update from Google Search: users who tap AMP results will now be sent directly to publisher-hosted AMP pages instead of cached AMP pages shown inside Google’s AMP viewer.

A Google spokesperson told Search Engine Land, “Starting today, we are updating how we connect users to AMP pages from Search, taking them directly to the AMP host pages.”

Google also made it clear that this is not a ranking change. AMP content will continue to rank like any other webpage, and Google said the serving and ranking of AMP content in Google Search and Google Discover will remain the same.

From my perspective, the practical value here is mostly on the publisher side. By sending searchers straight to the AMP host page, Google says publishers should have simpler analytics management and tracking, along with less maintenance work when creating and supporting AMP content.

Google told us it will continue to support the open-source AMPhtml format, and it also posted the update in its Search documentation.

I also think it’s worth noting how much AMP’s role has changed over time. AMP has not received preferential treatment in Google’s Top Stories for a while, and AMP pages are much less common to encounter than they once were. Search Engine Land even turned off AMP in 2021.

It has been a long time since I’ve had much reason to cover AMP closely, but this change matters because it shifts the user journey back to publisher-hosted pages while keeping AMP’s ranking treatment unchanged.

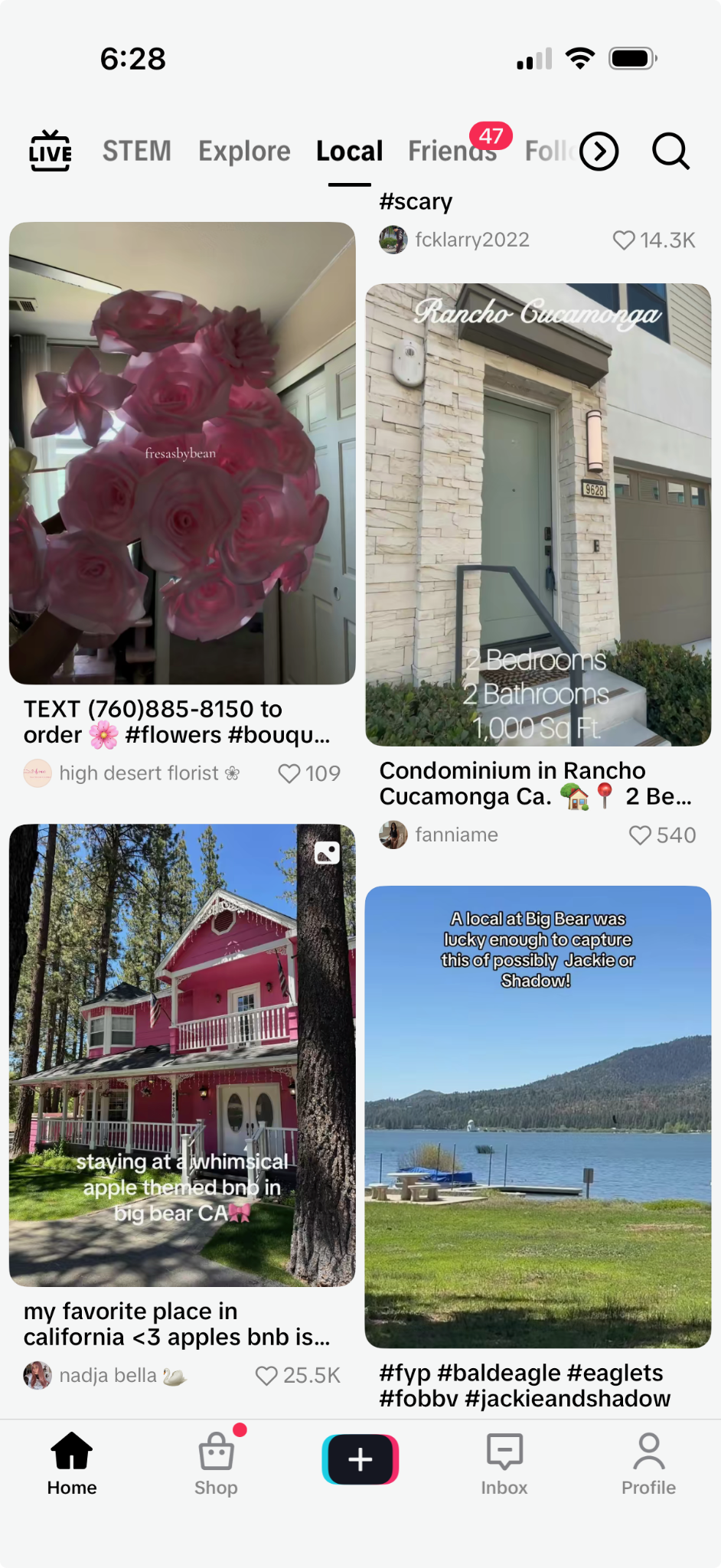

I see TikTok becoming harder to ignore in SEO because discovery no longer happens in one clean path. Someone might find a restaurant on TikTok, verify it through Google Reviews, check Reddit for honest opinions, scan the menu on the business website, and then book a table. Someone else might take those same steps in a completely different order.

Nearly half of U.S. consumers used TikTok as a search engine in 2026, up from 41% in 2024, according to Adobe survey data. What stands out to me is why people search there: short-form video, storytelling, interactivity, tutorials, product reviews, personal stories, and influencer recommendations all make the platform feel more immediate than a traditional results page.

I also think TikTok recent updates show how seriously the platform wants to be part of the search journey. Many purchase decisions are visual, social, emotional, and trust-driven, which is exactly where TikTok has strength. With Local Feed, AI summaries, creator reviews, and shopping features, TikTok is trying to meet people at the moment they are exploring, comparing, and deciding.

So instead of asking whether TikTok is a traditional search engine, I ask a more useful question: how do I make sure people can find, understand, trust, and choose a brand wherever their search journey begins? More often than many marketers want to admit, that starting point may be TikTok.

TikTok SEO Is More Than Hashtags Now

I think of TikTok SEO much like traditional SEO: it is the work of making a business, place, product, service, or experience easier to discover. As TikTok has evolved, the discovery surfaces have expanded far beyond captions and hashtags.

In the past, I mostly associated TikTok optimization with captions, hashtags, trending sounds, posting times, and the hope that a video would land on the For You feed. Those pieces still matter, but they are no longer the full picture.

Today, I have to think about TikTok Search, recommendations, Local Feed, Places, reviews, comments, creator content, visual cues, product signals, and AI-assisted discovery. A stronger TikTok SEO strategy now includes search query relevance, spoken topic clarity, on-screen text, captions, hashtags, location context, creator reviews, comments, product visuals, and the searches people make after seeing a video.

TikTok documentation says search results can be shaped by how well content matches a query, along with hashtags, sounds, user interactions, language, and location. The For You feed also weighs user interactions, content information, user information, and watch behavior, which means usefulness and engagement both matter.

Local Feed Creates a New Discovery Surface

TikTok launched Local Feed in the U.S. on Feb. 11 as a home-screen tab for nearby content related to travel, events, restaurants, shopping, small businesses, and local creators. TikTok says posts can appear based on location, topic, and when the content was published.

I see Local Feed as another organic discovery touchpoint, especially for local businesses. A restaurant can appear while someone is deciding where to eat nearby. A wellness club can show up when someone is looking for weekend plans. A venue can answer practical before-you-go questions before a guest ever reaches the box office.

There are limits I would keep in mind. TikTok precise location setting is optional, off by default, available only for users 18 and older, and still rolling out across the U.S. TikTok also says private accounts, accounts for users under 18, and posts limited to Friends or Only You will not appear in Local Feed.

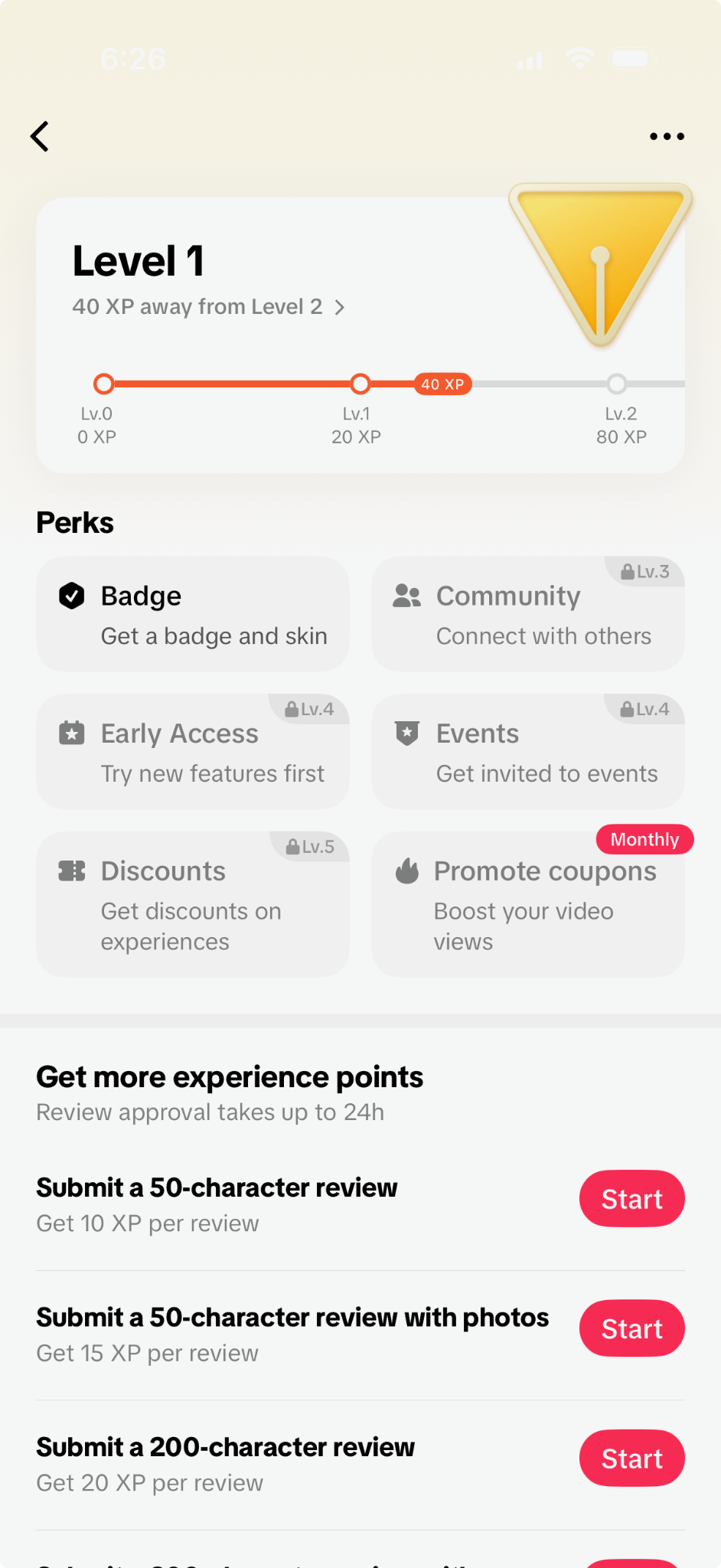

Local Explorer Shows TikTok Is Investing in Places

TikTok Local Explorer Program is one of the clearest signs I have seen that the platform wants to build stronger place-based discovery. The program encourages people to submit location-based reviews and rewards participation with experience points, levels, badges, community access, and other perks.

I would not assume every market has the same access or level of activity, because availability has been limited and uneven by region. Still, the direction matters: TikTok is building more ways for users to evaluate places inside the app.

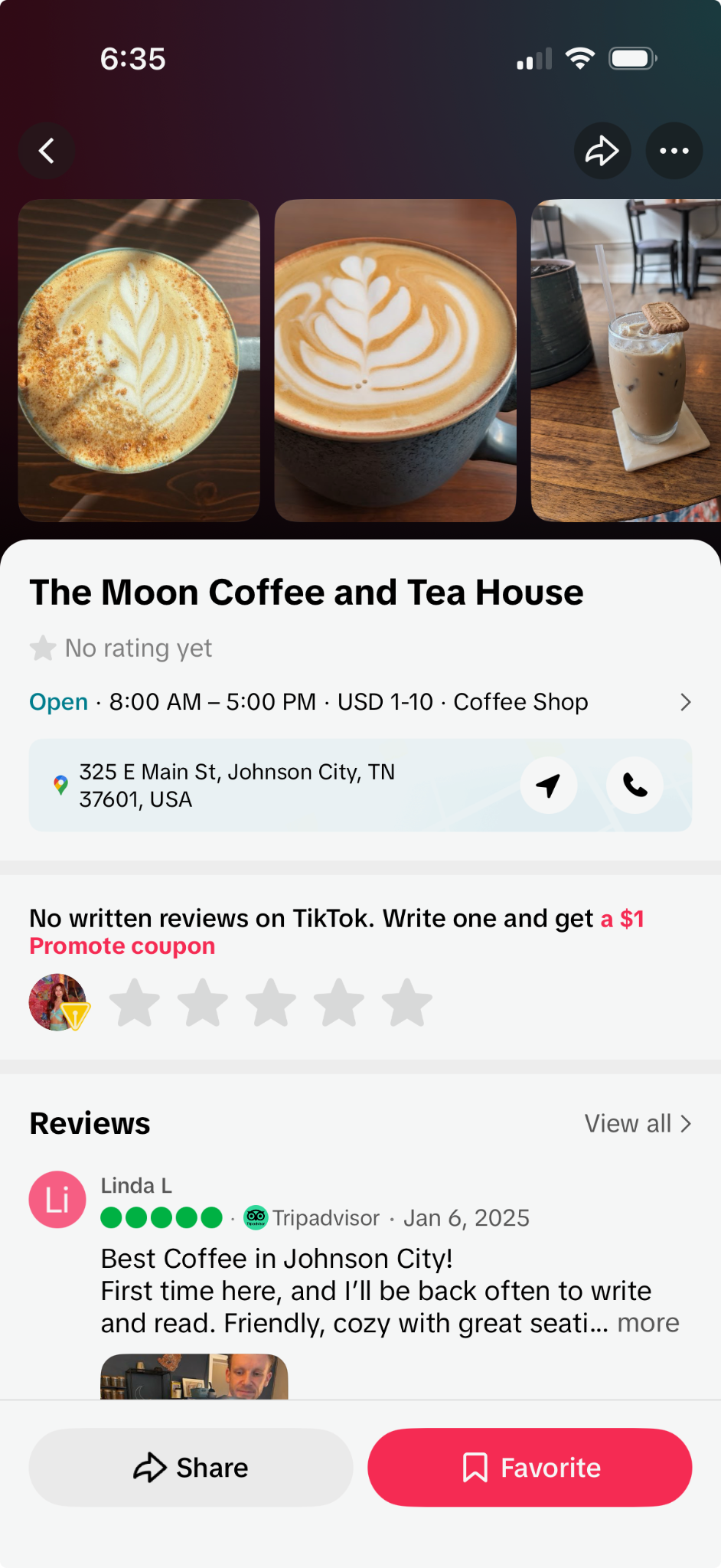

I have also seen TikTok incentivize reviews for places that do not already have TikTok reviews. In one example, a coffee shop had no TikTok reviews, and I was offered a $1 Promote coupon to leave one.

When a place does not have native TikTok reviews, I have seen TikTok pull reviews from TripAdvisor and, in some cases, Google. That makes the Places tab a useful comparison surface where people can evaluate reviews, videos, and comments before deciding whether to visit a local business.

Visual Search Links Matter More Than Exact Keywords

TikTok increasingly adds automated search links and related query prompts beneath videos. I pay attention to these because they show how TikTok can connect a video to a broader topic, place, or product discovery path.

For example, a video about a place like Glen Ivy may show a search bar at the bottom that lets users explore more related content. Those search bars can appear even when a creator has not overloaded the description with exact-match keywords, which tells me TikTok is reading more than just captions.

TikTok Shop Turns Discovery Into Buying

With TikTok Shop, someone can see a product in a video, search for it, compare it through comments and creator content, and buy it without leaving the app. That makes TikTok more than a discovery channel for ecommerce brands; it can become part of the full purchase path.

I would optimize TikTok Shop content around the information TikTok needs to understand a product. Search relies heavily on how well a shopper query matches product information such as titles, categories, attributes, and content context.

TikTok Shop has also released Shoppable Photos in beta for select sellers. Eligible sellers can create image-based posts, include multiple photos, and tag products directly in the post. These posts may appear in the For You feed, Search, and the Shop tab, giving sellers a simpler way to showcase inventory without producing a full video.

AI Is Becoming Part of TikTok Discovery

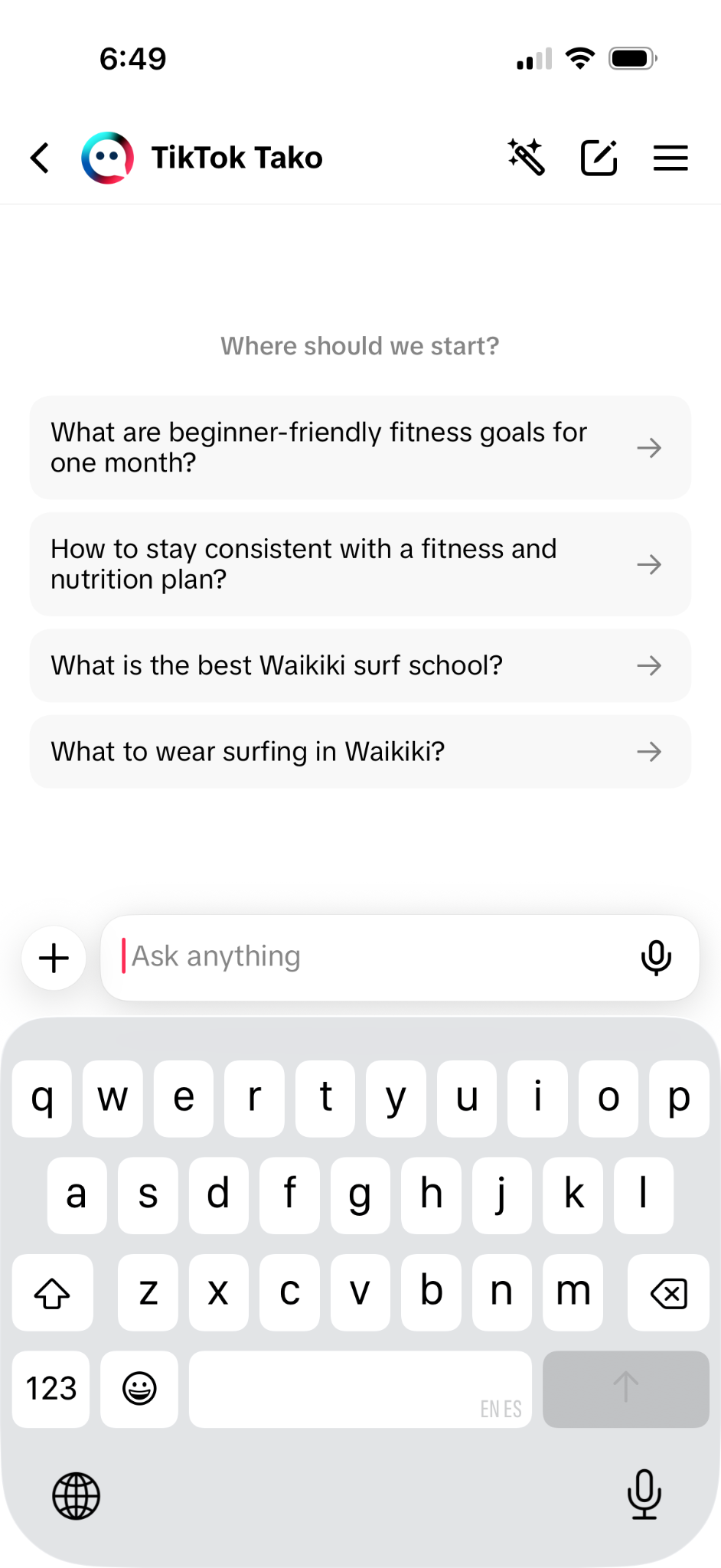

I am also watching TikTok AI-assisted discovery features closely, even though availability varies by market, account, and test. Features such as Tako, AI Overviews, Quick Highlights, AI summaries, and Content Studio all point in the same direction: TikTok wants to help users search, summarize, and create faster.

Tako is TikTok chatbot, and it lets users search in a way that feels similar to using the app search bar. It can surface relevant TikTok videos and external sources, including articles.

TikTok also now offers AI Overviews for some searches. When users search a topic, they may see an AI-generated summary of the results. If they click a visual search bar, they may also see Quick Highlights that summarize that search experience.

The Places tab includes AI summaries too, and users can see how many posts were used to generate a place summary. For local businesses, that makes the quality and clarity of creator posts, customer videos, and reviews even more important.

On the creator and seller side, TikTok AI tools can help generate captions, hashtags, and even videos. I would treat these tools as helpful support, not a substitute for real strategy, because features like Content Studio are still not available to everyone and remain in testing.

How I Would Improve Visibility on TikTok

On TikTok, visibility comes from what people search for, what TikTok can understand, and what the camera actually shows. That means I would focus less on cleverness and more on showing people what they need to see before they choose a business, product, or place.

For restaurants, I would show menu items, exterior signage, the dining room, takeout packaging, seasonal dishes, and neighborhood cues. Those visuals help both users and TikTok understand what the place offers and where it fits.

For retail, I would show product displays, packaging, try-ons, shelf layout, gift ideas, and the storefront. The more clearly a video communicates what is available, who it is for, and where someone can get it, the stronger the discovery signal becomes.

I would also build simple habits into every TikTok content workflow: use location context naturally, show products clearly, show the storefront or interior when relevant, mention the city or neighborhood when it helps, create timely content around local moments, tag the physical location when appropriate, and work with creators who already understand discovery-driven content.

Keyword Research

I would start TikTok keyword research inside the app because that is where the search behavior is happening. Seed topics might include best brunch, World Cup outfits, things to do in [location], wedding inspiration, or gluten-free bakery.

From there, I would search each phrase on TikTok, document autocomplete suggestions, review suggested filters, look for Others searched for prompts, study top videos, and pay close attention to comment themes. I would also test city and neighborhood modifiers, then compare TikTok findings with Google Search Console, Google autocomplete, Reddit, YouTube, and site search data.

TikTok Creator Search Insights can add another useful layer by showing personalized information about search topics, content gaps, and how content tied to searched topics is performing.

Keyword Placement

I would place the core topic where TikTok and viewers can recognize it quickly: in the first few seconds of the video, the first text overlay, the opening of the caption, relevant hashtags, location tags, pinned comments, reply videos, the profile bio, playlist names, and creator briefs.

Comments and Reviews

I would treat comments and reviews as visibility assets, not afterthoughts. That means pinning genuinely helpful comments, replying to repeated questions with videos, correcting misinformation when trust is at stake, watching for recurring objections, and turning repeated questions into FAQs, landing page content, Google Business Profile posts, and future videos.

A creator saying that a bakery is the best gluten-free option in Portland because it takes cross-contamination seriously may be more useful than a generic five-star review. That kind of specific language can shape website copy, FAQ strategy, and customer messaging.

Referral Traffic and Branded Search

I would track TikTok referral traffic and monitor branded searches over time. When a TikTok post performs well, I would annotate it and compare branded search trends against a baseline.

I would look for directional movement in branded clicks, branded impressions, TikTok referral traffic, Google Business Profile actions, and engagement on related pages. At the same time, I would avoid giving TikTok credit for every increase without considering PR, paid campaigns, email, promotions, seasonality, and other marketing activity.

Attribution may never be perfect, but imperfect measurement does not make TikTok influence meaningless. I would rather measure directional impact than ignore a channel that is clearly shaping discovery behavior.

I Would Explore TikTok Instead of Ignoring It

Someone may find a business on TikTok before they ever search for its name on Google or ChatGPT. Someone else may turn to TikTok midway through the journey to decide whether the business is worth the trip, the purchase, or the recommendation.

Either way, I believe TikTok has earned a meaningful role in modern SEO strategy. Between Local Feed, Places, Tako, AI summaries, creator reviews, and TikTok Shop, the platform keeps adding new ways for businesses to be discovered, and many of those opportunities are still underused.

I can now use Google Trends to quickly add previous time period data to a chart, making it easier to see how search interest compares with the same length of time immediately before it.

Google announced the update on LinkedIn, saying that I can now compare how a trend has changed against preceding periods directly inside Google Trends.

What it looks like. Google shared a GIF showing the feature in action, with a comparison line added directly to the Trends chart for faster context.

How it works. I can go to Google Trends, enter a search term or topic, and then use the new chips that appear above the timeline. Those chips surface percentage changes across different periods, including month-over-month, week-over-week, and specific year-over-year comparisons.

With one click, I can overlay the historical comparison line onto the graph and immediately see whether interest is rising, falling, or following a familiar seasonal pattern.

Why I care. Google Trends is already a helpful source for spotting topics, keywords, and audience interest patterns. When I am planning content, SEO priorities, or marketing campaigns, being able to compare current demand against a previous period gives me a clearer read on timing and momentum.

This update gives me more historical perspective inside Google Trends, which can make trend analysis faster and more useful for content strategy and marketing planning.