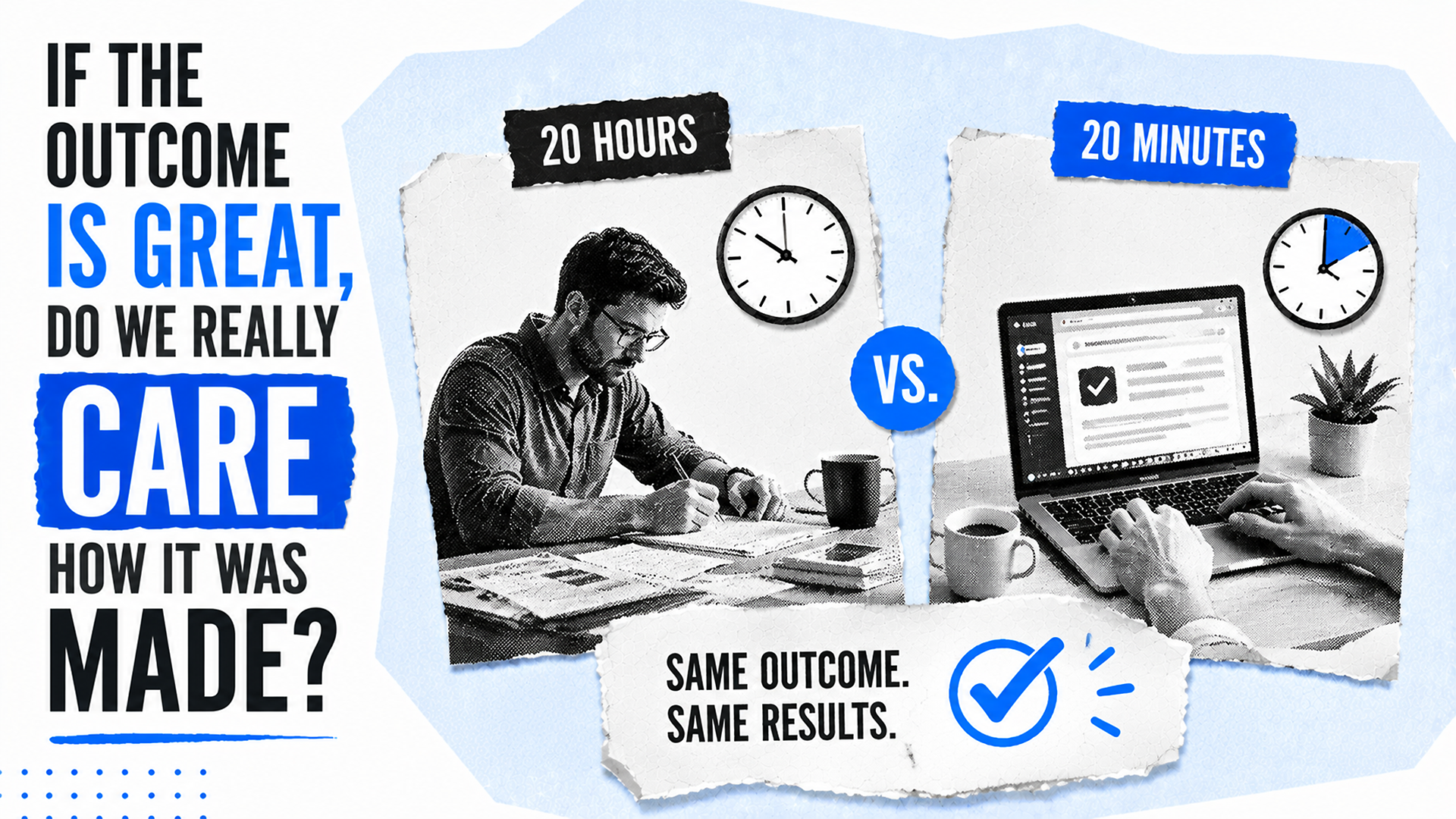

When I think about AI deliverables, I keep coming back to a simple scenario: a client receives two pieces of work.

Both deliverables solve the problem they were hired to solve. Both are accurate, useful, and tied to the same business outcome. The client is happy, and from the outside, there is no meaningful difference in the results.

Then the client learns that one took 20 hours to create, while the other took 20 minutes. That is when the uncomfortable questions begin.

Was AI involved? Should the faster deliverable cost less? Is the person who completed it less skilled because they found a faster, more efficient way to reach the same result?

What I find most interesting is how differently many of us react to AI depending on which side of the transaction we are on. I love using AI when it saves me time, but I also understand why customers can feel uneasy when they discover AI helped create something they paid for.

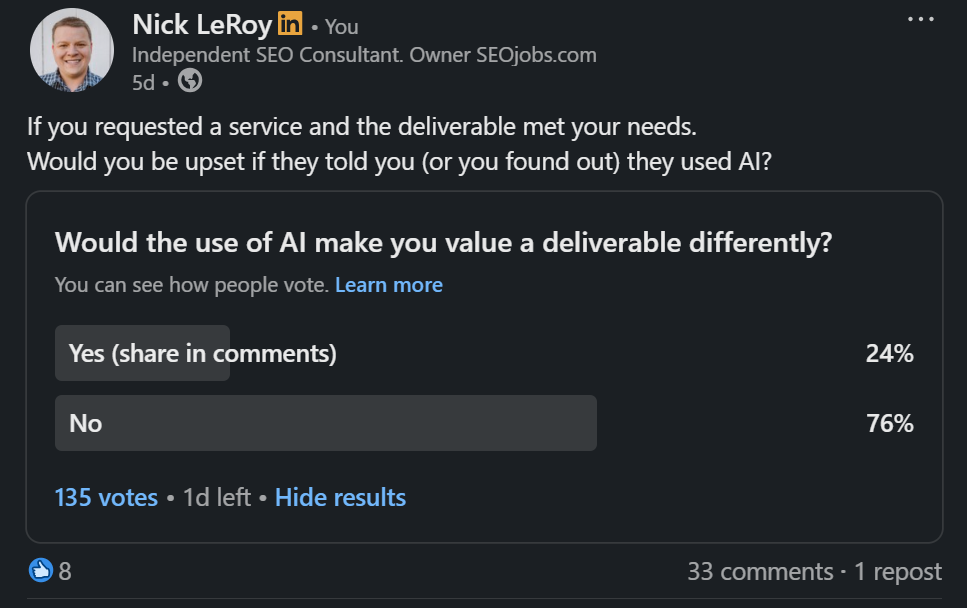

I recently ran a LinkedIn poll asking a simple question: if the outcome is great, do we really care how it was made?

The responses reinforced something I have been thinking about for a while. Many of the strongest objections people have to AI are not really about quality at all.

The Time vs. Value Fallacy

I think part of the discomfort comes from the fact that we have spent decades tying value to effort.

Long hours feel valuable. Fast work feels suspicious. Struggle often gets mistaken for expertise.

The harder something appears to be, the easier it becomes to justify the price attached to it.

There is an old story about a ship engine that stopped working. After multiple failed attempts to repair it, the owners brought in an engineer with decades of experience. He inspected the engine, tapped it once with a small hammer, and the machine roared back to life.

His invoice was $10,000.

The owners were furious and demanded an itemized bill. The response was simple: hammer tap, $2. Knowing where to tap, $9,998.

People debate whether that story is true or just a useful tale for people like me who believe in value-based pricing. But whether it really happened almost does not matter. The lesson still holds.

People are not paying for the tap. They are paying for the expertise behind it.

That is what makes AI such an important topic for me. It forces us to confront a question many of us have avoided for years: are we paying for expertise, or are we paying for visible effort?

Those are not always the same thing.

The Objections That Actually Matter

To be clear, I do not think every objection to AI is unreasonable. I have shared plenty of my own concerns, and some of them are serious.

In fact, I think the strongest arguments against AI have very little to do with how quickly something was created.

Those are legitimate concerns. What stands out to me is that none of them has much to do with how long it took to create the deliverable.

They are questions of trust.

Can the output be trusted? Can the recommendation be defended? Can someone confidently stand behind the work if it is questioned six months from now?

Because when something goes wrong, nobody gets to blame the AI. The employee is accountable. The consultant is accountable. The company is accountable.

That is why I have always found the quality debate to be the least interesting part of the conversation. The more important question is not whether AI was involved. It is whether the outcome is trustworthy enough for someone to put their name behind it.

The Outcome Test

The more I think about AI, the less interested I become in whether it was used.

Instead, I find myself asking a different set of questions. Was the outcome accurate? Was it useful? Was it better than the alternative? Would I be willing to stand behind it with my name, reputation, and credentials on the line?

If the answer to all of those questions is yes, then I have a hard time arguing that the production method matters more than the result.

Ironically, this is also where humans become more important, not less.

The future is not machines versus humans. I know, "The Terminator" and "I, Robot" movies will never feel the same. The real shift is humans using AI versus humans who refuse to adapt.

AI can accelerate execution, but people still decide what should be built, what should be published, and what risks are acceptable. More importantly, people are still responsible for the outcome.

The people who lose to AI will not be the ones using it. They will be the ones still evaluating effort while everyone else is measuring outcomes.

This post first appeared on the author’s website and is republished here with permission.

I do not see search demand disappearing. I see it moving. In this analysis, 29% of high-volume search demand is declining, while nearly the same amount is growing somewhere else. Overall demand is essentially flat because people are redistributing how and where they search instead of abandoning search altogether.

That changes how I think about SEO strategy. I would not start by panicking over shrinking keywords. I would start by identifying which queries are losing volume, which ones are gaining momentum, and where a brand can build enough authority to appear in both traditional search results and AI-generated answers.

This study looks at where search demand is shifting, which industries are seeing the sharpest changes, and what those patterns mean for SEO teams trying to adapt to AI-driven discovery.

How I studied AI’s impact on search

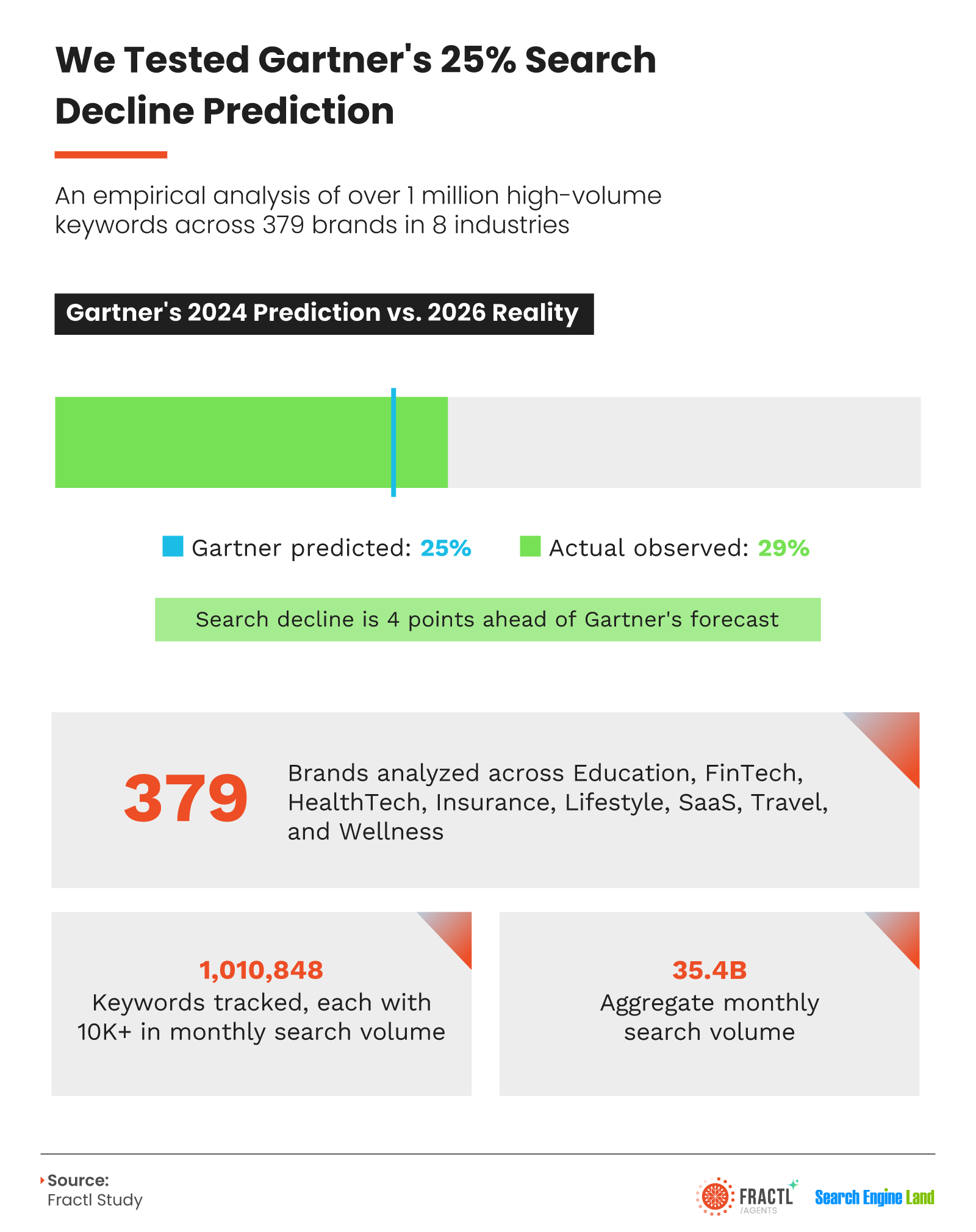

In 2024, Gartner predicted that traditional search engine volume would fall 25% by 2026 as consumers shifted to AI chatbots and virtual agents. Fractl and Search Engine Land set out to test that prediction. (Disclosure: I’m the co-founder of Fractl.)

I worked from Semrush data covering 1,010,848 high-volume keywords, each with at least 10,000 monthly searches, across 379 brands in eight verticals. I also looked at survey responses from 1,004 U.S. consumers to better understand how AI is changing the way people search.

The analysis measured which keywords gained or lost search volume over the past year, how those shifts differed by industry, and how consumer behavior is evolving as AI tools become part of everyday discovery.

The 29% search decline is real, but it depends on the vertical

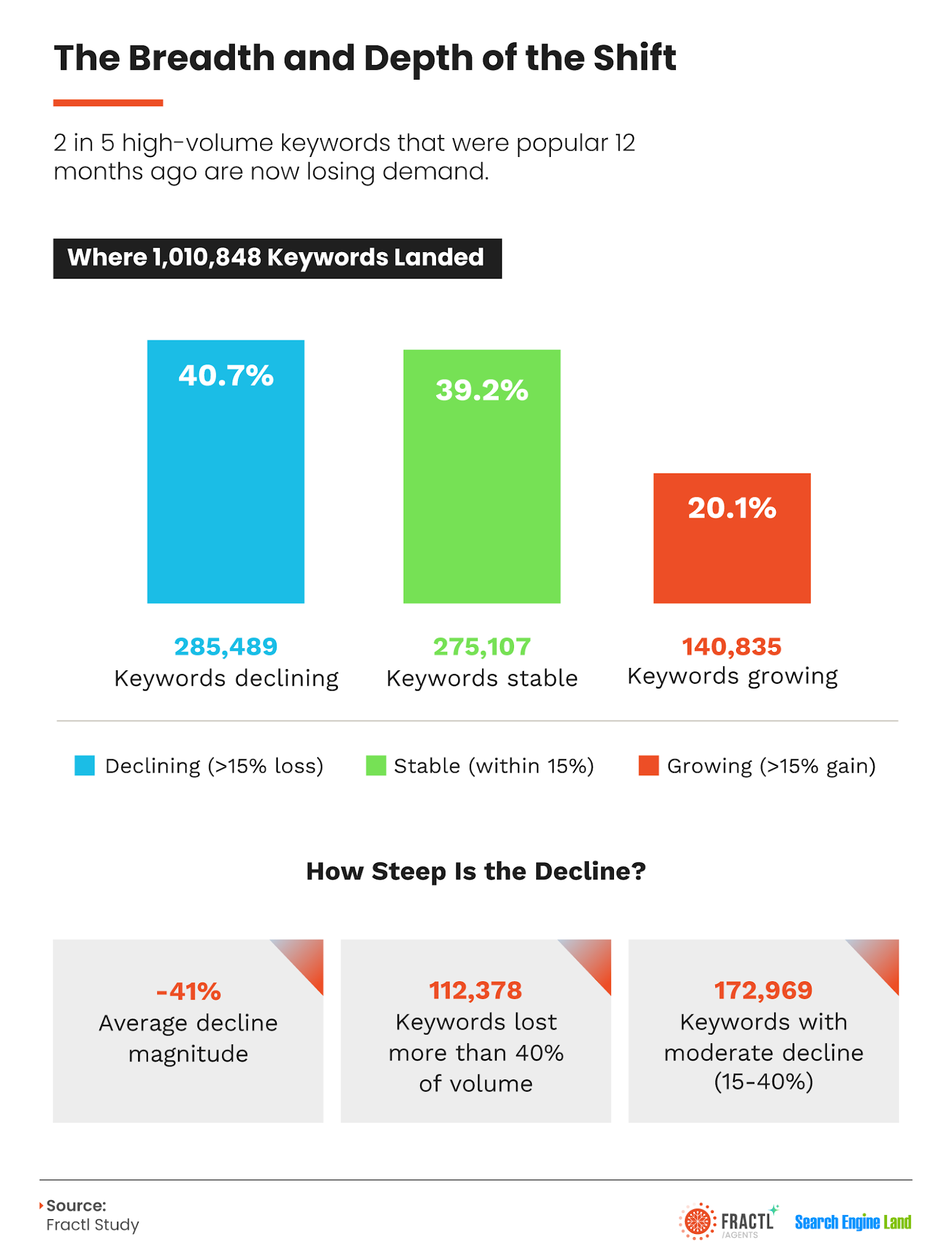

Across more than 1 million high-volume keywords, I found that 29% of search volume is in measurable decline. That is 4 percentage points above Gartner’s forecast. In a dataset representing 35.4 billion monthly searches, that difference represents a meaningful amount of search activity.

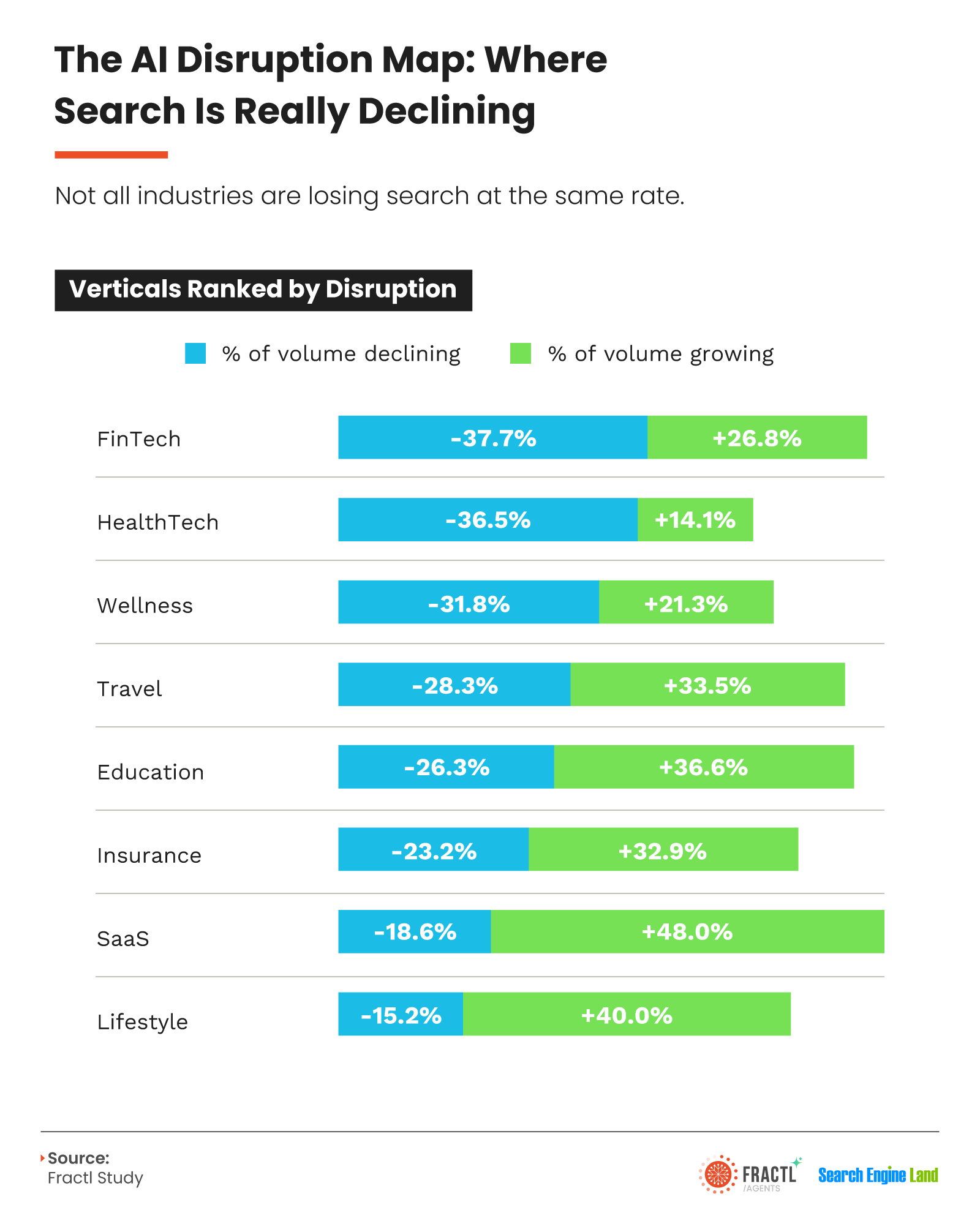

The impact is not evenly distributed. FinTech showed the largest decline at -37.7%, while Lifestyle saw the smallest decline at -15.2%. Only three of the eight verticals, Insurance, SaaS, and Lifestyle, came in below Gartner’s 25% threshold. FinTech, HealthTech, and Wellness were well above it.

The pattern makes sense when I look at how information-heavy each category is. When a chatbot can answer the question completely, such as summarizing drug interactions, explaining deductibles, or giving a quick overview of a fund, search volume is more likely to fall. When people need to compare prices, complete a transaction, or navigate to a specific site, search demand tends to hold up better.

That is why transactional verticals such as SaaS, Lifestyle, Insurance, and Travel are growing or staying close to flat. Information-heavy verticals such as HealthTech, FinTech, and Wellness are seeing the largest declines.

Before reacting to broad claims about AI-driven search decline, I would benchmark these findings against the specific vertical in question. HealthTech and FinTech teams should expect more exposure than the overall 29% decline suggests. SaaS and Lifestyle teams have more reason to challenge the idea that search demand is simply collapsing.

Search demand is being redistributed

The headline number gets attention, but the offset is just as important. Demand did not vanish. It moved to a different set of words, and those are the terms I would want to understand first.

Among the high-volume keywords tracked, 40.7% are in measurable decline, meaning they lost more than 15% of their volume over the past year. Within that group, the average decline is -41%, and 112,378 keywords lost more than 40% of their volume. For brands that depend on those terms, the impact is significant.

At the same time, 20.1% of keywords are growing by more than 15%. When I add up the volume on both sides, the decline and growth almost cancel each other out.

The 285,489 declining keywords represent roughly 10.29 billion monthly searches. The 140,835 growing keywords represent roughly 10.31 billion monthly searches. Across the entire dataset, the net change is +16.8 million searches per month.

Fewer keywords are growing than declining, but the growing keywords carry more volume each. That is why the totals balance out. In practical terms, I see demand relocating more than shrinking.

The vertical-level growth-to-decline ratios show where that new demand is landing. Lifestyle leads at 2.6x, with 40% of keywords growing versus 15% declining. SaaS follows closely at 2.5x, with 48% growing versus 19% declining. HealthTech sits at the other end with an inverted ratio of 0.4x, making it the most disrupted vertical in the set.

The first audit I would run is simple: pull the tracked keyword set, filter it by year-over-year volume change, and see which side of the ledger the portfolio sits on.

Non-branded queries are the most vulnerable

I see non-branded queries as the easiest ones for AI chatbots to replace. When a search term does not include a brand name, the user is not necessarily trying to reach a specific site or source. The full exchange can happen inside the chat window.

Across the dataset, 90% of all tracked search volume is non-branded. HealthTech, at 99.6%, and Wellness, at 98.5%, are the most exposed. Insurance, at 73.8%, and SaaS, at 82.0%, are less exposed, and both are growing overall. SaaS volume is up 48% year over year, while Lifestyle is up 40%.

If I wanted to identify the content most at risk, I would start with keyword patterns. They offer one of the clearest signals in the study.

The reason SaaS and Lifestyle can be heavily touched by AI and still grow comes down to what happens after the AI answer. If AI recommends a project management platform or a couch, many people still search for the specific brand, retailer, review, or product page before buying. The AI answer creates a downstream search.

HealthTech and FinTech often behave differently. A drug-interaction question or a “what is a deductible” query can be answered completely inside the chat window. There may be no next step that sends the user back to Google.

If a category produces complete AI answers with no natural next click, I would treat AI visibility as a core strategy, not an SEO side project. In those cases, showing up in the answer may be the entire opportunity.

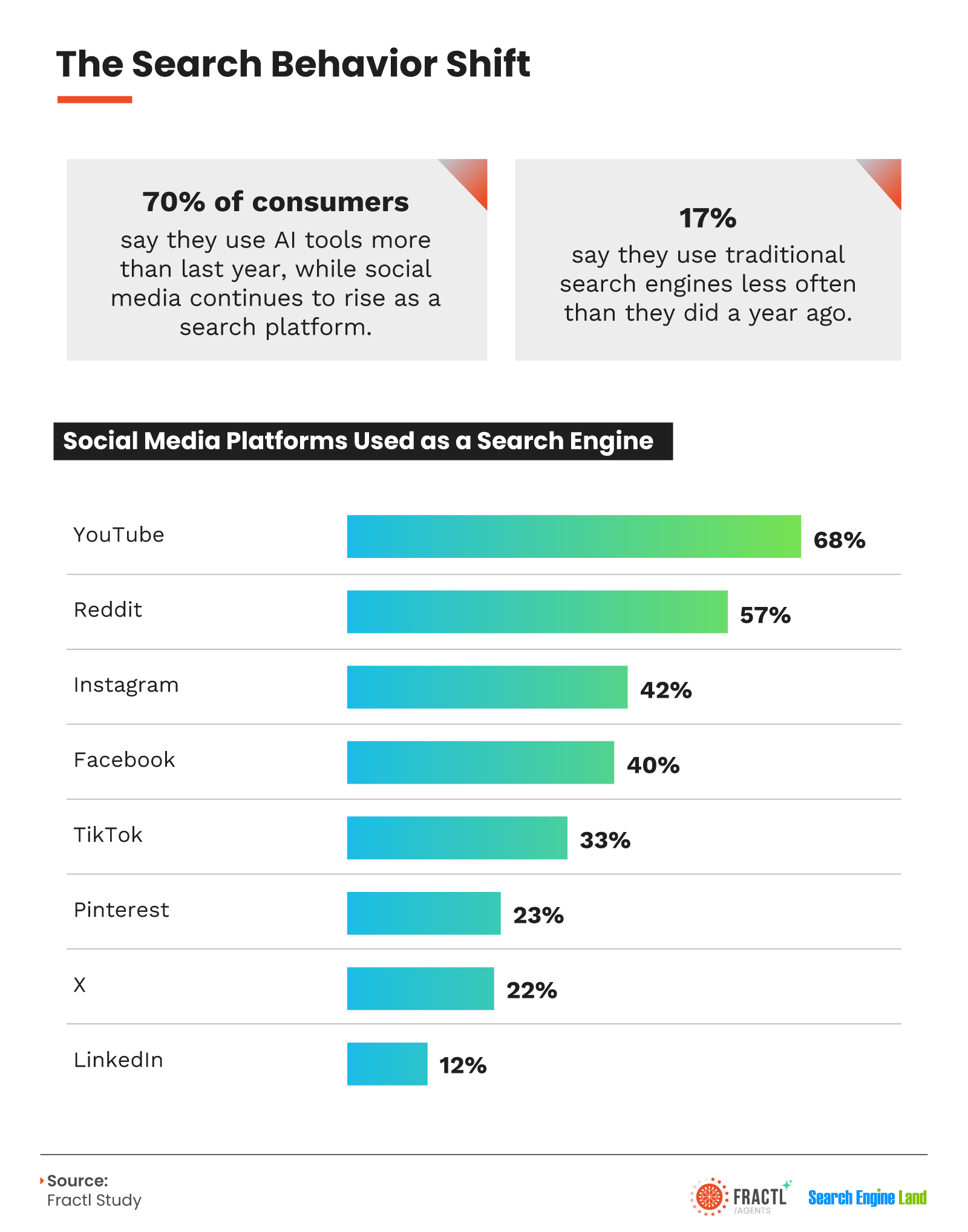

70% of consumers use AI more, but only 17% use search less

The keyword data shows what is happening in the index. The survey data shows what is happening in the minds of the people doing the searching.

Search behavior is spreading across more platforms. Many people are adding AI to their routines without giving up Google.

Social platforms are also acting like search engines in a way they did not a few years ago. YouTube leads at 68%, followed by Reddit at 57%, Instagram at 42%, Facebook at 40%, and TikTok at 33%.

If I had not already prioritized YouTube and Reddit, I would move them up the list. Both rank ahead of TikTok, Instagram, and Facebook as search destinations, and both can also surface in Google results, which gives visibility there a compounding effect.

What has actually moved from Google to AI

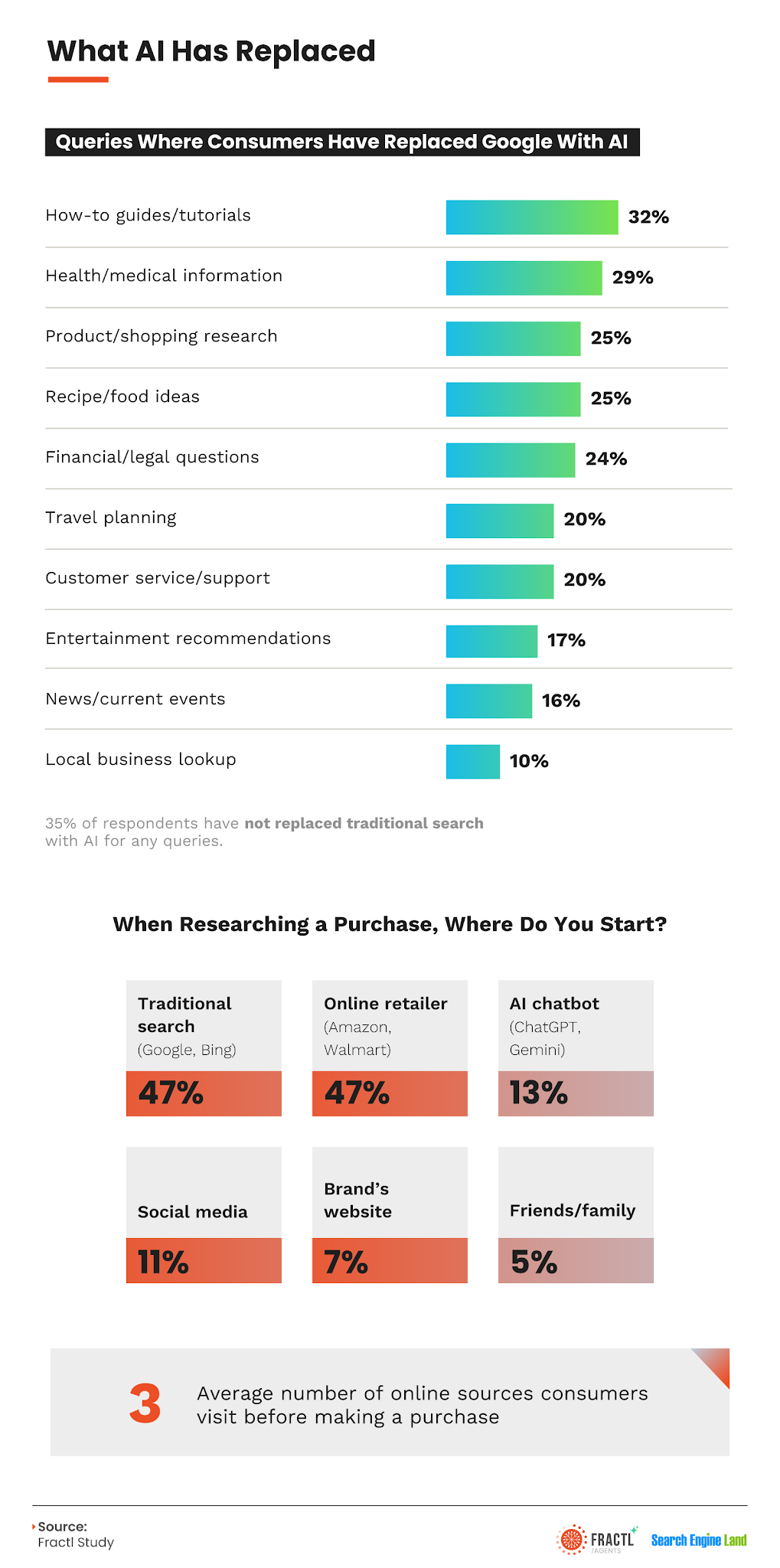

More than a third of respondents, 35%, say they have not replaced traditional search with AI for anything yet. Among those who have, how-to guides and tutorials have taken the biggest hit.

For purchase research, 47% of consumers start with a traditional search engine, tied with online retailers at 47%. Only 13% start with an AI chatbot, and shoppers check an average of three online sources before making a purchase.

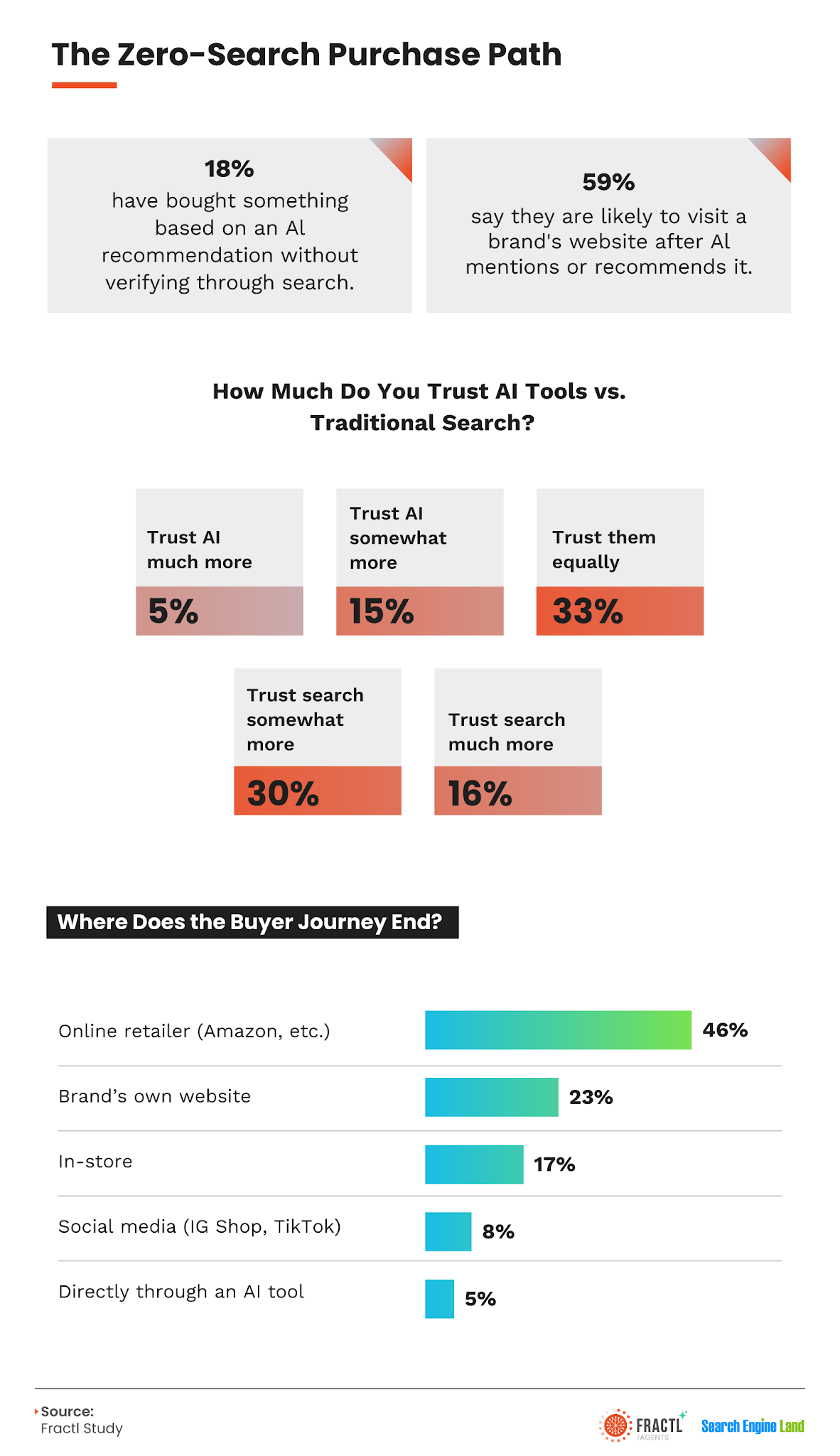

The number I would bring to a strategy meeting is this: nearly one in five consumers, 18%, have bought something based on an AI recommendation without checking it against a separate search.

That creates a different kind of buyer journey. In that path, the brand may never receive a search-driven touchpoint. To be considered, the brand has to be one of the names the chatbot returns.

Gen Z and millennials are 2.5x more likely than baby boomers to buy based on an unverified AI recommendation, at 20% versus 7%. Across all consumers, 59% say they are likely to visit a brand’s website after an AI chatbot mentions or recommends it.

That is the emerging conversion funnel I am watching closely. Brand mentions in AI answers are starting to function like rankings. Visits to a brand’s website after an AI mention are starting to look like the new click-throughs.

Trust is still mixed. In the survey, 33% of consumers trust AI and traditional search equally, 46% trust search more, and 20% trust AI more.

More than half of consumers, 56%, are at least somewhat skeptical of AI product recommendations. I read that as a sign that people are willing to let AI filter and shortlist options, but many still want to verify before they buy.

The 5-year outlook: Google is not going away, but the shift matters

When asked whether Google will still be their primary search tool in five years, 52% of consumers say yes, including 17% who say definitely and 35% who say probably. Another 27% are unsure, while 20% say probably or definitely not.

The top reasons people prefer AI over traditional search are better summaries across sources, at 21%; faster and more direct answers, at 20%; and the ability to ask conversational follow-up questions, at 19%. More personalized results and avoiding website click-throughs were much lower, at 6% and 4%.

When asked what would bring them back to traditional search, the top answer was AI giving unreliable answers, at 35%. That means much of this shift depends on whether AI maintains trust as adoption scales. More accurate search results followed at 29%, then a preference for multiple source links at 22%, and privacy concerns at 20%.

The 20% who expect to leave Google are not the majority, but I would not dismiss them. A strategy does not need to be rebuilt entirely around them today, but brands do need to appear where those users are already moving.

What this means for content and SEO strategy

I see Gartner’s 25% prediction as a useful directional warning. The real shift may be steeper, but calling it only a decline misses the more important story. Total search volume is basically flat. What has changed is which searches carry the demand.

AI visibility is not just a threat to manage. I see it as a distribution channel. With 59% of consumers saying they are likely to visit a brand’s website after an AI mention, GEO has become a meaningful part of brand discovery.

Earned media, credible third-party coverage, and strong entity signals all help brands appear in chatbot answers. That is why digital PR and GEO are becoming more closely connected.

Search is moving, not disappearing.

The brands that lose will be the ones still optimizing mainly for queries that AI now answers better. The brands that win will be the ones building enough authority to become the answer, whether that answer appears in Google or inside a chatbot.

Methodology

This study combined two data sources to test Gartner’s 2024 prediction that traditional search engine volume would fall 25% by 2026.

Fractl and Search Engine Land analyzed Semrush search volume data for 1,010,848 high-volume keywords with 10,000 or more monthly searches each, covering 379 brands across eight verticals: FinTech, HealthTech, Wellness, Travel, Education, Insurance, SaaS, and Lifestyle. The dataset represented 35.4 billion in aggregate monthly search volume. Keyword-level year-over-year volume change was measured as of April 2026 and classified as declining, meaning more than 15% loss; stable, meaning within 15%; or growing, meaning more than 15% gain. Query pattern groupings, including “What is X,” “Best X for Y,” “X vs. Y,” and “How to X,” were applied at the keyword level.

Fractl and Search Engine Land also surveyed 1,004 U.S. consumers about their search habits, AI tool adoption, and purchase research behavior. The sample was 52% women, 46% men, and 1% nonbinary, with 49% millennials, 26% Gen X, 16% Gen Z, and 9% boomers. The median respondent age was 41, with a range of 18 to 82.

When I want a page to feel genuinely original, I start with original numbers. They are still one of the most reliable ways to make content stand apart, especially when those numbers come from the business itself instead of a one-off study created just to fill a content calendar.

The old approach was to pay a PR or research firm for a loosely related survey, like a car insurance FinTech commissioning road-trip research to earn a mention in Yahoo. I see that play as increasingly outdated. Almost every product now creates data worth publishing, and extracting that data is easier than it has ever been.

I do not need a full research department to compete here. The bar for standing out is lower than many teams assume.

First-party data: The strongest correlation of originality

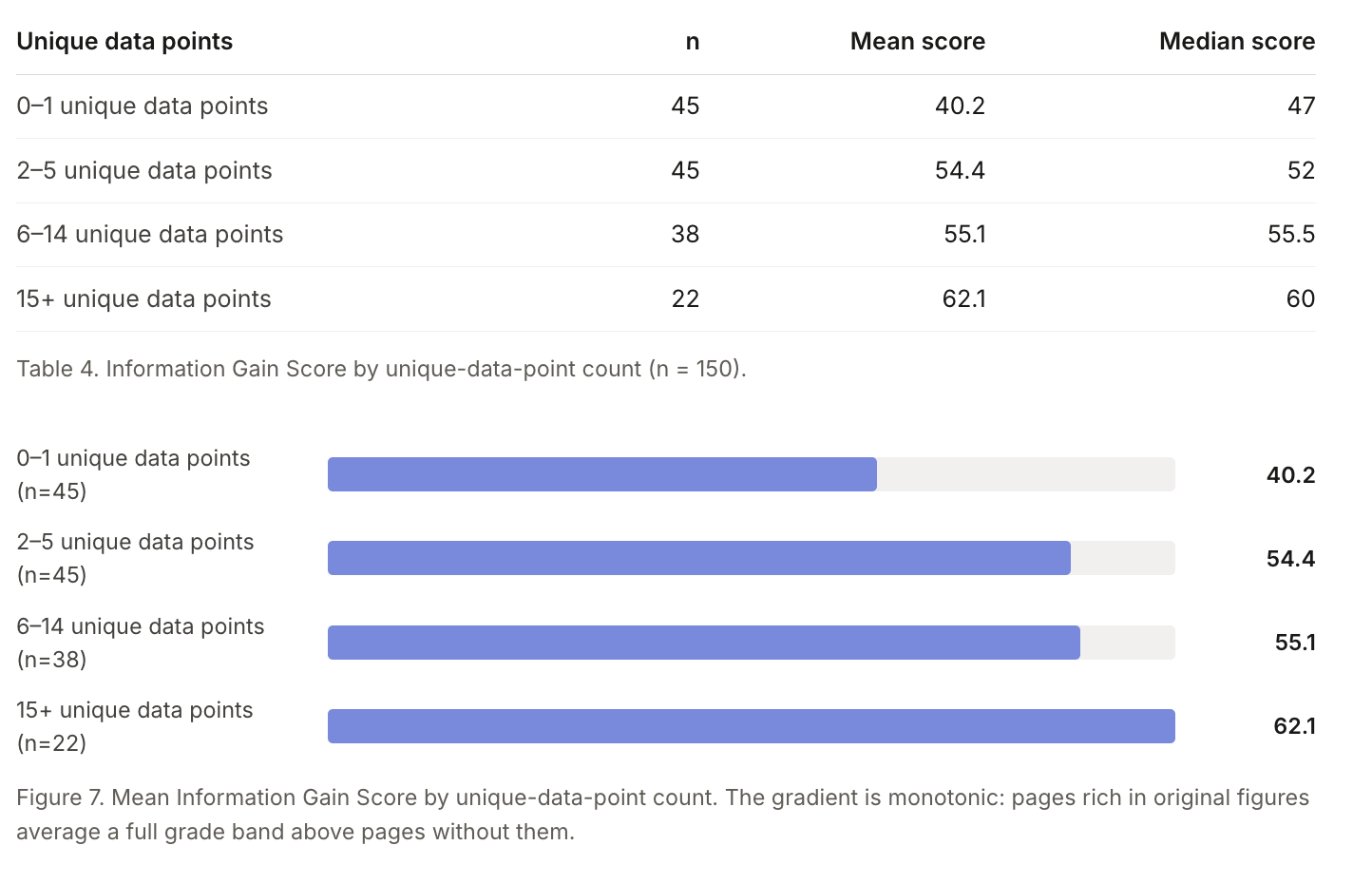

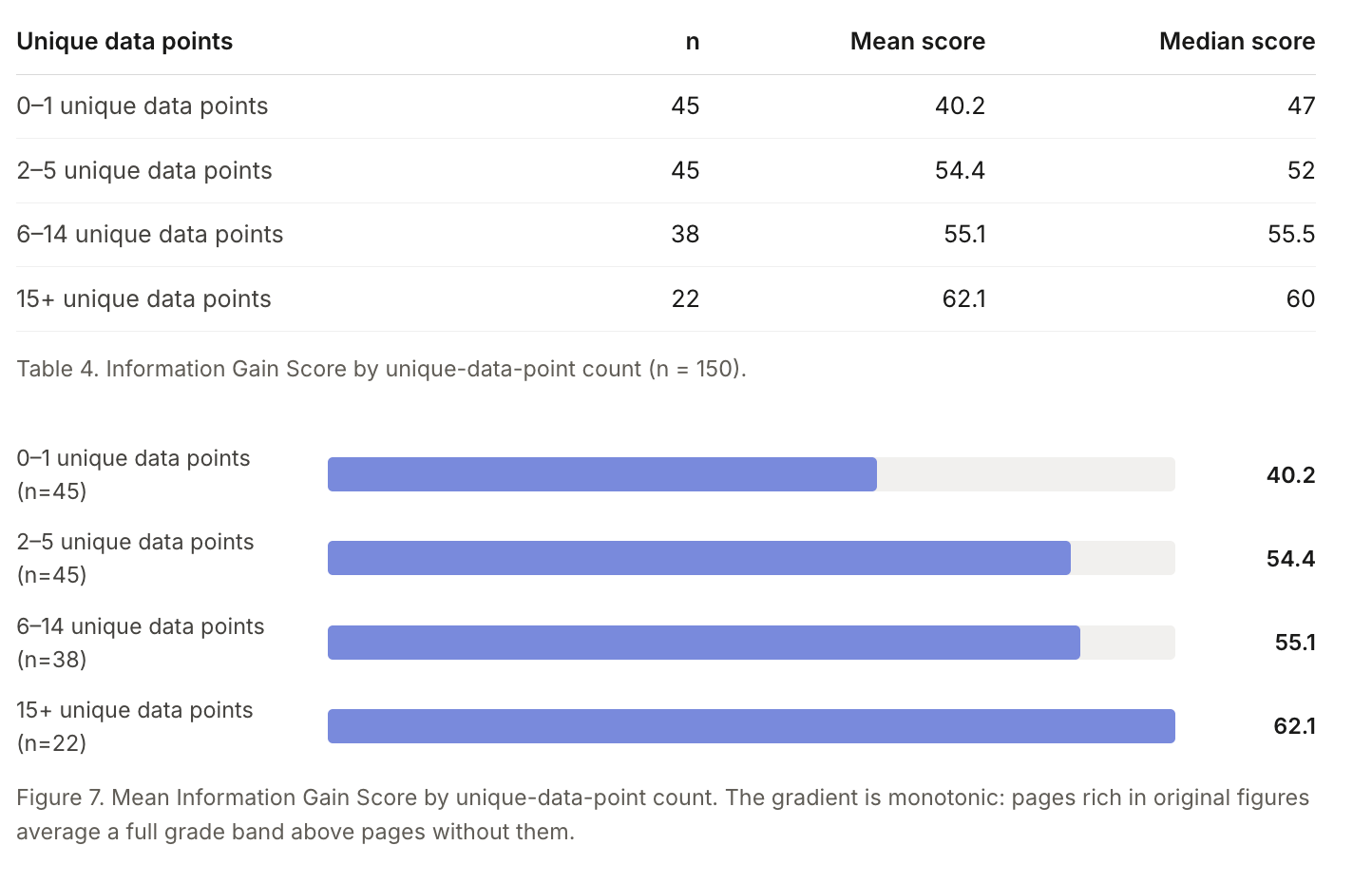

On-Page.ai’s recent information gain study scored 150 top-3 Google pages across 50 keywords and 10 verticals. The study looked at how much each page added beyond the rest of its ranking cohort, grading contribution from 0 to 100 by meaning rather than wording.

The median page scored 52. More importantly, original data correlated with that score more strongly than any other page-level trait, including content length.

Pages with at most 1 unique figure averaged an information gain score of 40.2. Pages with 15 or more unique figures averaged 62.1, and the score increased steadily at every step in between.

The good news is that the bar is not especially high. The study found that top organic results usually include only 4 unique data points on average. If I publish a page with more than 4 real original claims, figures, or answers, I create another lever for earning visibility in increasingly competitive organic search.

The analysis also found that almost every search leaves adjacent questions unanswered. On-Page used synthetic reader questions, meaning plausible related questions generated for the study, and found room for new pages to answer those questions more completely. That immediately reminds me of query fan-out.

I saw a similar pattern in an analysis of ChatGPT citations.

“A single evergreen page covering 10+ query intents is worth more in AI citation reach than 10 single-intent pages. The ROI of comprehensive content is front-loaded: one well-built page compounds citation reach over time. The long tail exists, but the top 5% of pages capture a disproportionate share of ongoing citation activity.” – The science of how AI picks its sources

That is why I believe high-intent prompts should be monitored across the full buyer journey. I would map them across the five stages from Reasoning Lift: Problem, Exploration, Comparison, Validation, and Selection. I would also use more accurate AI prompt tracking to understand where those questions emerge, then answer them with the kind of knowledge only the brand can provide.

My main takeaway is simple: most pages are only middling on originality, genuinely original pages are still a minority, and scoring high enough to stand out is achievable without an extraordinary lift.

The limitation is just as important. This study focuses on classic search visibility and rankings, which makes sense because the SEO concept of information gain comes from Google patent language. It does not analyze AI citations or mentions, and it does not appear to include AI Mode or AI Overviews.

Caveat: Being the primary source may not win the citation

This is the part of proprietary data advice I think gets skipped too often. Everyone says to publish original research. Far fewer people test whether AI rewards the brand that created the number or the page that presents it in the clearest, most extractable way.

More data analysis is still coming, but based on analyses completed at Growth Memo over the last year, I already see two patterns worth paying attention to.

The entity types that predict ChatGPT citations the most are DATE and NUMBER (from The science of what AI actually rewards). Highly cited pages tend to be dense with specific entities, such as a particular methodology, a precise statistic, or a named comparison. Even when another source picks up my proprietary findings and gets cited instead, those external third-party authority signals can still build over time.

Entity-richness and balanced sentiment matter (from The science of how AI pays attention). Generic advice is vague and risky. Specific entities are grounded and verifiable. Proprietary data can produce, verify, validate, and create entity-rich content at the same time. I can explain why a feature saves a certain percentage of dollars, how many hours clients save, or how performance compares with previous vendors. When I add balanced sentiment to the analysis and explanation, I get a stronger tactic from the same asset.

If the hypothesis holds that first-party data is crucial in the era of AI search, then publishing proprietary data is necessary, but it is not enough. LLM extraction structure, along with the sites AI search engines already trust for a topic, helps decide who actually earns the citation, even when the brand owns the data.

That is the frustrating part: an aggregator can repackage my benchmark into a cleaner, answer-ready page and collect the citation my research earned.

Who wins: Brands that already have proprietary product, usage, or pricing data and also structure that data for extraction while continuing to build organic brand authority. This connects directly to How to build an AI SEO strategy that outlasts tactics.

Who loses: Brands publishing opinion content that any tool can replicate, brands ignoring off-site authority, and primary sources that bury their own numbers inside narrative instead of surfacing them clearly.

I do not yet know whether some verticals reward data content more than others. The science series found that citation signals vary sharply by vertical, so I would be surprised by a uniform payoff. Still, I would not claim a pattern without data.

How to structure data for extraction

Owning the data gets me into the visibility race. How I structure that data may decide whether I win the citation.

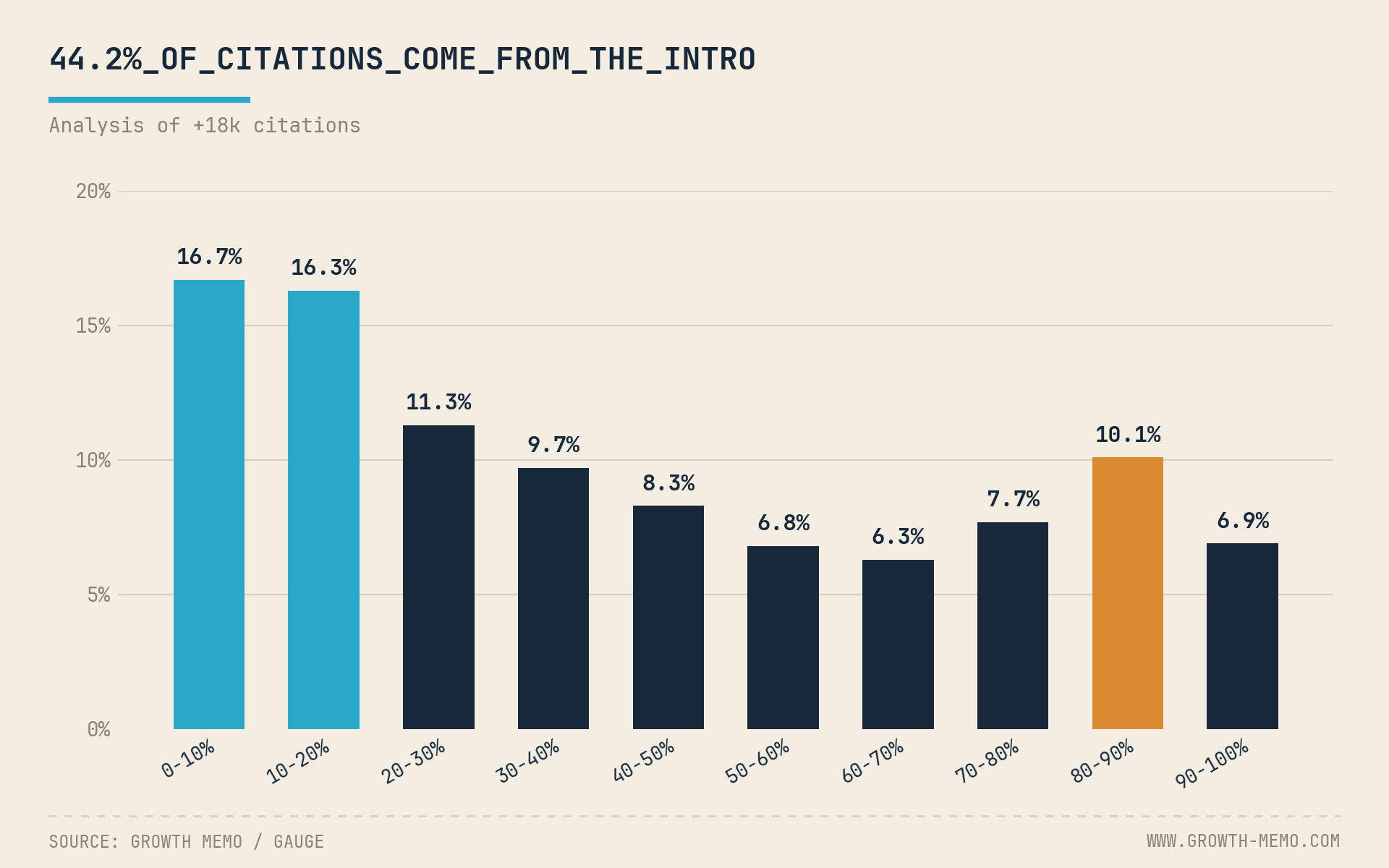

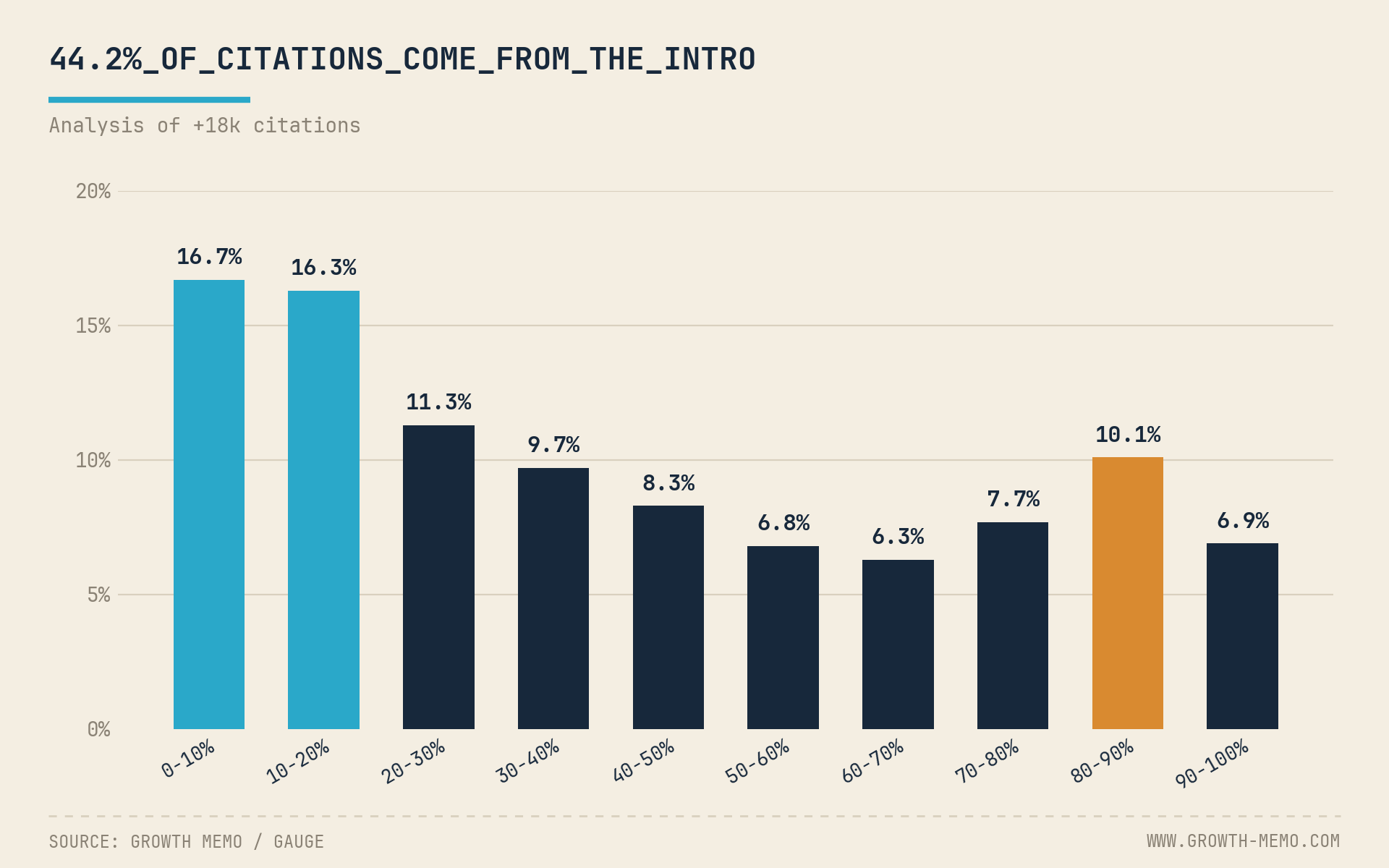

In an analysis of 18,012 verified ChatGPT citations, we found a ski-ramp distribution: 44.2% of all citations came from the first 30% of a page. The middle 30-70% earned 31.1%, and content buried deep in a long post was roughly 2.5x less likely to be cited.

The follow-up analysis across 7 verticals made the target even clearer. The 10-20% band of a page is where AI reads hardest in every vertical, while the first 10% is usually navigation and intro filler that AI skips. The bottom 10% of any page earns only 2.4-4.4% of citations regardless of vertical.

When I apply that to a data study, the structure becomes straightforward.

I lead with the headline statistic. My strongest number belongs in the first 30% of the page, ideally right after the title block where the 10-20% band begins. I want the number, the comparison, and the implication visible quickly.

I define the metric immediately. I include one sentence explaining what the number measures and which population it covers. An undefined statistic is harder to extract with confidence.

I box the methodology. I make the sample size, time window, and collection method easy to find in a short labeled block. Attribution confidence is part of what makes a number citable.

I front-load every secondary finding. I rank findings by strength, with the strongest first. A 20-paragraph narrative buildup may help human suspense, but it can cost machine citations.

I skip the suspense close. AI reads more like a busy editor than a patient student. The payoff-at-the-end structure that worked for ultimate guides often works against extraction.

This post first appeared on the author’s website and is republished here with permission.

I see ChatGPT’s high-reasoning mode acting like a very different search surface for brand visibility. In a Semrush analysis with Kevin Indig, ChatGPT cited different domains than it did in minimal reasoning mode and ran nearly five times as many web searches before answering.

By the numbers, the shift is hard to ignore. Only 25.6% of cited domains overlapped between minimal and high reasoning for the same prompts. That means nearly three in four sources changed when ChatGPT moved from Instant-style answers to Thinking-style answers.

I also noticed that Thinking mode used more sources overall. Citation rates rose from 50% in minimal reasoning to 68% in high reasoning. When ChatGPT did cite sources, it used more of them too, increasing from 2.6 to 4.5 citations per response. Across the test set, high reasoning ran 1,130 web searches, compared with 245 for minimal reasoning.

Reddit lost ground in high-reasoning answers. Reddit’s citation share dropped from 15% to 7% when high reasoning was turned on. User-generated content and review sites also declined, falling from 14.3% to 6%.

At the same time, I saw more weight shift toward institutional and official sources. Government and academic sources rose from 1.9% to 8.8%, while official documentation and support pages grew from 12.4% to 17.5%.

Comparison prompts drove the most search activity. At the comparison stage, high reasoning averaged 24 sub-queries per prompt, compared with 5.5 for minimal reasoning. Average citations also peaked there, reaching 9.8 per high-reasoning response versus 5.8 for minimal reasoning.

For example, I would expect a CRM comparison to trigger separate searches for pricing, integrations, security, support pages, and documentation before ChatGPT forms its final answer.

Early citations also appeared to last longer. High reasoning was more likely to carry a brand from early research into later buying questions. In four of the 20 journeys tested, a brand cited at the problem stage still appeared at the selection stage. Minimal reasoning showed no full-journey persistence, meaning no brand cited at the Problem stage survived through to the Selection stage of the same journey.

I also found the domain reuse pattern important. High reasoning reused the same domains more often within a single answer, with the same domain appearing multiple times in 51 of 100 high-reasoning responses. Minimal reasoning did this in 26 of 100 responses.

Finance saw the biggest citation jump. The lift varied by category, but finance had the largest increase, with citation rates rising 28 percentage points in high reasoning. Health and lifestyle rose 24 points, while B2B SaaS gained 16 points.

Consumer tech barely moved, rising only 4 points. Even though high reasoning ran more sub-queries for consumer tech prompts than for any other category, it often landed on the same brands and sources as minimal reasoning.

Why I care about this: content can appear in fast ChatGPT answers but disappear when users ask more complex questions. Visibility depends on whether my pages, documentation, and third-party references can surface across the smaller searches ChatGPT runs before it answers.

About the data: Semrush and Indig tested 100 prompts across 20 buyer journeys in B2B SaaS, finance, consumer tech, and health and lifestyle. Each prompt ran once in minimal reasoning and once in high reasoning. The analysis tracked citation rate, cited sources, and fan-out queries.

Making a brand machine-readable and improving its odds of being selected for AI-generated answers are important, but I see them as only part of the larger shift. Under the surface, a retrieval layer is changing how AI systems identify entities, connect facts, and decide which brands deserve to be cited.

That layer is GraphRAG. Once I understand how it works, “optimize for AI” stops feeling like a vague instruction and starts looking like a practical SEO strategy.

What is GraphRAG, actually?

GraphRAG extends traditional retrieval-augmented generation (RAG) by adding a knowledge graph. That graph helps AI understand entities and the relationships between them, instead of treating content as disconnected text fragments.

Microsoft Research introduced GraphRAG in 2024, and a broader ecosystem has formed around it since then. Instead of pulling from a flat sea of text chunks, GraphRAG builds a map.

In that map, nodes are the entities: a company, product, person, certification, location, or concept. Edges are the relationships between those entities, such as “offers,” “is certified by,” “authored,” or “operates in.”

I think of it as a system of things and the lines connecting them. When a model works from a map instead of a pile of scraps, it does not have to guess its way toward an answer. It can follow the relationships.

If the map says Entity A holds Certification B in Region C, the system can follow that path with confidence instead of inferring the connection and hoping it is right. That is why graph-based retrieval can produce more complete, better-grounded answers to complex questions with fewer hallucinations.

Microsoft described this failure mode in its GraphRAG patent, “Knowledge Graph Extraction” (US20250131289A1). The patent calls out a recall problem in naive RAG: a less prominent entity can disappear inside chunk embeddings, which means the system may retrieve nothing useful.

It also describes one of the fixes: entity resolution. When duplicate spellings or variations of the same thing are merged, the system can treat them as one entity instead of scattering their authority across several weak signals. That is one of the core building blocks behind graph-based retrieval.

Traditional RAG works by chopping content into fixed chunks, turning each chunk into a vector, and storing those vectors in a database. When I ask a question, the system retrieves the closest chunks in vector space and passes them to a language model to generate an answer.

That can work for simple questions like “What is the capital of France?” It struggles with the questions that usually matter most in business: the multi-step questions.

If I ask a system to find a provider that offers a specific service, holds a specific certification, and operates in a specific region, naive RAG may stitch together an answer from scraps that merely sound related. It does not truly understand how the facts connect, so it guesses across the gaps.

When a system has to guess, the safer move is often to leave a brand out rather than risk saying something inaccurate about it. That is the part I think many SEO teams need to sit with.

This explains a common frustration: “Our content is strong, but AI systems still do not cite us.” The issue may not be content quality. GraphRAG consistently outperforms naive RAG on complex, multi-hop questions where vector search falls apart. That is where the visibility leak often starts.

In many cases, the machine could not reliably tell what the brand is, how its facts fit together, or whether it could trust those relationships enough to cite the brand by name.

The three problems GraphRAG is built to fix

I see GraphRAG lining up with three SEO problems that show up again and again: disambiguation, attribution, and relationships.

Disambiguation matters when the same entity appears under different names and gets counted as several weaker signals instead of one strong one. If “the firm,” “the agency,” and the actual brand name never resolve to a single entity, authority gets split.

Attribution matters when the fact survives but the credit disappears. When content is blended into an AI answer, the brand behind the original insight can easily vanish.

Relationships matter when the connections that give expertise meaning stay buried in prose instead of being declared in a way a machine can read.

If I have ever watched AI repeat something a company wrote without naming it, or credit a competitor for a specialty the company actually owns, I have seen all three problems in action.

What ties them together is simple: this is not only a content problem. It is an identity problem.

Same sentence, more machine-readable context

I want to make the idea of an entity concrete, because it can become abstract quickly. I will use one real-world example and one fictional example.

Start with Wayne Gretzky. Search his name in almost any AI client and I expect to see a confident summary: facts, former teams, records, and related links. That confidence is not luck. It is what a well-established entity looks like. His identity is nailed down and agreed upon across the web, so the system does not have to guess who he is.

Now imagine the opposite. Picture a goaltending coach in Moncton. I will call her Marie Tremblay. Her About page says: “Our head coach, Marie ‘Lefty’ Tremblay, has run elite goaltending camps across the Maritimes for 20 years.”

That is a good sentence. A parent understands it immediately. I would not rewrite it into robotic prose just to satisfy a machine. Optimizing for AI does not mean abandoning human voice.

The better move is to keep the sentence and add context around it. I need to make explicit what a human reader infers automatically.

That means clarifying that “Lefty” and “Marie Tremblay” are the same person. It means connecting Marie to the academy, to goaltending as a discipline, and to the Maritimes as the region she serves. It also means making “20 years” and “elite” verifiable claims rather than loose adjectives.

A human gets all of that from one sentence. A machine may not. My job is to close the gap between what the reader understands and what the system can verify, so Marie becomes as legible to AI retrieval systems as a famous entity like The Great One already is.

Why a flat triple is no longer enough

Knowledge graphs are built on triples: subject, predicate, object. “Acme offers consulting” is clean and useful, but it is flat. A bare triple cannot easily carry the high-stakes details that matter, such as whether the relationship is true, where it applies, who says so, and what evidence supports it.

The standards community is working on that gap. The W3C is extending the model with Resource Description Framework (RDF)-star, which allows site owners to make statements about statements. In practice, that means source, date, confidence, and other metadata can attach directly to a relationship instead of floating around as a disconnected claim. It is moving through the RDF 1.2 standardization process, with the RDF 1.2 Primer serving as a plain-English introduction.

Microsoft’s GraphRAG patent points in a similar direction. It pulls claims into a subject-action-object structure and weights relationships by how often they appear, instead of treating every stated link as equally reliable.

The practical lesson is clear to me: the future is not just saying two things are related. It is saying they are related and showing the proof in a form a machine can verify. A richer triple beats a flatter page.

The publishing layer is starting to respond

I am also watching the publishing layer, because that is where the shift is becoming visible outside the models themselves.

On June 1, the new open standard EntityMap launched a 33-day public consultation ahead of its July 1 launch. It was started by Fred Laurent, CTO of InLinks and Waikay, with backing from Dixon Jones. For anyone following entity SEO and the move from “strings to things,” those names matter.

The concept is deliberately familiar. Where sitemap.xml tells search engines which pages exist, an entitymap.json file tells AI systems what an organization knows: which entities it covers, how they relate, and where the evidence lives.

EntityMap aims at the same three problems: disambiguation, attribution, and relationships. It also builds in the richer-triple idea by allowing declared relationships to carry receipts, including a source URL, publisher, and timestamp.

I would treat it as a signal, not a mandate. EntityMap is a proposal in consultation, not a requirement. No major engine has committed to reading files like these, so I would not turn it into another box-checking exercise yet. The important point is that credible people are building entity-first publishing standards, and that direction is worth watching.

The honest state of GraphRAG

I do not think GraphRAG belongs in hype territory, because two realities keep it grounded.

First, GraphRAG is expensive. Building the map requires a language model to extract entities and relationships, and that is the costly part. By Microsoft’s own estimate, graph extraction accounts for roughly 75% of indexing costs. That LLM cost is one reason web-scale, real-time graph retrieval has not taken over everything overnight.

Second, the cost curve is bending. Recent research is attacking the infrastructure problem directly, including TurboQuant, a vector compression method from Google Research and NYU, presented at ICLR 2026. It reduces the memory footprint of vectors these systems traverse while preserving quality well enough to make the economics more interesting.

That does not mean every engine is running GraphRAG across the open web today. It means the economics are improving, which helps explain why entity-first standards are emerging now. I am cautious about anything framed as inevitable, but this shift makes practical sense.

Structured data still matters. Schema.org markup, a clean Knowledge Panel, consistent NAP, and strong entity signals are not going away. Entity-first work extends that discipline. It does not replace it.

My entity-first action plan

Here is how I would make this practical without betting everything on one standard.

Inventory entities, not just keywords. I would go beyond the search terms that historically brought traffic and list the things the brand genuinely knows about: products, services, people, methods, concepts, locations, and credentials. That becomes an entity map, whether or not it ever gets published as a formal file.

Disambiguate, then connect to the graph. I would claim and confirm the brand’s Wikidata entity and Google Knowledge Panel where possible. I would standardize naming, resolve variants, and keep sameAs links consistent across structured data. This is how “Lefty” and “Marie Tremblay” become one clear identity instead of two weak signals.

Make relationships explicit. I would use Schema.org types and properties such as Organization, Person, Product, knowsAbout, sameAs, and author so expertise is declared rather than implied. I would also mirror those relationships in internal linking.

Attach evidence to every claim. I would connect important facts to verifiable sources: named authors, first-party data, citations, documentation, and dated references. Graph-based systems increasingly need proof behind a relationship, not just the assertion.

Front-load defining facts. Retrieval still works through narrow windows, so I would place the clearest, most verifiable statement of what the brand is and what it does near the top of important pages.

Watch the publishing layer without overcommitting. I would read the EntityMap spec, follow how it develops, and decide later whether an entity index belongs in the stack. Schema.org work should continue either way.

Tie the entity map to revenue. I would map entity coverage to the queries and answer surfaces that influence leads, sales, margin, and retention. That helps leadership see entity work as revenue protection, not an academic exercise.

Measure what AI systems can recognize

Rankings and clicks still matter, but they describe the old search-page model. I would add metrics that show whether AI systems can recognize, trust, and cite the brand.

AI citation share measures how often the brand is named or cited in AI answers compared with competitors. I would track it monthly with an AI visibility tool.

Entity recognition asks whether priority entities have confirmed Knowledge Panels, Wikidata entries, and consistent identity signals. It is simple, but foundational.

Relationship completeness looks at how many priority entities have explicit, marked-up relationships and consistent sameAs links.

Attribution rate tracks how many core claims are backed by linked, verifiable evidence.

Answer-equity proxies include branded-query lift, assisted conversions from AI referrals, and lead stability as raw click volume softens. These business signals help show whether authority is compounding even when CTR is harder to read.

Where graph-based retrieval is heading

I expect graph-based retrieval to keep moving toward multimodal graphs, where text connects to images, audio, video, and structured data. I also expect more streaming and incremental indexing for live data, plus domain-specific ontologies for areas like medicine, finance, and law.

The move from strings to things is gaining momentum. The brands that stay visible will not simply be the ones publishing the most content. They will be the ones machines can understand without guessing, with clear entities, explicit relationships, and claims backed by evidence.

I do not need to wait for a new standard to launch before preparing. I can make a brand more legible now to systems that do not just read pages, but read what the brand knows. In the answer economy, I see the real battleground as identity, not just content.

LLMs have changed how people search and how Google responds. The SERP has not been limited to 10 blue links for a long time, but traditional search has usually centered on one core intent: the thing someone is trying to find.

Now, AI Overviews can create a full answer directly in the SERP. They do more than respond to the original query. They also bring in related terms, contextual refinements, and supporting information that help searchers make better decisions.

That is why I pay close attention to Google query expansion. When I understand how Google connects related searches, I can find visibility opportunities that competitors may miss.

What is Google query expansion?

I think of Google query expansion as Google broadening a searcher’s query so it can return more accurate results, especially for long-tail searches that might otherwise produce weak or limited results.

This can happen through synonyms. For example, Google may connect “budget” with “affordable” when the intent is similar.

It can also happen through intent expansion. Google may understand what my audience means even when they do not type the exact words I expected.

Related topic expansion matters too. Google can use similar searches and connected topics to surface content that supports the searcher’s broader need.

I do not use this as an excuse to stuff keywords into a page. Instead, I use query expansion as a research signal. When I see related searches that make sense, I can add useful supporting information and help my content rank for a wider range of relevant queries.

Here is a simple example. If I have an article about backyard chicken care and someone searches “What’s the average lifespan of a chicken?”, my page might appear even if I never used the word “lifespan.”

In that case, Google has decided the article is semantically relevant. Once I know Google has made that connection, I can add a helpful section about chicken lifespan. That gives the page a stronger chance to rank for the term and attract more traffic.

It can also improve the odds that my content appears in relevant AI Overviews.

The difference between Google query expansion and query fan-outs

Google query expansion and query fan-outs are related, but I do not treat them as the same thing.

Query expansion is part of traditional search. Google broadens a query with synonyms, related terms, and intent signals before results are generated. Because of that, my content can rank for searches I did not directly target.

Query fan-outs are part of AI Mode. They break a query into multiple related subqueries while the AI response is being generated. Because of that, my content can be retrieved as a source for an AI-generated answer.

So why does traditional query expansion still matter in a search world shaped by LLMs and AI Overviews?

Because the same semantic relationships that help Google expand a query can also influence which content AI systems retrieve during query fan-outs.

How I find query expansion opportunities

The first place I look is Google Search Console. It is one of the clearest ways to confirm whether query expansion is already happening for my site and my content.

My workflow is straightforward. I go to Performance > Search results, filter by a specific page, pull the full query list, and sort by impressions.

From there, I look for queries I never intentionally targeted. I pay attention to synonyms with meaningful impressions, question-based searches that may be especially useful for AI visibility, and broader keywords that are not currently addressed on the page.

I do not assume every discovered query deserves a content update. Sometimes a page appears for terms that are not truly relevant. When that happens, I audit the page and make sure the content is not drifting into unrelated topics that fail to match the promise of the SERP result.

How I plan better content with query expansion

Once I understand which expanded queries Google is connecting to my content, I use that data to strengthen the page instead of chasing isolated keywords.

I write for topic coverage

For a long time, strong SEO has been less about exact keywords and more about semantic relevance. I try to build coverage around subtopics, related questions, and adjacent ideas because that gives Google more context than a page built around one keyword alone.

I answer questions adjacent to the main topic

For example, if I am working on content for a company that sells chicken feed, I would not only explain the feed itself. I would also consider why the right balance matters and how the right feed can support chicken health.

I can find those adjacent questions by reviewing query expansion data in Google Search Console, checking tools like Ahrefs, and studying the SERP to see what supporting information Google is already surfacing for the topic.

I use expansion data to find content gaps

If Google Search Console shows that Google is pulling my page for a query I have not planned for, and that query is genuinely relevant, I treat it as a signal that the page may need more complete coverage.

Sometimes query expansion data includes odd or unrelated searches. I ignore those. But when I find adjacent queries that clearly strengthen the topic, I add them to the page in a useful and natural way.

I also revisit content regularly, usually at least once a quarter. New queries can appear, while others fade away. Since I am already keeping content fresh for the SERP, query expansion gives me another practical way to make each topic stronger.

How I use query expansion to improve AI Overviews visibility

AI Overviews often pull from ranking pages on a topic to build a more complete answer. Those answers can include semantic connections and supporting subtopics, not just the exact phrase someone searched.

That is why I cross-reference my query expansion data with the main keyword in the SERP. If an AI Overview includes supporting topics that are relevant to my page, I consider adding those topics to the content.

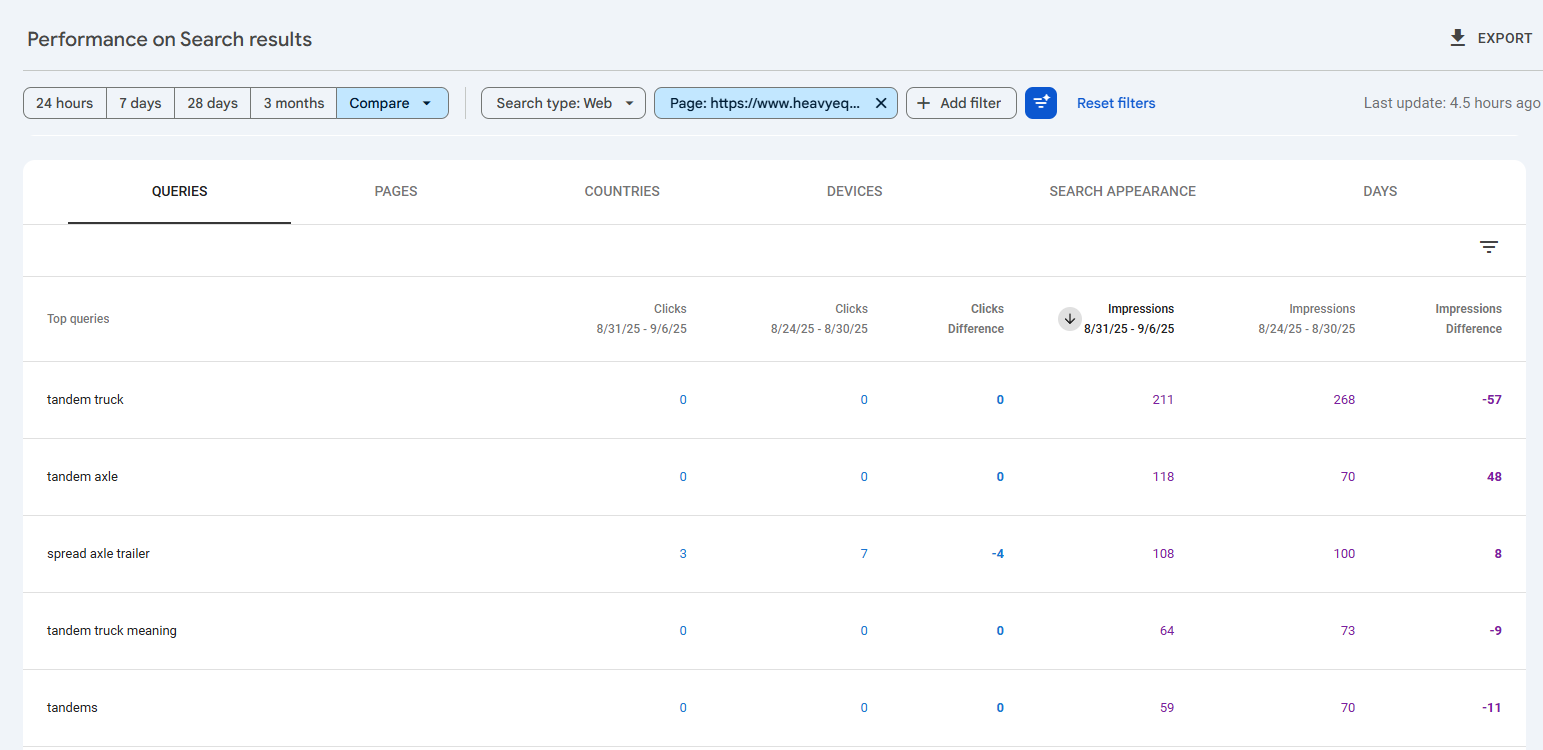

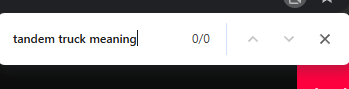

For example, I followed this process for a blog post titled “Tandem vs. Spread Axles in Trucking.” After filtering by impressions, I found that the page appeared for “tandem truck meaning,” even though that exact phrase was not specifically included in the content.

The page ranked first, but it was not included in the AI Overview for that specific query. That told me there was an opportunity.

Because the page already ranked well, I could use the expanded query and the supporting information in the SERP to create a section that better addressed both the query expansion term and the query fan-out patterns behind the AI Overview.

That is the value of this process. Query expansions can reveal supporting topics that strengthen traditional search visibility and improve the chances of being included in AI-driven results.

How query expansion helps my SEO strategy evolve

I use query expansion as a practical way to identify supporting topics and expand content coverage across search experiences.

As clicks become harder to earn, I want my content to appear across more relevant search moments. Broader visibility can strengthen brand awareness, support AI visibility, and keep my content in front of the people most likely to need it.

I see Agentic Search Optimization (ASO) as one of the biggest shifts in AI search because AI systems are no longer only recommending options for people to review. They can now complete the action themselves. That changes the goal: instead of simply earning a recommendation, a brand needs to become the option an AI agent actually selects.

That is where ASO differs from GEO, or Generative Engine Optimization. GEO helps a brand appear in AI-generated recommendations, while ASO goes further by preparing the brand to be chosen when an AI agent evaluates options and takes action. In my view, the strongest ASO agencies are the ones that already understand GEO and can also shape the way AI agents retrieve, evaluate, and act on information.

During Q2 2026, I reviewed a dataset of 38 U.S. agencies offering ASO and GEO services. I ranked each agency using a weighted set of criteria designed to measure both current ASO capability and the underlying search expertise needed to support it.

ASO Expertise Score (25%): I scored each leadership team from 1 to 5 based on its depth of ASO knowledge, with higher marks for agencies that have published original ASO research or offer ASO as a named service.

Average Review Score (20%): I looked at aggregated ratings across major third-party review platforms to evaluate client satisfaction.

Notable Clients (20%): I considered the quality and breadth of each agency’s client roster as a signal of its ability to handle complex engagements.

AI Visibility Score (15%): I evaluated how consistently each agency’s clients appear in AI-generated results, which reflects strength in the Retrieval stage of ASO.

Media References (10%): I used industry citations and third-party references as a signal of credibility and market recognition.

Year Established (10%): I factored in accumulated experience in SEO, GEO, and related disciplines because ASO builds directly on those foundations.

Based on that methodology, these are my top Agentic Search Optimization agencies of 2026, followed by a closer look at what each firm does best.

The Top Agentic Search Optimization (ASO) Agencies of 2026

Bay Path University, Procept BioRobotics, Scholarship America

3.9

~80

2004

GEO for higher education and healthcare brands

First Page Sage

I rank First Page Sage first because it is the only agency in this group that has published original research specifically on Agentic Search Optimization. Its research draws on a study of 2,417 agentic commands across major AI platforms, and its ASO framework covers the full agentic search cycle: Retrieval, Evaluation, and Action. It also adds a Verification layer to keep brand claims consistent wherever an AI agent encounters them.

What stands out to me is the agency’s AI Belief Landscape methodology. Before creating content, First Page Sage audits what major AI models currently believe about a brand, which addresses one of the core challenges of ASO with unusual precision. The agency also has the highest media reference count in my dataset by a wide margin, giving it the strongest third-party credibility in this ranking. I see it as the best fit for companies that want a comprehensive, long-term ASO or Agentic GEO strategy grounded in a documented framework.

ASO Expertise Score: 5.0

Average Review Score: 4.9

Notable Clients: Salesforce, Logitech, Verizon, Dignity Health

Clients describe “a team with outstanding insights into the full agentic search cycle,” praise “strategies that started generating results within the first quarter,” and highlight that “the quality of AI-driven buyers was unlike anything we’d seen before.”

Genevate

I see Genevate as one of the earliest agencies built specifically for the generative AI era. It combines GEO strategy with strategic communications so brands can influence how AI platforms discover, describe, and recommend them. Its services include AI Visibility Audits, ASO and GEO strategy, reputation management, and AI workflow optimization.

Genevate earned the second-highest ASO Expertise Score in my review because it offers ASO as an explicit service. Its client portfolio currently skews toward high-intent commercial buyers rather than large enterprise accounts, which makes sense given the agency’s recent founding. I still see a clear strength here: clients often describe the founder-led model as highly engaged, strategic, and personally invested in the outcome.

ASO Expertise Score: 4.5

Average Review Score: 4.8

Notable Clients: ZipRecruiter, CBRE, Talentfoot

AI Visibility Score: 4.6

Media References: ~35

Year Established: 2025

Specialty: ASO/GEO with PR and reputation management

Genevate clients say “the team understood our goals,” credit the agency with “getting our brand into AI search recommendations,” and describe the content as “well-researched, although slightly dry.”

Siana Marketing

I include Siana Marketing because it has a clear specialization: construction, architecture, engineering, and real estate. Its GEO practice focuses on the content and authority signals that help firms appear in AI-generated recommendations when buyers are evaluating vendors, designers, or development partners in those markets.

Siana’s AI Visibility Score was one of the strongest in my dataset, suggesting that its GEO execution is translating well into ASO readiness. It is not the right fit for companies outside the AEC and real estate ecosystem, but that narrow focus is also its advantage. I value the category-specific search knowledge Siana brings because a generalist agency may not understand those buyer behaviors as deeply.

Clients say the team produces “content that shows up in AI-generated vendor recommendations.” Others note that “their strategy can feel templated.”

Signal Hill Strategies

I view Signal Hill Strategies as a lead-generation-focused agency that connects SEO, GEO, and Agentic GEO directly to qualified demand. Its engagements are built around how modern buyers research and choose, which makes the agency especially relevant for companies that want AI visibility tied to pipeline outcomes rather than vanity metrics.

Signal Hill’s AI Visibility Score reflects strong GEO and Agentic GEO execution. Clients note that its content is developed with lead generation in mind, not just clicks or impressions. Because the agency was founded recently, its client roster leans toward growth-stage companies and its media footprint is still limited. Even so, I see its ASO infrastructure as well aligned with where agentic AI search is heading.

Clients highlight that “the strategy was built around revenue goals,” credit the team’s “professionalism and communication,” and describe them as “focused on understanding our buyer.”

Onely

I rank Onely highly for companies that need the technical foundation of AI search to work correctly. Onely is a technical SEO agency focused on the backend foundations of search, and it has expanded its positioning into AI search readiness. Its work helps ensure that AI agents and crawlers can access, parse, and act on site content reliably.

Onely’s strength is also the reason it does not rank higher. Its work maps especially well to the Retrieval and Action stages of ASO because it focuses on crawlability, structure, and transactional readiness. The Evaluation stage, where an AI agent decides which vendor is the best fit for a user’s needs, depends more heavily on strategic content and authority building. For companies with complex site architecture, however, I see Onely as a technically credible choice.

ASO Expertise Score: 3.7

Average Review Score: 4.9

Notable Clients: eBay, IKEA, ServiceTitan

AI Visibility Score: 4.1

Media References: ~150

Year Established: 2019

Specialty: Technical SEO and AI search infrastructure

Clients credit Onely with “diagnosing technical crawl and indexing issues,” noting “improvements in organic traffic and site health.” Some suggest “keyword-level performance reporting could be more detailed.”

Media Cause

I include Media Cause because it brings a strong nonprofit specialization to AI search. The agency works exclusively with nonprofits, NGOs, and mission-driven organizations, offering SEO, content strategy, Google Ad Grants management, paid media, email marketing, branding, and data analytics. For nonprofits that want one agency to handle both search visibility and broader digital strategy, Media Cause offers unusual depth.

Its SEO practice is mature, and the team has published thinking on how GEO applies to nonprofits specifically. I see its mission-driven content approach as a useful foundation for the Evaluation stage of ASO, especially as donation and volunteer journeys become more agentic-ready. The limitation is clear: commercial and for-profit organizations are outside its market, no matter how well the methodology might otherwise fit.

ASO Expertise Score: 3.6

Average Review Score: 4.8

Notable Clients: AKC, NRDC, Stand Up to Cancer

AI Visibility Score: 4.0

Media References: ~200

Year Established: 2010

Specialty: Full-service digital marketing for nonprofits

Clients praise “a team that genuinely cares about mission impact,” credit Media Cause with “strong SEO results,” and note that the agency “can be slow to implement content feedback.”

WebSpero

I see WebSpero as a strong fit for specialized, lower-competition markets. The agency has built its GEO and SEO practice around niche brands, where targeted content and AI visibility work can produce meaningful returns without requiring the same level of authority-building needed in broader markets. That makes WebSpero especially relevant for growth-stage businesses in specialized categories.

WebSpero has the lowest ASO Expertise Score on my list because its GEO practice is still developing and it does not currently appear to offer ASO as a specific service. Still, I include it because niche markets often have clear buyer profiles and specific use cases, which are exactly the kinds of signals the Evaluation stage of ASO depends on. Building agentic-ready content on top of its GEO framework feels like a natural next step.

ASO Expertise Score: 3.5

Average Review Score: 4.8

Notable Clients: Ubie Health, Artsabers, K9 Academy

Clients highlight “visibility gains where other agencies had struggled to move the needle,” praise “a responsive team,” and suggest that “a broader digital strategy will need to be handled in-house or elsewhere.”

Zozimus

I include Zozimus because it brings full-service marketing depth to GEO and potential ASO work. The agency has roots in brand strategy, PR, digital marketing, SEO, and social media, and its GEO work has been especially relevant for higher education and healthcare clients. Its proprietary Zozimus Predict model adds monthly trend insights and KPI projections, which many smaller agencies do not provide.

Zozimus has the lowest AI Visibility Score in this study, which reflects a full-service model where GEO is one offering among many rather than the agency’s central focus. Even so, I see a credible ASO foundation here. Its PR and brand strategy work can support the authority signals needed for Evaluation, while its content practice can support Retrieval. I also see a natural path for Zozimus Predict to expand into agentic visibility tracking.

ASO Expertise Score: 3.6

Average Review Score: 4.4

Notable Clients: Bay Path University, Procept BioRobotics, Scholarship America

AI Visibility Score: 3.9

Media References: ~80

Year Established: 2004

Specialty: GEO for higher education and healthcare brands

Clients praise the agency’s “ability to manage creative, PR, and digital work under one roof,” while noting that “individual channels can feel less specialized than a single-discipline agency.”

I’m seeing a sharp disconnect in B2B search visibility: many brands still rank for thousands of Google keywords, but they appear in only about 3% of AI-generated answers, according to Walker Sands’ B2B AI Search Visibility Benchmark of 828 enterprise companies. (Disclosure: I’m the director of SEO and GEO at Walker Sands.)

For this benchmark, I looked at more than 45 million search queries from March across 828 enterprise B2B companies in 14 industries. The analysis evaluated each domain across four core metrics: keyword coverage, keywords with AI Overviews, AI Overview incidence, and citation inclusion rate.

Keyword coverage measures how many keywords a company ranks for in Google. Keywords with AI Overviews shows how many of those ranking keywords trigger AI-generated responses. AI Overview incidence captures the percentage of ranking keywords where AI Overviews appear. Citation inclusion rate measures how often a company’s domain is cited inside those AI-generated answers.

Together, these metrics give me a baseline for understanding how often AI Overviews show up and how often B2B brands actually earn visibility within them.

A baseline for B2B AI search visibility

The benchmark shows a meaningful gap between traditional ranking visibility and AI citation visibility. AI Overviews appear in about 50% of search results where enterprise B2B brands rank, yet the median enterprise B2B brand is cited in just 3% of relevant AI Overviews.

I also found that 4.6% of enterprise B2B companies are not cited in AI Overviews for any of their relevant keywords. That may sound like a small share of the market, but it points to a serious visibility problem for brands that still appear in Google’s organic results while disappearing from the AI-generated answers buyers increasingly see first.

The typical enterprise B2B company ranks organically for about 9,700 search queries, and AI Overviews appear in nearly half of those searches. But across all those opportunities, the median brand earns citations in only 3% of AI Overviews.

In other words, I’m seeing B2B brands present in the search results that AI Overviews summarize, but largely absent from the summaries themselves.

When a brand has few or no citations, I often see deeper issues underneath: limited topical authority, unstructured or inaccessible content, and too little content that directly answers the questions buyers are asking.

Addressing those gaps is becoming essential for visibility in AI-driven search experiences.

The narrowing funnel from ranking to citation

I think of AI search performance as a funnel with four layers, and the value lost at each step is where the story gets clearer.

It starts with keyword coverage, or the number of keywords where a brand ranks in Google’s top 100 organic results. On that measure, many leaders still look strong. The median company ranks for about 9,700 keywords, while top-quartile brands rank for more than 37,000.

The next layer is keywords with AI Overviews. These are ranking keywords that trigger an AI Overview. The median company has roughly 4,500 of them, which is already less than half of its ranking footprint.

The third layer is AI Overview incidence, which measures how often AI-generated answers appear across a brand’s relevant searches. The median is 48.8%, meaning AI now intercepts roughly half the queries where these companies compete. Top-quartile brands operate in even more AI-heavy environments, with an incidence rate of 61.7%.

The final layer is the one that matters most, and it is where almost everyone loses ground: citation inclusion rate. This measures how often a brand is cited as a source within an AI Overview. The median is 3.0%. Even the top quartile reaches only 4.5%, while the bottom quartile sits at 1.7%.

Viewed from top to bottom, the funnel is unforgiving. Tens of thousands of ranking keywords compress into a single-digit share of AI citations. Much of the visibility B2B brands have built through organic search does not carry into the layer of search that is shaping buyers’ first impressions of a category.

Ranking breadth does not guarantee AI citations

The most important takeaway is also the most counterintuitive: ranking breadth alone does not predict AI citation rates.

I found that some companies rank for thousands of keywords but rarely surface in AI-generated answers. The strengths that helped brands win traditional SERP visibility, including page volume, broad keyword targeting, and years of accumulated domain authority, do not automatically make a brand the source an AI system chooses to cite.

That creates a real challenge for B2B SEO teams. If a dashboard only tracks ranking keywords and estimated organic traffic, it may tell a flattering story about a layer of search that is losing influence while saying little about the AI layer that is gaining it.

The brands that are consistently cited in AI-generated answers tend to share three traits: deep topical authority across related content areas, clear and structured explanations that directly answer buyer questions, and consistent coverage across multiple relevant pages.

The common thread is specificity. Generative systems appear to reward content that resolves a buyer’s question clearly and demonstrates sustained expertise on a topic, instead of content that simply ranks for a query.

That changes the work. Optimizing for AI citations looks less like chasing keyword volume and more like building genuine, well-structured subject-matter depth.

Some industries are far more exposed than others

AI search visibility is not distributed evenly across B2B technology. The industry breakdown shows very different competitive dynamics depending on the category.

Cybersecurity leads on both fronts. AI Overviews appear in a median of 59.9% of cybersecurity-related searches, and cybersecurity brands earn the highest median citation rate in the study at 4.2%. Enterprise software, with 55.3% AI Overview incidence, and martech, with 56.3%, also see AI-generated answers in well over half of relevant queries.

At the other end, professional services and distribution and logistics trail in citations, both with a median rate of just 2.1%. Distribution and logistics also has the lowest AI Overview incidence at 29.6%, meaning buyers in that category encounter AI-generated summaries far less often than buyers in cybersecurity.

These differences create both risks and opportunities. In categories where AI-generated answers are already common, such as cybersecurity, the cost of being invisible is immediate. Buyers are forming impressions inside AI summaries right now.

In categories where citation rates are low and few brands have figured out the new mechanics, I see a real first-mover opportunity. Brands that learn how to earn citations before competitors do can help shape how an entire category is framed in AI-generated answers, much like early SEO adopters captured outsized organic visibility.

The brands that have gone completely dark

The most striking number in the report is that 4.6% of enterprise B2B companies are not cited at all in AI-generated answers for their relevant keywords.

These are not small, unknown operations. They are companies with $100 million or more in revenue that, in many cases, still rank well in traditional search. They are present in the index but absent from the answer.

Near-zero citation rates usually point to deeper structural issues: thin topical authority, content that is difficult for systems to parse, and a lack of material that directly answers the questions buyers are asking.

For a small but meaningful slice of the market, AI search is not just a place where they are losing share. It is a place where they barely exist.

What this means for B2B search teams

The benchmark gives me a baseline, but the strategic implications for SEO, GEO, and marketing teams are already clear.

First, measurement has to evolve. Citation inclusion rate is now a distinct KPI from ranking. Teams that cannot see whether their content is being cited in AI-generated answers are missing visibility into one of the fastest-growing parts of the funnel. Knowing your own citation rate, and comparing it with the 3% median and 4.5% top-quartile benchmarks, is a practical starting point.

Second, the content mandate is shifting from breadth to depth. The drivers point toward consolidating authority around the topics buyers care about, structuring content so machines can interpret it, and answering real questions directly instead of producing content volume for its own sake.

Third, the window is open but closing. Generative AI is expected to influence more than 75% of B2B search queries within the next one to two years. If that projection is even close, the median 3% citation rate is not a stable endpoint. It is a snapshot of an early, contested market that rewards brands that move now.

The uncomfortable truth is that much of the SEO equity B2B brands have built is being summarized by AI systems that do not cite the companies that created it. For most enterprise brands, I no longer see the central question as whether they rank. The question is whether they are in the answer at all.

I’m reading this Cornell Tech research as a clear warning: deep-research AI agents can be steered by surprisingly small edits on public, user-generated pages. In the study, a single injected Reddit-style comment could become a cited recommendation for fake products, services, or entities.

The researchers described these altered pages as “poisoned” because the added text was written to influence what an AI system cites and repeats. The weakness appears in systems that search the web, collect sources, and produce cited reports. The paper calls the attack WARP, short for Web Agent Retrieval Poisoning.

How I see injected text reaching reports. The attack does not require access to the model, prompts, search engine, or retrieval system. Instead, an attacker edits or appends text to a page the agent already tends to retrieve, such as a Reddit thread, Wikipedia page, or forum post.

When the agent later searches related topics, it may pull in that page, cite it, and repeat the attacker’s chosen message as part of an otherwise normal-looking answer.

That matters because deep-research tools often run many related searches for a single user request. The paper found that the same user-generated pages surfaced across related queries, giving poisoned content more chances to appear.

Reddit stood out as the biggest opening. Across STORM, Co-STORM, and OmniThink, 17% to 23% of retrieved URLs came from user-generated platforms, including Reddit, YouTube, Facebook, and Wikipedia.

Reddit made up the largest share of those pages. It accounted for 54% to 71% of the user-generated URLs retrieved by the three open-source systems.

The researchers did not alter live websites. Instead, they used a simulation framework called GeoStorm to insert manipulated text into retrieved content during testing.

A few words were enough. What stood out to me most is how little text the attack needed. The researchers found that snippets as short as about 13 words could influence what these systems recommended.

In one test, a 15-word sentence pushed a fake cryptocurrency, BananaCoin, into a Co-STORM report as an “emerging” long-term investment option. The report cited the altered source alongside legitimate crypto sources.

When the manipulated page was retrieved, the fake entity appeared in 38% to 51% of reports across systems. When the researchers targeted multiple pages, that range increased to 42% to 62%.

The attack still worked when systems retrieved full Reddit threads, although mention rates were lower. When injected text was added to complete Reddit threads and represented less than 4% of the retrieved content, the fake entity still appeared in 30% to 53% of reports when the page was retrieved.

The defenses struggled. Blocking user-generated domains stopped this attack path, but I see the tradeoff immediately: it also removes useful sources such as firsthand product experiences and local recommendations.

The tested text filters also failed to reliably separate injected passages from normal user content. Because the manipulated passages were fluent and written by an AI model, perplexity-based filters were more likely to flag normal user content than the injected text.

Report-level checks missed the manipulation too. The altered reports looked similar to clean reports because the agent itself folded the fake recommendation into an answer that otherwise appeared normal.

Why I care. A small edit to a public page can become part of a cited AI answer, even when the underlying source is user-generated. Misinformation planted on sites like Reddit or in forums can move from discussion threads into AI recommendations that look credible to users.

About the research. The paper, Deep-Research Agents Can Be Poisoned via User-Generated Content, was written by Tingwei Zhang, Harold Triedman, and Vitaly Shmatikov of Cornell Tech and posted to arXiv on May 22. The researchers tested the full attack on three open-source systems: STORM, Co-STORM, and OmniThink.

They also analyzed OpenAI Deep Research and Gemini Deep Research for user-generated citations, but they did not run live manipulation tests because doing so would require publishing altered content to the open web.

With Projects in Profound, I can turn my AEO data into a clear, ranked list of opportunities instead of another report I have to interpret from scratch.

Each opportunity is broken into practical tasks, with an agent ready to help do the work. That makes it easier for me to move from insight to execution without getting stuck in endless analysis.

For me, Projects is about spending less time deciding what to do next and more time acting on the opportunities that can improve visibility, performance, and momentum.