A year ago, I saw 82% of consumers say AI-powered search was more helpful than traditional search. By 2026, that number had fallen to 54%, a 28-point drop in sentiment in just 12 months.

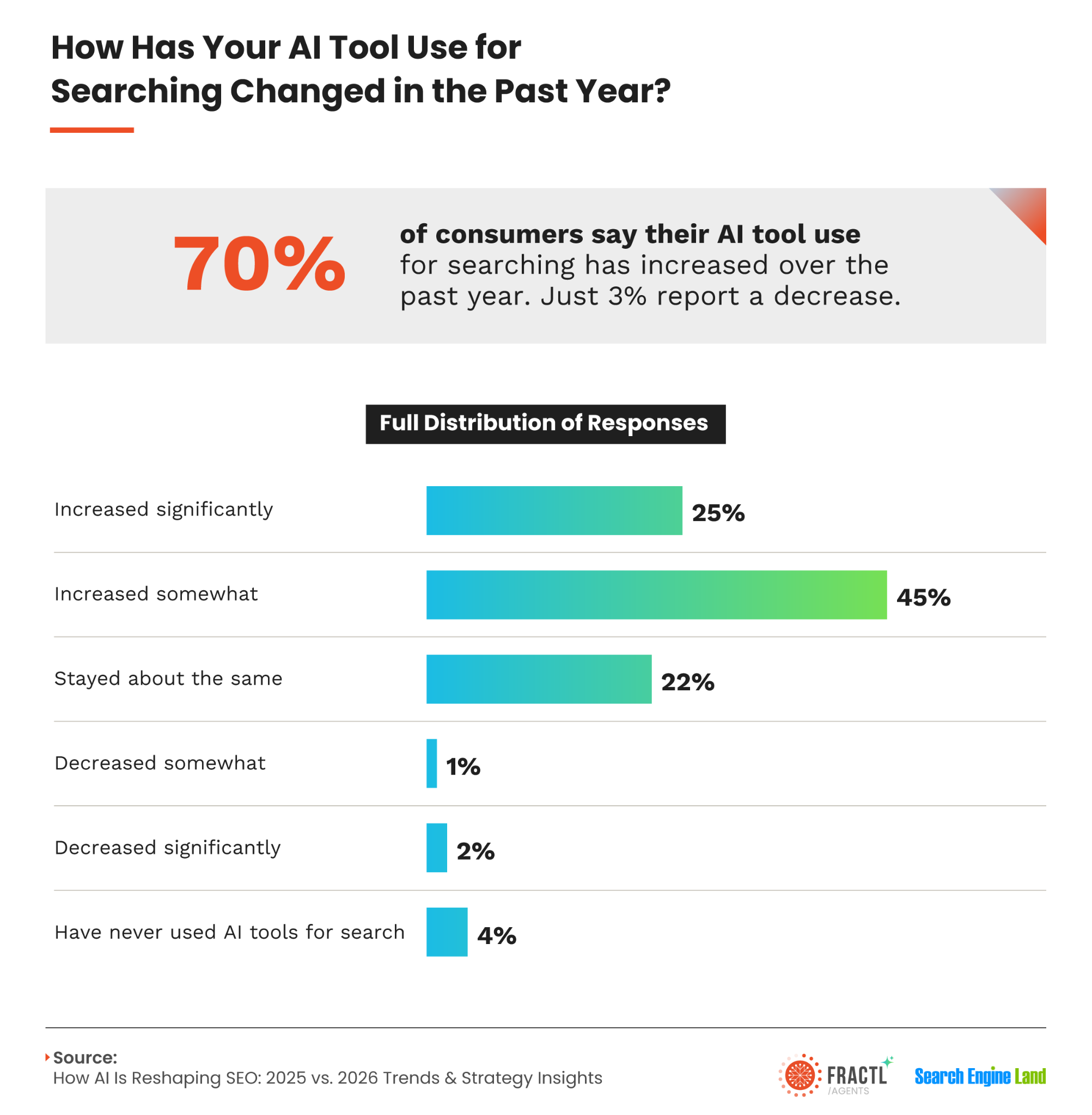

That does not mean people are abandoning AI search. In fact, 70% of consumers say they are using AI tools for search more than they did last year. The tension is clear: adoption is rising, but trust is slipping.

That is the core issue I believe search marketers need to solve in 2026. It is no longer enough to appear in AI answers. I need my brand, and the brands I work with, to be visible, accurate, credible, and trusted when AI systems surface information.

To understand the shift, Fractl partnered with Search Engine Land to expand our 2025 research. We surveyed 1,008 U.S. consumers and 150 marketers to compare how consumer trust, marketer adoption, and brand strategy are changing in the AI search era. Disclosure: I am the co-founder of Fractl.

Here is what I believe the data means for 2026 search strategy.

Consumers are using AI more, but trusting it less

AI search adoption is no longer the main story. Seventy percent of consumers report increased use of AI tools for search over the past year, while only 3% say their use has decreased. The bigger question is whether people trust what those tools return.

One surprising finding is that baby boomers now find AI more helpful than Gen Z, 63% to 47%. That challenges the assumption that younger users automatically embrace AI while older users lag behind. What I see instead is a more complicated market where trust has to be earned across every generation.

In 2025, only 3% of consumers said AI was less helpful than traditional search. By 2026, that skeptic group had grown to 17%, nearly six times larger than the year before. Even among the 54% who still find AI helpful, enthusiasm is softer: 37% say it is only somewhat more helpful, while 17% say it is much more helpful.

I think hallucinations and low-quality AI content are changing how people evaluate the entire channel. Consumers may use AI because it is convenient, but convenience does not automatically create confidence.

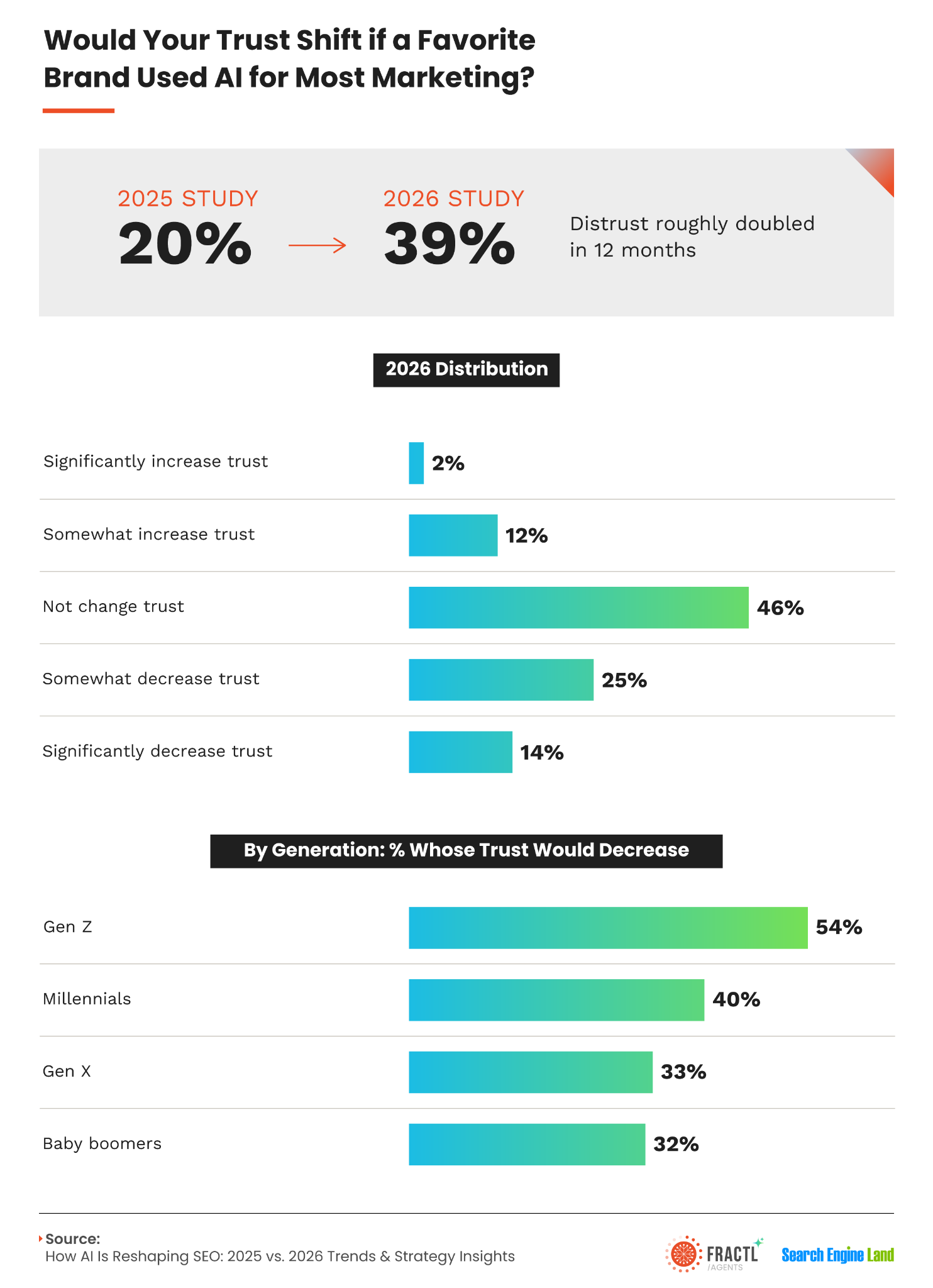

AI content volume has become a brand trust risk

In 2025, 20% of consumers said heavy AI use would reduce their trust in a brand. In 2026, that number rose to 39%. For me, that makes AI content scale a reputational issue, not just an operational decision.

If I publish AI-assisted content at scale without disclosure, strong editorial standards, or obvious quality signals, I am asking my audience to trust a process they are increasingly skeptical of. That is a risk more brands need to take seriously.

Gen Z is especially strict. Fifty-four percent of Gen Z consumers say heavy AI use in a brand’s marketing would decrease their trust, compared with 32% of baby boomers and 33% of Gen X. Women are also more likely than men to penalize brands for heavy AI use, 44% vs. 34%.

That matters because Gen Z is often the audience most likely to engage deeply, share content, shape online conversations, and influence long-term organic visibility. If that audience matters to a brand, AI-generated filler is not a harmless shortcut.

Disclosure is now a consumer expectation

Across every major content format, more than 80% of consumers want AI-generated content labeled. Video leads at 91%, followed by images at 90%, audio at 87%, and written content at 84%. More than half of respondents strongly agree with labeling in every category.

I do not read that as a mild preference. I read it as a near-universal expectation. The brands that treat AI disclosure as optional are creating a gap between how they operate and what their audiences want.

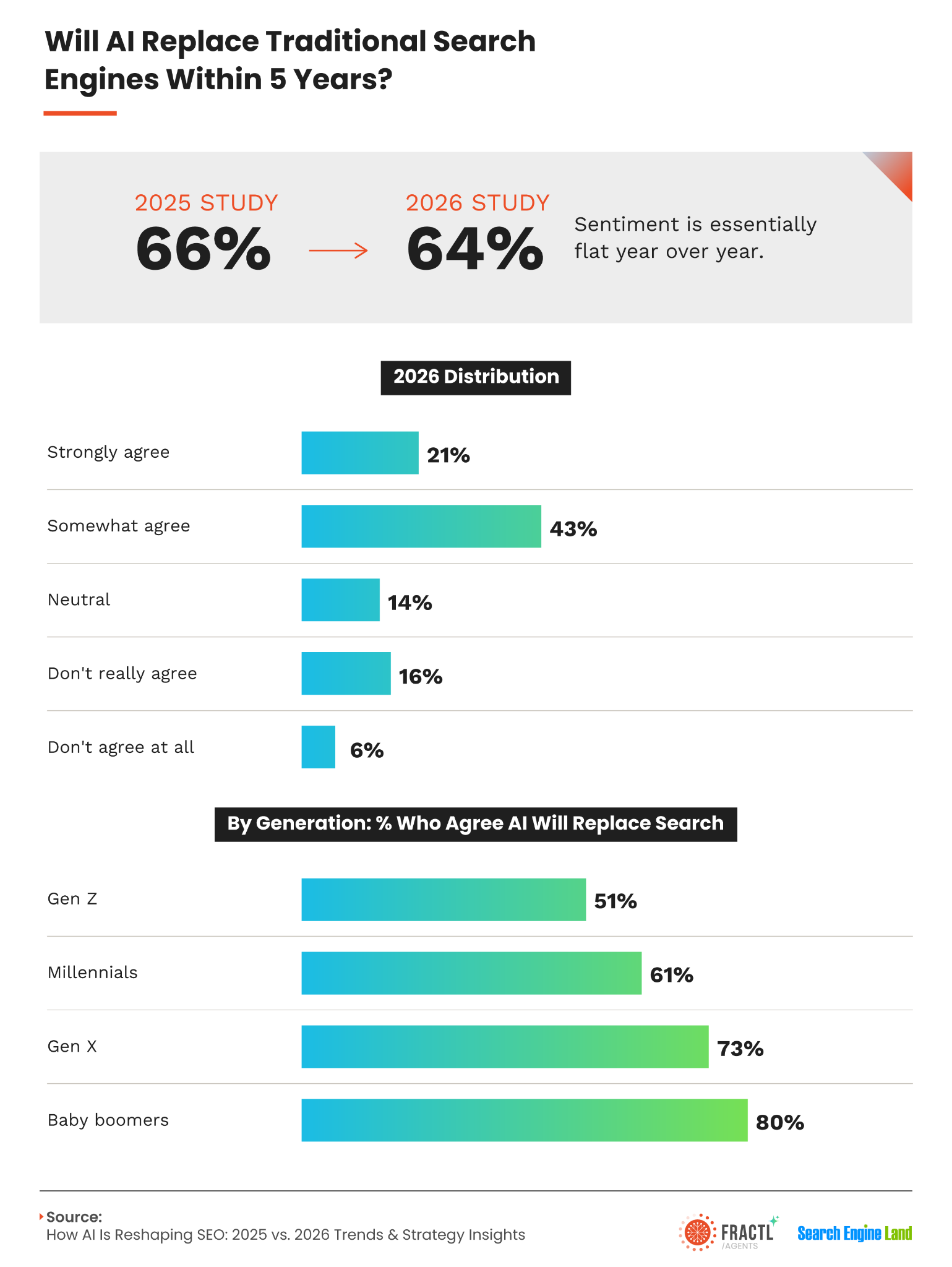

Consumers still believe AI will shape the future of search. Sixty-four percent agree that AI will replace traditional search engines within five years, nearly unchanged from 66% in 2025. The channel is not going away. But being present in AI results and being trusted in AI results are now two different challenges.

Google still leads on trust, especially for buying decisions

When consumers are making purchase decisions, 39% turn to Google first. Reddit follows at 15%, AI tools at 14%, and review sites and friends or family each at 11%. The trust people have built with Google has not automatically transferred to AI tools.

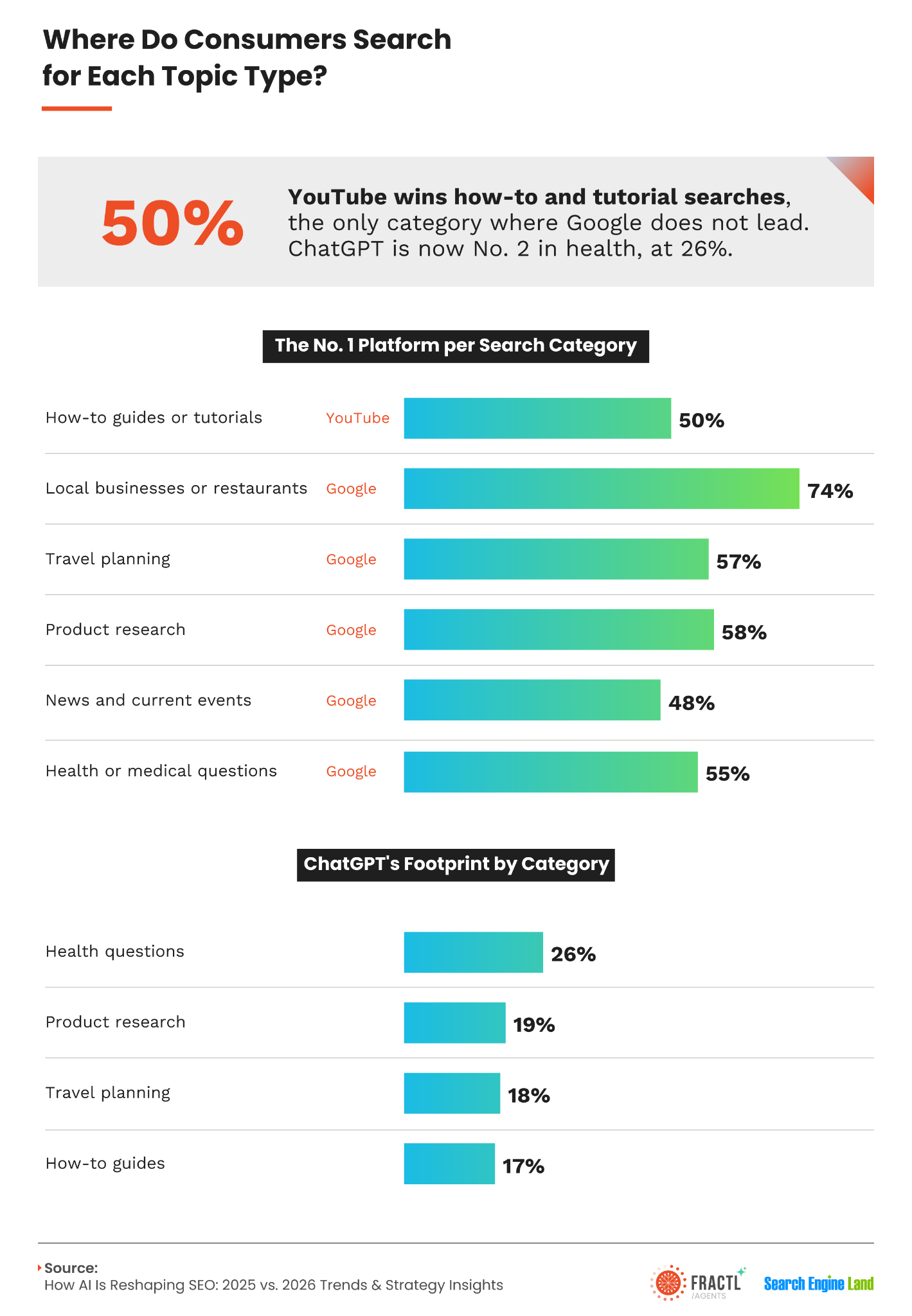

Platform preference also changes by query type. Google dominates five of six major search categories. It is the first stop for local businesses, product research, travel planning, and health questions. YouTube overtakes Google for how-to content, while ChatGPT is now the second-most-used destination for health questions and ranks strongly for product research, travel planning, and how-to content.

That tells me there is no single AI search platform to optimize for. I need to map content strategy to actual user behavior: where people search, what they are trying to decide, and which platforms influence confidence at each stage.

Before making a purchase decision, the average consumer checks 2.4 platforms. Gen Z checks 2.5, millennials 2.4, Gen X 2.3, and baby boomers 2.2. This behavior is consistent enough that I now think of search optimization as a multi-platform visibility strategy, not a rankings-only discipline.

A brand that appears in Google results but nowhere else can lose to a brand that appears in Google, shows up in Reddit discussions, gets cited by ChatGPT, and has strong third-party review content. Visibility now has to travel with the buyer.

AI is changing marketing operations quickly

AI now touches 53% of marketing work on average, up from 38% in 2025. In practical terms, the equivalent of one full workday per week has shifted to AI-assisted workflows in just 12 months. Fifty-nine percent of marketers say AI is involved in at least half their work, while 27% say it is involved in three-quarters or more.

For SEO and content teams, this means competitors are moving faster. But speed alone is becoming commoditized. Accuracy, original insight, expert judgment, and brand credibility are much harder to copy.

Marketers are also feeling pressure to adopt AI. Fifty-five percent of marketing roles report a 7-out-of-10 level of pressure to use it. SEO and analytics teams feel that pressure most, while PR is not far behind. As AI makes generic content easier to produce, the advantage shifts toward what AI cannot automate well: judgment, relationships, trust, and reputation.

The quality tradeoff is real. Only 26% of marketers say AI made their work both faster and better. Nearly half say it made their work faster but more generic, and 7% report an outright quality decline.

That is where I see a major competitive opening. If other teams are scaling generic AI content while I invest in original data, expert quotes, third-party validation, and earned brand mentions, I am building assets that are more visible, credible, and retrievable across search engines, social platforms, and LLMs.

AI governance is still too weak

About three in four organizations conduct human editorial review before publishing AI-generated content. Sixty-two percent check for brand voice, 54% check facts, and 42% conduct legal or compliance review. Only 27% evaluate content for bias.

That means nearly half of AI-generated content may enter the market without fact-checking, legal review, or plagiarism checks. Too many teams are still relying on surface-level review: Does it sound right? Is the tone appropriate? Are there typos?

In a year when consumers are already prepared to distrust generic AI content, I see governance as one of the cheapest gaps to close and one of the most expensive to ignore.

The disclosure gap is just as serious. Heavy, generic AI use is now a brand-trust liability, yet only 20% of organizations always disclose AI use to their audiences. Compare that with the 84% average consumer demand for labeling written content, and the disconnect is obvious.

The takeaway is not to abandon AI. It is to stop treating governance as optional. Every AI workflow needs accuracy checks, transparency standards, bias review, and human accountability before content reaches an audience.

AI hallucinations are already a brand problem

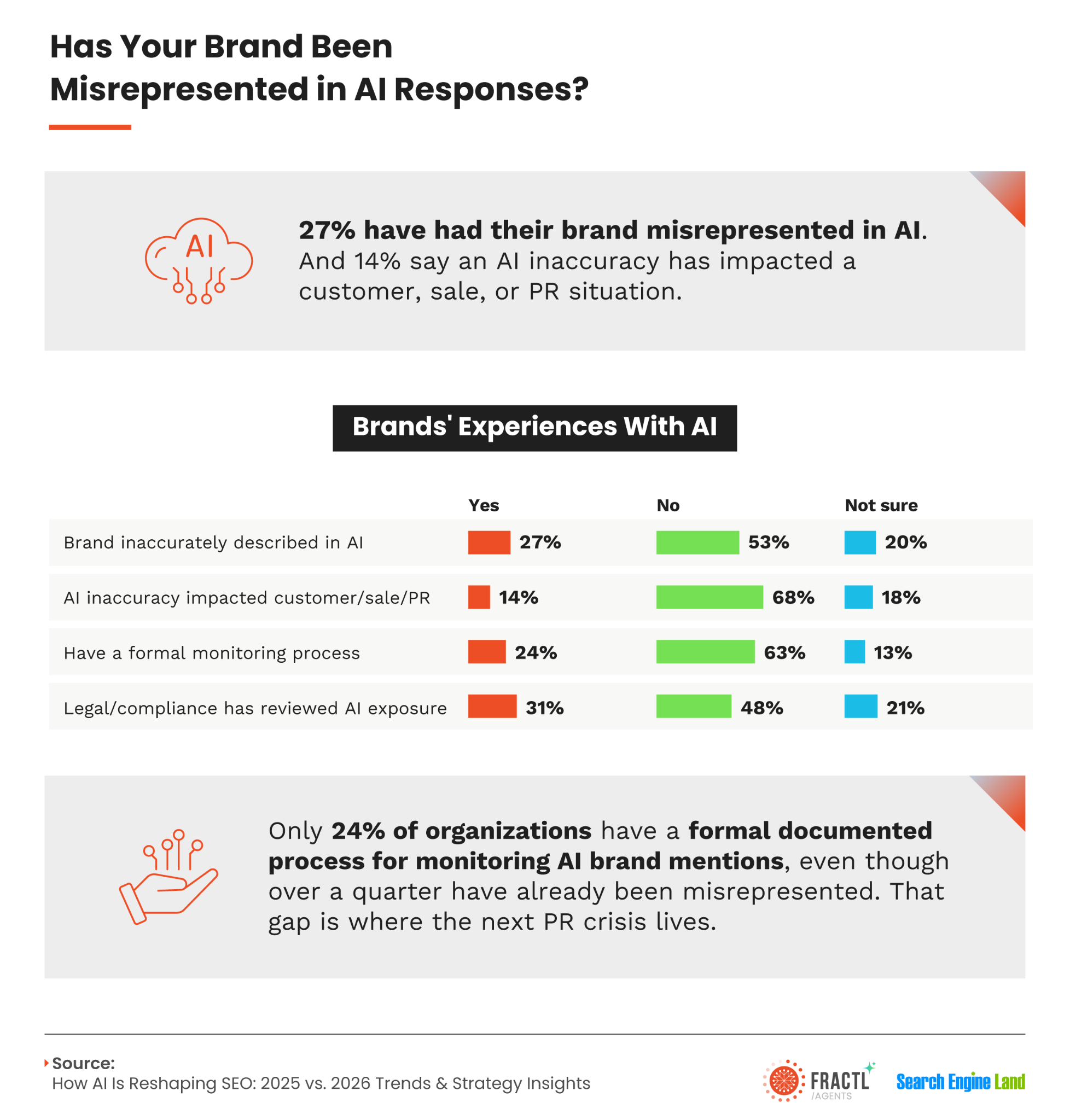

A year ago, about 22% of marketers tracked LLM visibility. In 2026, that figure barely moved to 24%. At the same time, 27% of brands have already been misrepresented in AI-generated responses, and 14% say an AI inaccuracy has affected a customer relationship, sale, or PR situation.

More brands have been misrepresented by AI than have a formal monitoring process. That should concern every search and communications team.

If AI is summarizing my category, comparing my product, or explaining my brand incorrectly, that is not only an SEO issue. It is a reputation risk, a revenue risk, and a PR issue waiting to escalate.

When AI misrepresents a brand, I believe fixing the source matters more than arguing with the output. That can mean reaching out to publishers for updates, correcting owned profiles, improving brand pages, and publishing clear correction content tied to the entity.

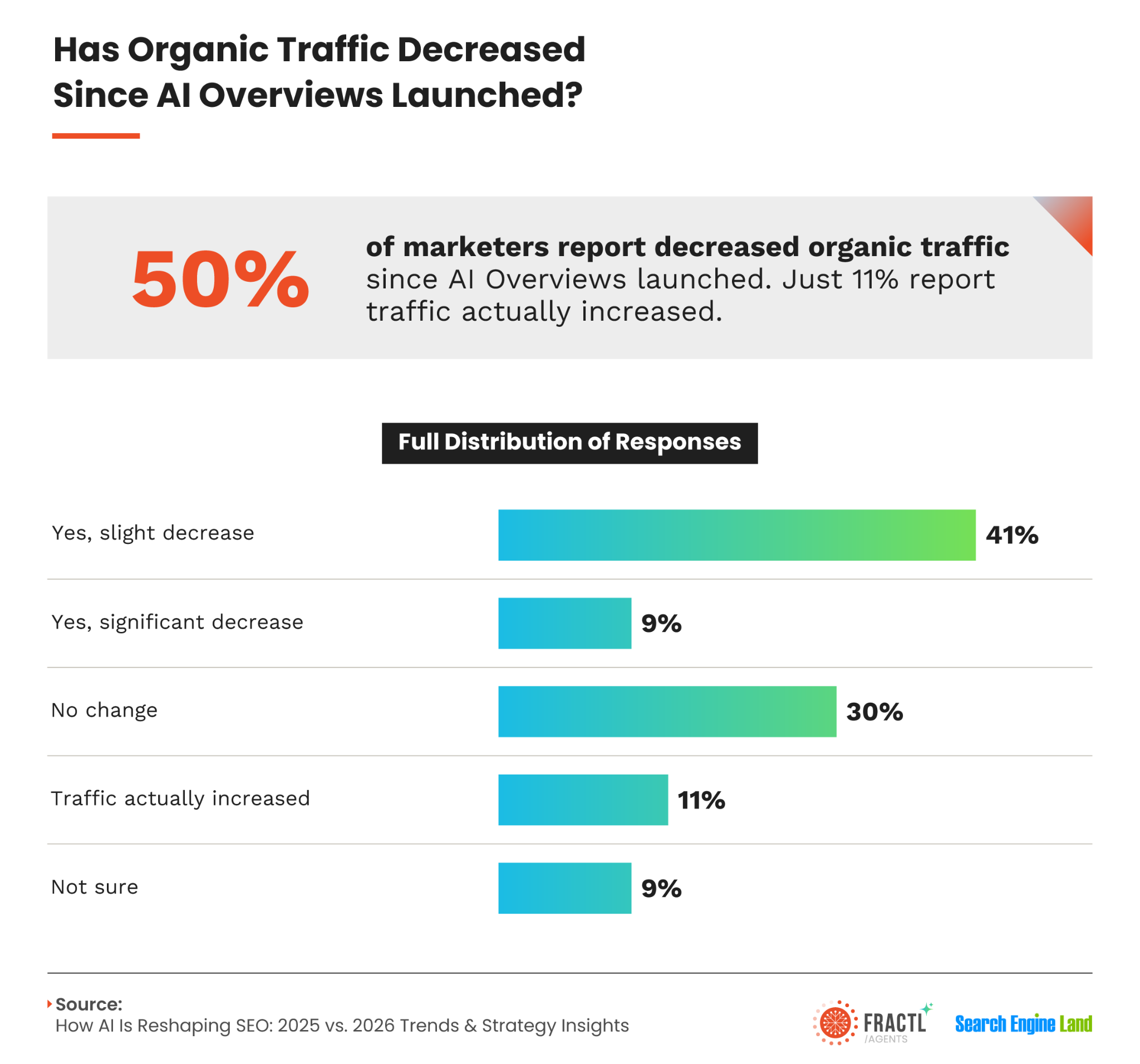

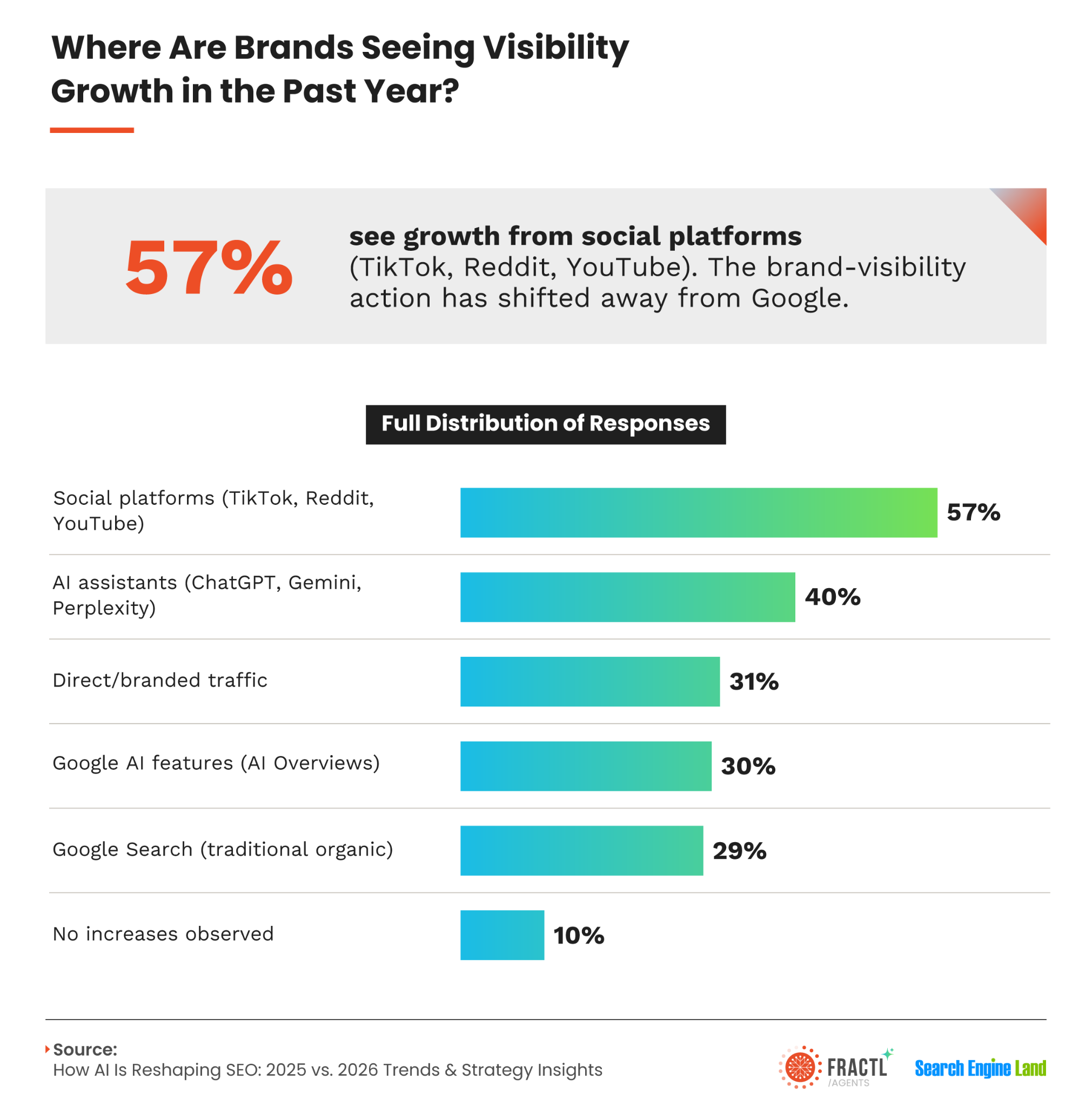

Organic traffic is under pressure, not in freefall

Half of the marketers surveyed reported organic traffic declines since the launch of AI Overviews, and 61% blame AI. That is meaningful, but it is not the whole story.

The larger shift is not simply from Google to ChatGPT. It is from search as a destination to search as a behavior. People are asking, comparing, validating, and deciding across platforms, communities, assistants, and review environments.

The same marketers reporting organic losses are often finding visibility elsewhere. Fifty-seven percent report growth from social platforms such as TikTok, Reddit, and YouTube. Forty percent see growth from AI assistants such as ChatGPT, Gemini, and Perplexity. Thirty-one percent see growth in direct or branded traffic, while only 10% report no visibility growth anywhere.

That is why I think 2026 brand visibility depends on brand mentions and entity authority across the web, not just individual page rankings in Google.

Marketers are prioritizing the easiest tactics

Many teams are moving in the right general direction: community building, earned authority, owned audiences, expert content, and traffic diversification. The most prioritized strategies include building brand presence on social platforms at 59%, GEO and AEO optimization at 54%, and creating authoritative expert content at 44%.

But the least prioritized strategy is original research and data, at only 15%. I see that as a strategic inversion.

Original, proprietary research is one of the hardest content assets for AI to replicate or commoditize. It earns citations, attracts links, builds topical authority, and gives journalists, communities, search engines, and AI systems something distinctive to reference.

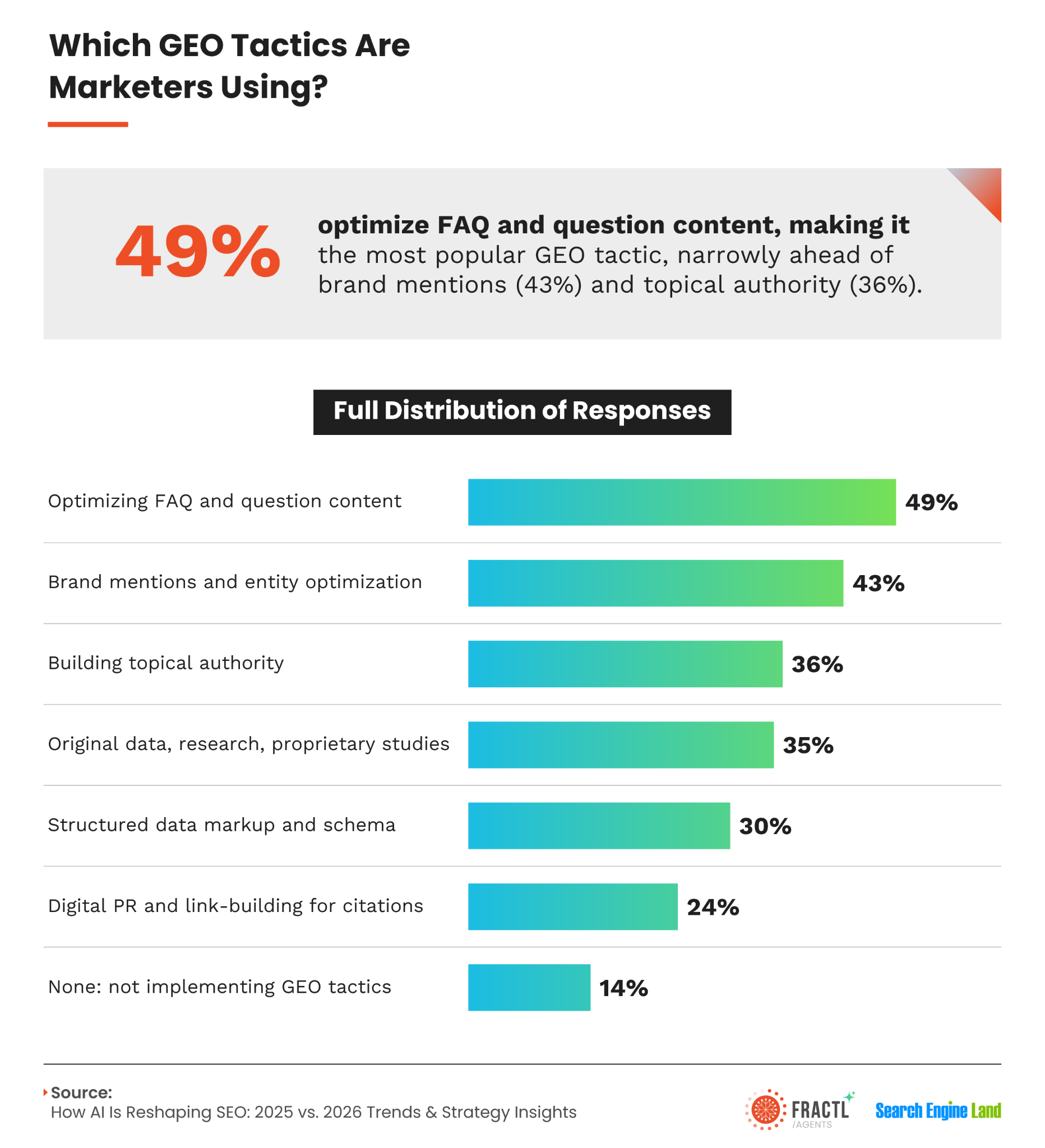

In GEO, the same pattern appears. Many marketers are using content-led tactics that AI can easily replicate. Long-tail FAQs can help with AI Overviews, and schema can support structure, but neither one builds credibility by itself.

The stronger moat is entity authority: proprietary data, expert perspectives, topical depth, and third-party validation. These are the assets that make a brand worth citing.

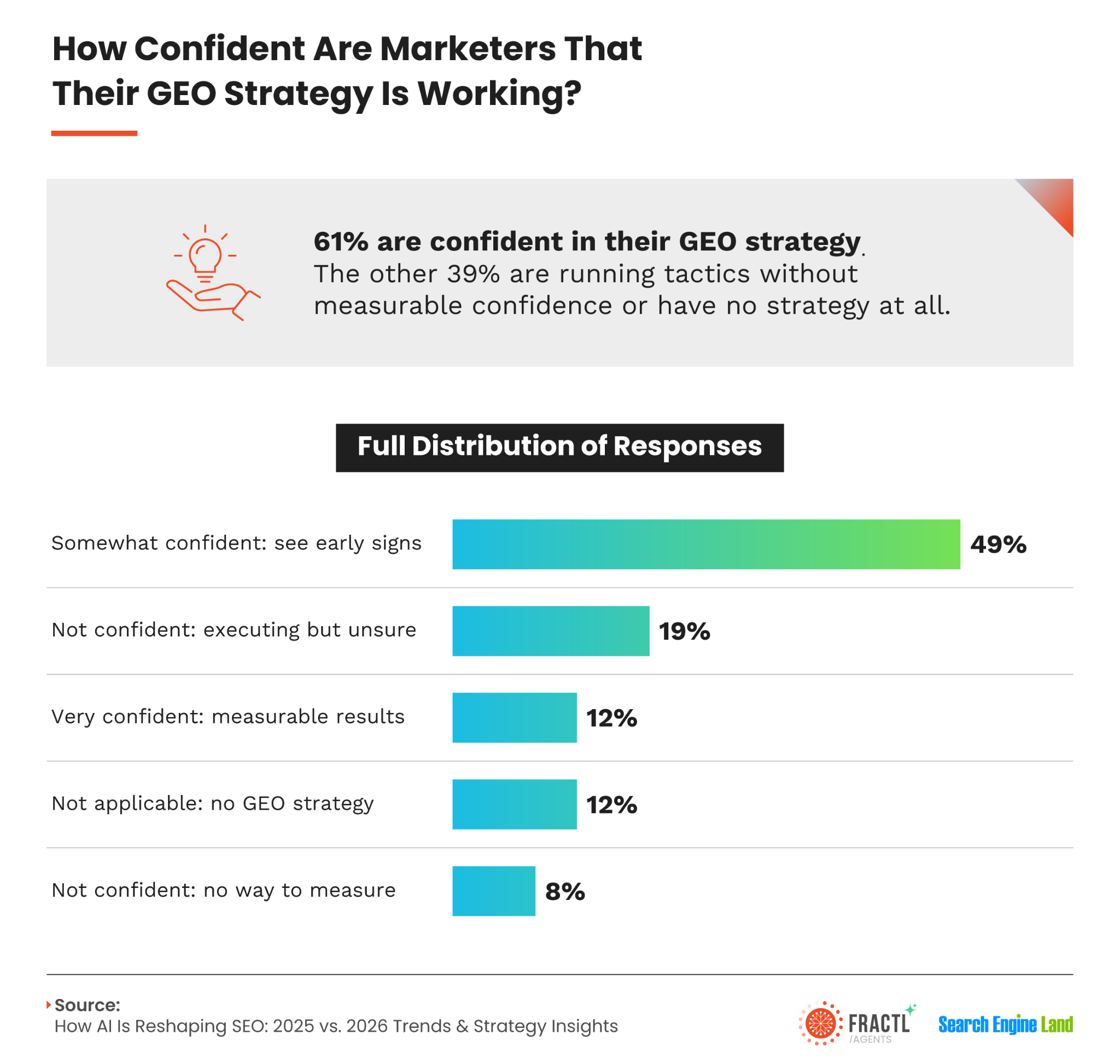

GEO measurement is lagging behind execution

Only a little more than half of marketers are confident in their GEO strategy, and only 12% have measurable results. That is understandable for a newer channel, but GEO is becoming too important to manage casually.

I believe visibility tracking, citation monitoring, branded search lift, and AI-assisted conversion analysis all need more attention. Teams that can prove GEO ROI will be able to defend and grow investment while others are still guessing.

The main barrier to deeper AI integration is not leadership buy-in. Only 2% cite that as the obstacle. The top barrier is team training and skill gaps at 26%, followed by tool fragmentation at 20%, budget constraints at 19%, unclear ROI at 12%, and legal or compliance concerns at 12%.

For search teams, that means AI literacy, prompt strategy, content quality control, and GEO measurement skills may be more valuable right now than adding another tool to the stack.

What I would do for a 2026 search strategy

First, I would audit the brand’s AI footprint. I would query the brand name across ChatGPT, Gemini, Perplexity, and Google AI Overviews, then document what is accurate, what is missing, and what is wrong. Waiting until an AI error becomes a PR issue is too late.

Second, I would invest in entity authority and original research. AI cannot invent legitimate proprietary survey data, named expert perspectives, verified brand facts, or original market analysis. Those assets become more valuable as AI systems get better at rewarding genuine authority.

Third, I would distribute visibility across multiple platforms. Google organic remains necessary, but it is no longer sufficient. A brand needs a consistent presence in Reddit discussions, YouTube content, AI assistant responses, review platforms, and earned media.

Fourth, I would build AI content governance, not just AI content workflows. Consumer demand for AI disclosure ranges from 84% to 91% across formats, while only 20% of brands always disclose. That gap is a reputational liability and may become a legal and regulatory one.

Fifth, I would close the GEO measurement gap. If I can connect AI search mentions to traffic, lead quality, and revenue, I can prove ROI at a time when most teams cannot. That creates a budget and strategy advantage that compounds.

Finally, I would double down on what AI cannot easily replicate: proprietary data, named experts, human-verified claims, transparent sourcing, and a consistent high-quality brand voice. In 2026, the brands that treat quality as a strategic differentiator are the ones most likely to be surfaced, cited, and trusted.

Methodology

Fractl and Search Engine Land surveyed 1,008 U.S. consumers and 150 marketers in Q2 2026. The consumer sample was nationally representative across age, gender, and region. The marketer sample included companies ranging from fewer than 10 employees to more than 5,000 and covered roles in SEO, content, social, analytics, paid media, PR, and marketing leadership.

Where noted, findings are compared year over year against the same questions asked in Fractl’s 2025 consumer study conducted with Search Engine Land.

Inspired by this post on Search Engine Land.