AI now shows up in nearly every corner of marketing, and for every useful initiative I see, it feels like 10 vendors appear with a tool that claims to solve it.

When this wave first started, I took more vendor calls and answered more outreach than I do now. Over time, I noticed I was asking the same core questions again and again to decide whether an AI tool was actually worth deploying.

If I feel overwhelmed by AI vendor pitches, these are the five questions I use to separate useful solutions from noise. They help me understand what the tool does, whether it solves a real business problem, and whether the vendor is the kind of partner I would trust with my budget, data, and team’s time.

1. What problem does your tool solve?

I start here because I want to understand the purpose of the tool and, more importantly, whether the value it creates connects to real business outcomes.

If a vendor cannot clearly explain the challenges or use cases the tool addresses, I assume it was not purpose-built for a real problem my team faces. That applies whether I am evaluating it from an in-house perspective or on behalf of an agency. I am cautious when vendors lead with feature-heavy language but cannot explain the business benefits those features are supposed to deliver.

If a vendor can identify at least one existing team problem and explain how the tool improves business outcomes, I keep the conversation going. My next question is usually for a case study that shows how the tool was used and what results it delivered for an organization similar to mine in size, market, or vertical.

I look for benefits such as increasing output or identifying tracking gaps that speed up troubleshooting. I do not rush to buy a tool simply because it promises to save time, even if that promise is true. I need to know how I will use that extra time before I can decide whether the savings are meaningful.

2. What expertise do you have in the space where this tool solves a problem?

This answer tells me whether the vendor built the tool for advertisers or merely at advertisers.

Technical skill matters, but so does understanding how a media buyer actually spends the day. If the vendor does not have direct experience in media buying, I want to hear how the team researched the market and how those insights shaped the product.

A shallow understanding of the problem is a red flag for me. I do not expect every sales rep to have deep domain expertise, but someone on the team should. If I am seriously considering the tool, I want access to that person early in the process.

When a vendor has a credible story about identifying a problem I recognize firsthand and building a solution around it, I find that compelling. A founding mission tied to my actual challenges gives me more confidence that the tool can make a real difference in performance.

3. What case studies, real use cases, and results can you share?

In a fast-moving AI market, I treat case studies as essential. I want to know whether the vendor has a strong track record with customers like me or whether I would be one of the first teams testing the product in my space.

If I would be an early adopter, I weigh the tradeoffs carefully. I might gain an advantage by finding a growth accelerator before competitors do. I might also spend time working through bugs, giving detailed feedback, or discovering that the tool does not deliver what was promised.

If I cannot trust the tool, or if I will need to provide a lot of feedback just to make it useful, I have to decide whether the potential payoff is big enough to justify the time and money. In most cases, that bar should be high.

Rows of illuminated data cabinets and paper files stretch into the distance, capturing the pressure on marketers to turn fragmented customer data into a smarter performance engine.

If I am clearly going to be an early adopter and the vendor will not offer flexible contract terms that reduce my risk, I consider that a nonstarter. Established tools may be less flexible on pricing because they can already prove consistent value. Newer tools that take a hard line on price and contract terms are much less likely to become strong long-term partners.

For established vendors, I want specific and relevant case studies with real numbers from advertisers in a similar space, at a similar size, or with a similar use case.

For early-stage companies, the best answer is honesty. If a vendor says, “You’d be one of our first clients in this vertical. Here’s what we’ve seen elsewhere, and here’s what that partnership would look like,” I see that transparency as a positive sign.

4. Who owns my data, and how is it being used to train models?

I am still surprised by how quickly people share data with AI tools in the rush to find a competitive edge. Before I sign anything, I take data ownership and model training terms seriously.

I watch for any answer suggesting that my data could be used to train shared or third-party models without my explicit consent. I also treat vague answers, deflections, or terms of service that conflict with the salesperson’s verbal explanation as major warning signs.

I own my data, full stop.

The vendor should be able to clearly explain where my data is stored, how long it is retained, whether it is used for model training, and what happens to it if I stop using the tool. If model training is involved, I want that training limited to refining my own instance. Most importantly, I want those commitments in the contract, not just in a conversation. If the language is missing, I insist that it be added before I sign.

5. What does implementation actually look like, and what does success require from our team?

Before I commit budget, I need to understand the real cost of adopting the tool. That cost is not just the subscription price. It includes the time, internal lift, integration work, training, QA, and possible disruption to the existing martech stack.

If the tool requires resources my team does not have, or if I cannot realistically dedicate the time needed to use it well, I do not consider it a smart investment yet. A lot of wasted martech spend could be avoided by asking this question and taking the answer seriously.

I do not expect every tool to fit every organization, but I do expect implementation to be clear and the product to be intuitive enough for the team to adopt. If people cannot understand it, trust it, or fit it into their workflow, it will not create the value the vendor promised.

I do not let AI hype rush my decision

I know firsthand that many AI tools sound too good to be true, and often they are. I still want to stay curious and ambitious, but I balance that with caution.

I also remind myself that AI adoption is still early. If a tool feels too expensive, too difficult to onboard, or too rigid in its contract terms compared with its track record, I am willing to wait. A better option may appear in the next few months.

When I am unsure, I ask for a free trial. If integrating the tool will not create too much work for the team, a trial can be the best way to decide whether I have found a real competitive advantage or just another AI pitch dressed up as one.

A year ago, I saw 82% of consumers say AI-powered search was more helpful than traditional search. By 2026, that number had fallen to 54%, a 28-point drop in sentiment in just 12 months.

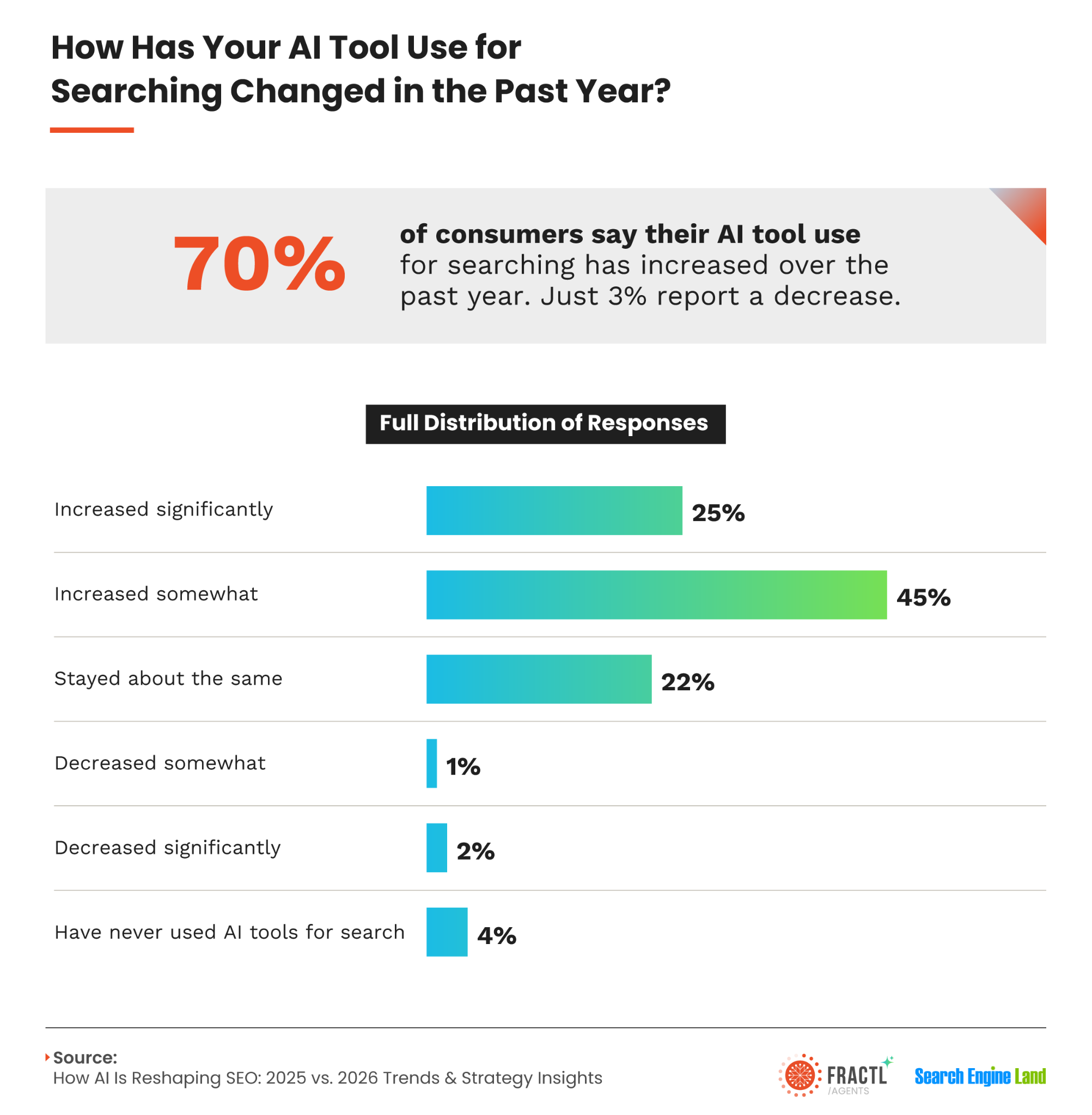

That does not mean people are abandoning AI search. In fact, 70% of consumers say they are using AI tools for search more than they did last year. The tension is clear: adoption is rising, but trust is slipping.

That is the core issue I believe search marketers need to solve in 2026. It is no longer enough to appear in AI answers. I need my brand, and the brands I work with, to be visible, accurate, credible, and trusted when AI systems surface information.

To understand the shift, Fractl partnered with Search Engine Land to expand our 2025 research. We surveyed 1,008 U.S. consumers and 150 marketers to compare how consumer trust, marketer adoption, and brand strategy are changing in the AI search era. Disclosure: I am the co-founder of Fractl.

Here is what I believe the data means for 2026 search strategy.

Consumers are using AI more, but trusting it less

AI search adoption is no longer the main story. Seventy percent of consumers report increased use of AI tools for search over the past year, while only 3% say their use has decreased. The bigger question is whether people trust what those tools return.

One surprising finding is that baby boomers now find AI more helpful than Gen Z, 63% to 47%. That challenges the assumption that younger users automatically embrace AI while older users lag behind. What I see instead is a more complicated market where trust has to be earned across every generation.

In 2025, only 3% of consumers said AI was less helpful than traditional search. By 2026, that skeptic group had grown to 17%, nearly six times larger than the year before. Even among the 54% who still find AI helpful, enthusiasm is softer: 37% say it is only somewhat more helpful, while 17% say it is much more helpful.

I think hallucinations and low-quality AI content are changing how people evaluate the entire channel. Consumers may use AI because it is convenient, but convenience does not automatically create confidence.

AI content volume has become a brand trust risk

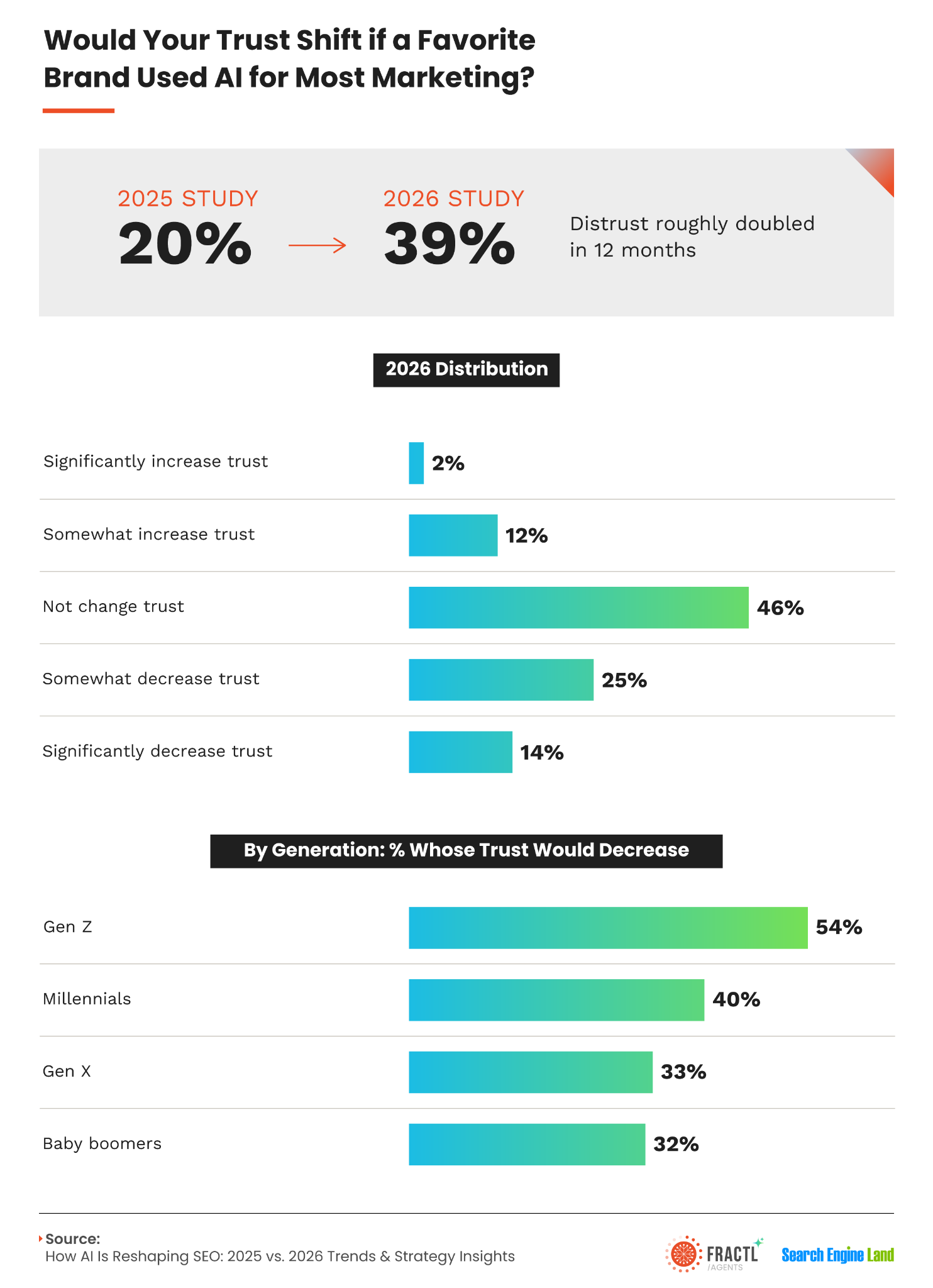

In 2025, 20% of consumers said heavy AI use would reduce their trust in a brand. In 2026, that number rose to 39%. For me, that makes AI content scale a reputational issue, not just an operational decision.

If I publish AI-assisted content at scale without disclosure, strong editorial standards, or obvious quality signals, I am asking my audience to trust a process they are increasingly skeptical of. That is a risk more brands need to take seriously.

Gen Z is especially strict. Fifty-four percent of Gen Z consumers say heavy AI use in a brand’s marketing would decrease their trust, compared with 32% of baby boomers and 33% of Gen X. Women are also more likely than men to penalize brands for heavy AI use, 44% vs. 34%.

That matters because Gen Z is often the audience most likely to engage deeply, share content, shape online conversations, and influence long-term organic visibility. If that audience matters to a brand, AI-generated filler is not a harmless shortcut.

Disclosure is now a consumer expectation

Across every major content format, more than 80% of consumers want AI-generated content labeled. Video leads at 91%, followed by images at 90%, audio at 87%, and written content at 84%. More than half of respondents strongly agree with labeling in every category.

I do not read that as a mild preference. I read it as a near-universal expectation. The brands that treat AI disclosure as optional are creating a gap between how they operate and what their audiences want.

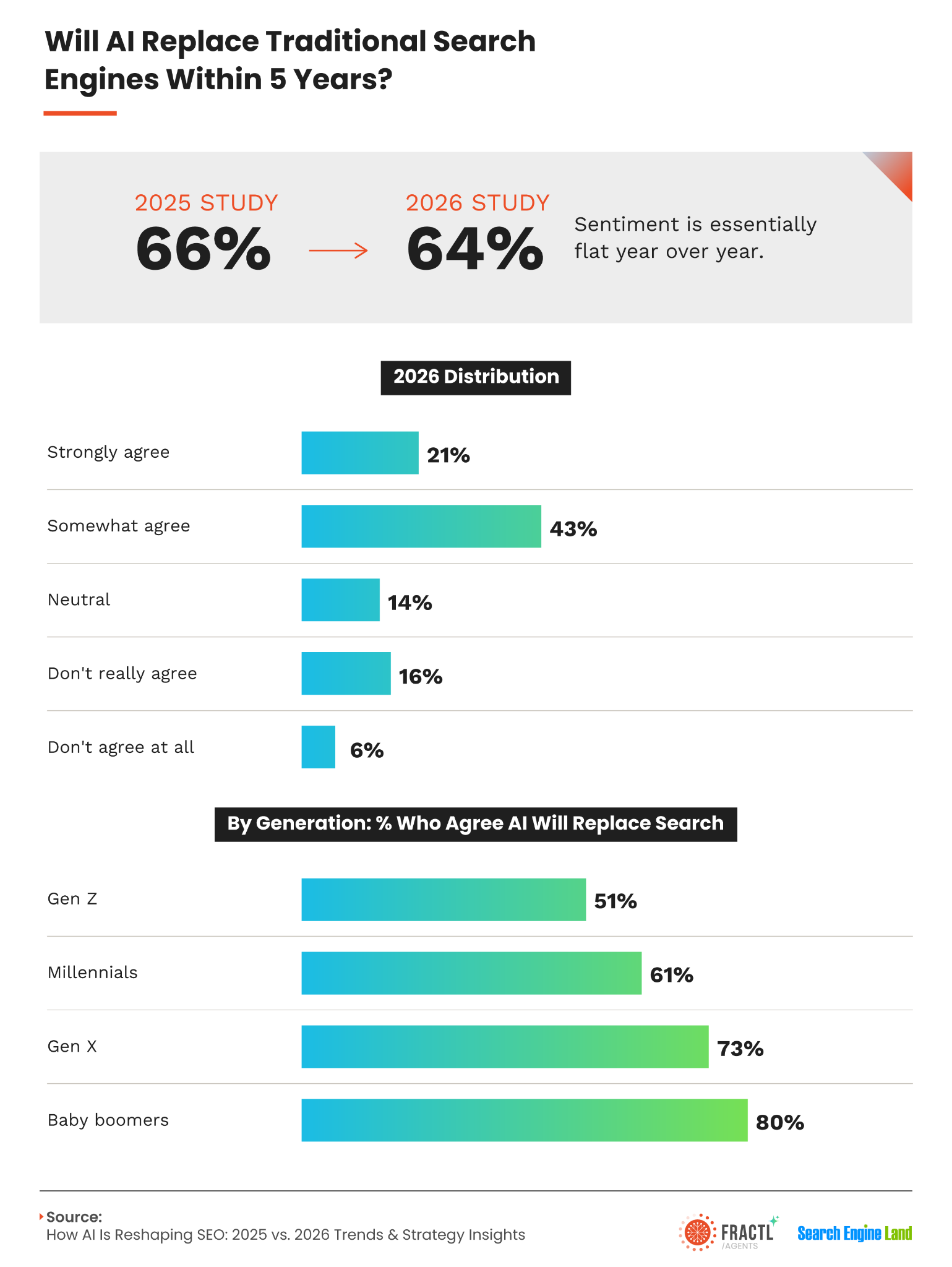

Consumers still believe AI will shape the future of search. Sixty-four percent agree that AI will replace traditional search engines within five years, nearly unchanged from 66% in 2025. The channel is not going away. But being present in AI results and being trusted in AI results are now two different challenges.

Google still leads on trust, especially for buying decisions

When consumers are making purchase decisions, 39% turn to Google first. Reddit follows at 15%, AI tools at 14%, and review sites and friends or family each at 11%. The trust people have built with Google has not automatically transferred to AI tools.

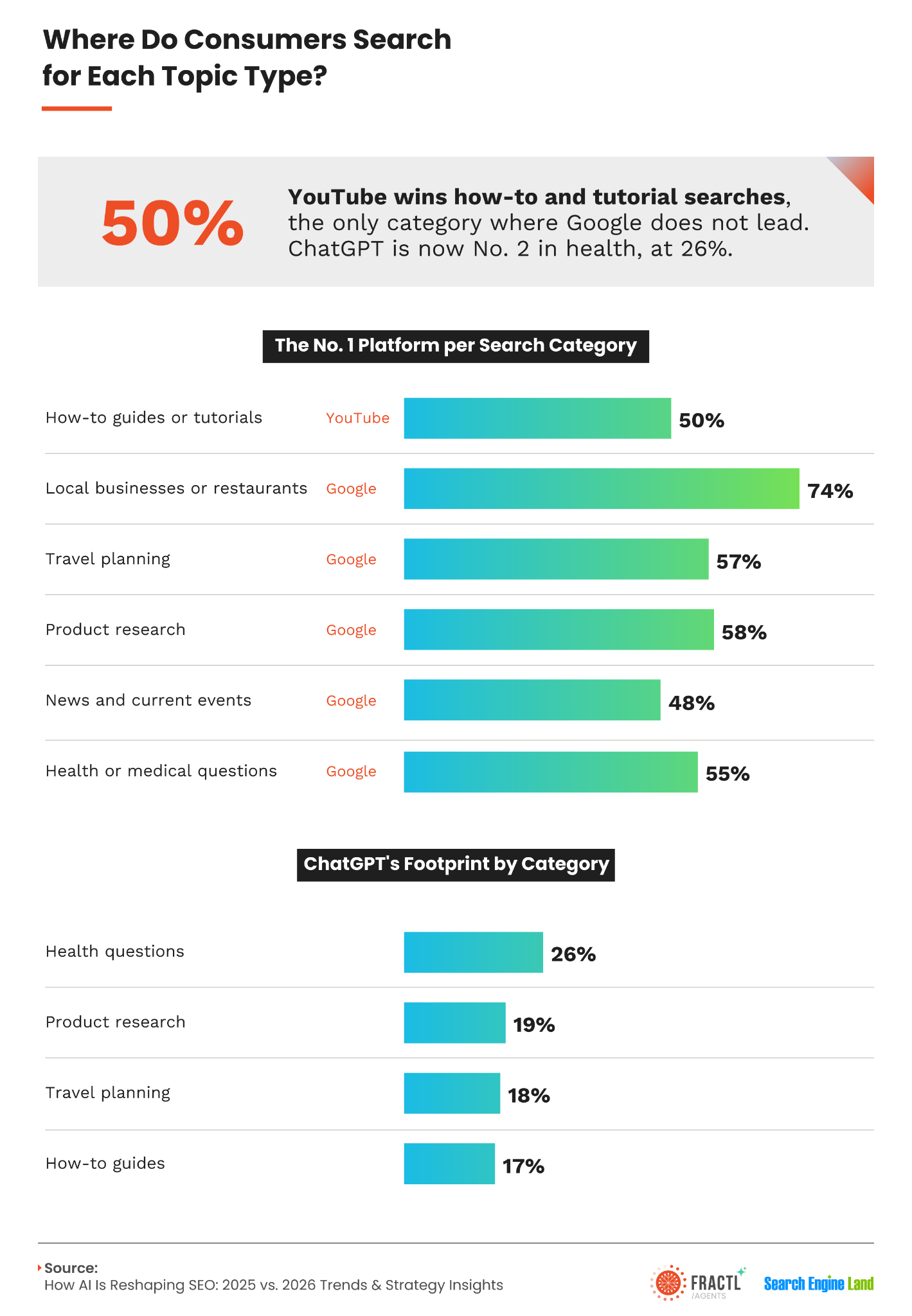

Platform preference also changes by query type. Google dominates five of six major search categories. It is the first stop for local businesses, product research, travel planning, and health questions. YouTube overtakes Google for how-to content, while ChatGPT is now the second-most-used destination for health questions and ranks strongly for product research, travel planning, and how-to content.

That tells me there is no single AI search platform to optimize for. I need to map content strategy to actual user behavior: where people search, what they are trying to decide, and which platforms influence confidence at each stage.

Before making a purchase decision, the average consumer checks 2.4 platforms. Gen Z checks 2.5, millennials 2.4, Gen X 2.3, and baby boomers 2.2. This behavior is consistent enough that I now think of search optimization as a multi-platform visibility strategy, not a rankings-only discipline.

A brand that appears in Google results but nowhere else can lose to a brand that appears in Google, shows up in Reddit discussions, gets cited by ChatGPT, and has strong third-party review content. Visibility now has to travel with the buyer.

AI is changing marketing operations quickly

AI now touches 53% of marketing work on average, up from 38% in 2025. In practical terms, the equivalent of one full workday per week has shifted to AI-assisted workflows in just 12 months. Fifty-nine percent of marketers say AI is involved in at least half their work, while 27% say it is involved in three-quarters or more.

For SEO and content teams, this means competitors are moving faster. But speed alone is becoming commoditized. Accuracy, original insight, expert judgment, and brand credibility are much harder to copy.

Marketers are also feeling pressure to adopt AI. Fifty-five percent of marketing roles report a 7-out-of-10 level of pressure to use it. SEO and analytics teams feel that pressure most, while PR is not far behind. As AI makes generic content easier to produce, the advantage shifts toward what AI cannot automate well: judgment, relationships, trust, and reputation.

The quality tradeoff is real. Only 26% of marketers say AI made their work both faster and better. Nearly half say it made their work faster but more generic, and 7% report an outright quality decline.

That is where I see a major competitive opening. If other teams are scaling generic AI content while I invest in original data, expert quotes, third-party validation, and earned brand mentions, I am building assets that are more visible, credible, and retrievable across search engines, social platforms, and LLMs.

AI governance is still too weak

About three in four organizations conduct human editorial review before publishing AI-generated content. Sixty-two percent check for brand voice, 54% check facts, and 42% conduct legal or compliance review. Only 27% evaluate content for bias.

That means nearly half of AI-generated content may enter the market without fact-checking, legal review, or plagiarism checks. Too many teams are still relying on surface-level review: Does it sound right? Is the tone appropriate? Are there typos?

In a year when consumers are already prepared to distrust generic AI content, I see governance as one of the cheapest gaps to close and one of the most expensive to ignore.

The disclosure gap is just as serious. Heavy, generic AI use is now a brand-trust liability, yet only 20% of organizations always disclose AI use to their audiences. Compare that with the 84% average consumer demand for labeling written content, and the disconnect is obvious.

The takeaway is not to abandon AI. It is to stop treating governance as optional. Every AI workflow needs accuracy checks, transparency standards, bias review, and human accountability before content reaches an audience.

AI hallucinations are already a brand problem

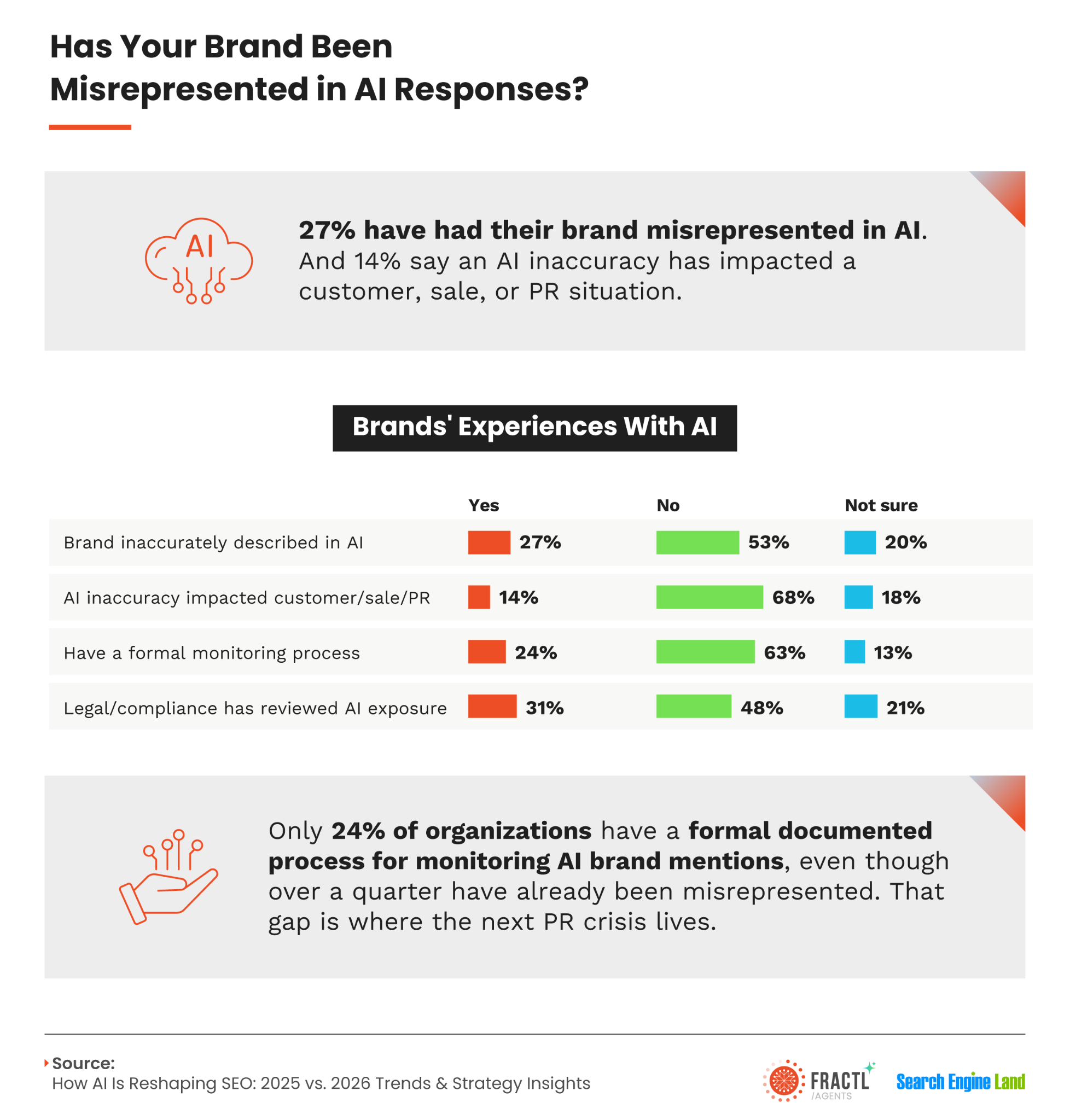

A year ago, about 22% of marketers tracked LLM visibility. In 2026, that figure barely moved to 24%. At the same time, 27% of brands have already been misrepresented in AI-generated responses, and 14% say an AI inaccuracy has affected a customer relationship, sale, or PR situation.

More brands have been misrepresented by AI than have a formal monitoring process. That should concern every search and communications team.

If AI is summarizing my category, comparing my product, or explaining my brand incorrectly, that is not only an SEO issue. It is a reputation risk, a revenue risk, and a PR issue waiting to escalate.

When AI misrepresents a brand, I believe fixing the source matters more than arguing with the output. That can mean reaching out to publishers for updates, correcting owned profiles, improving brand pages, and publishing clear correction content tied to the entity.

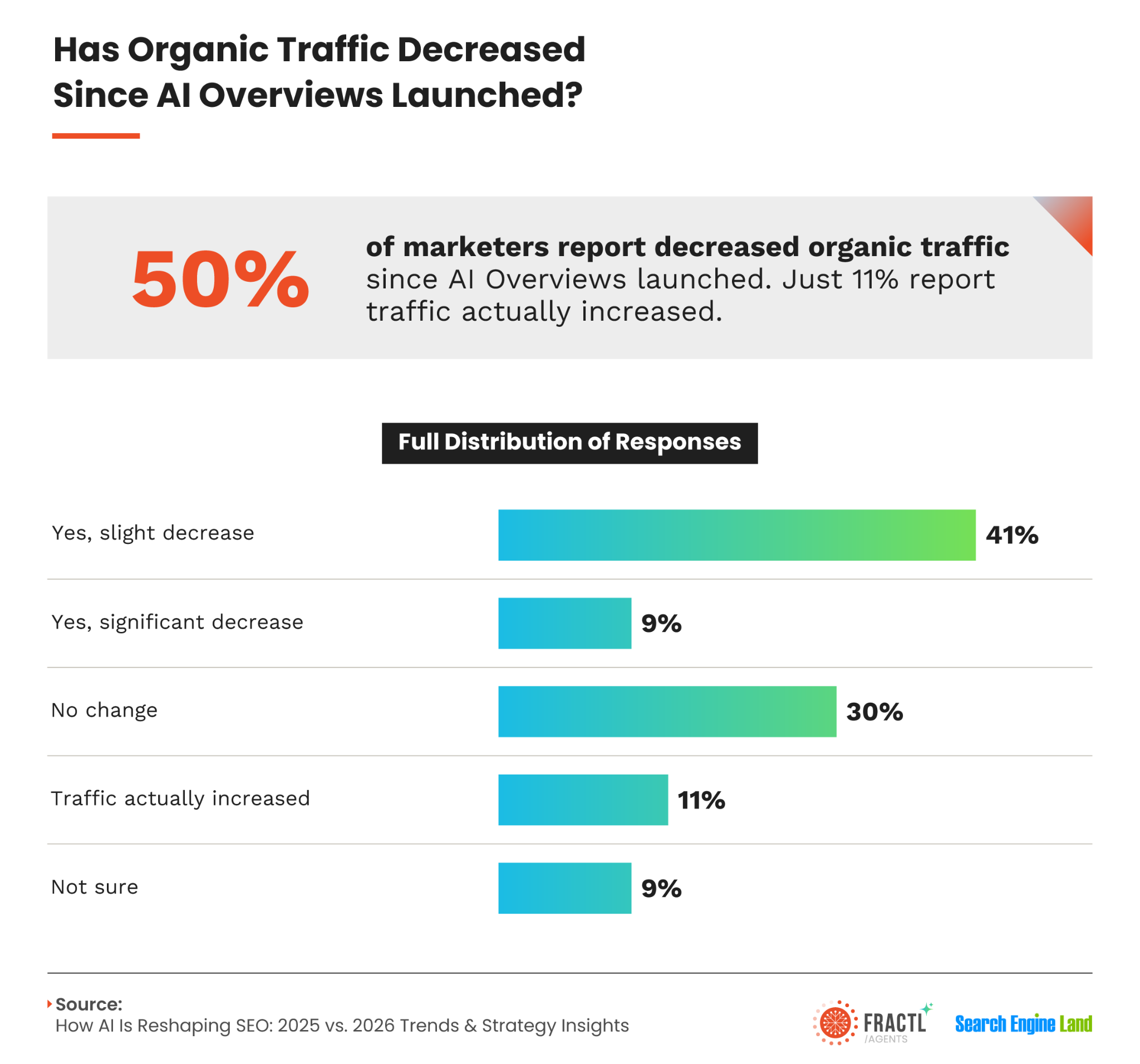

Organic traffic is under pressure, not in freefall

Half of the marketers surveyed reported organic traffic declines since the launch of AI Overviews, and 61% blame AI. That is meaningful, but it is not the whole story.

The larger shift is not simply from Google to ChatGPT. It is from search as a destination to search as a behavior. People are asking, comparing, validating, and deciding across platforms, communities, assistants, and review environments.

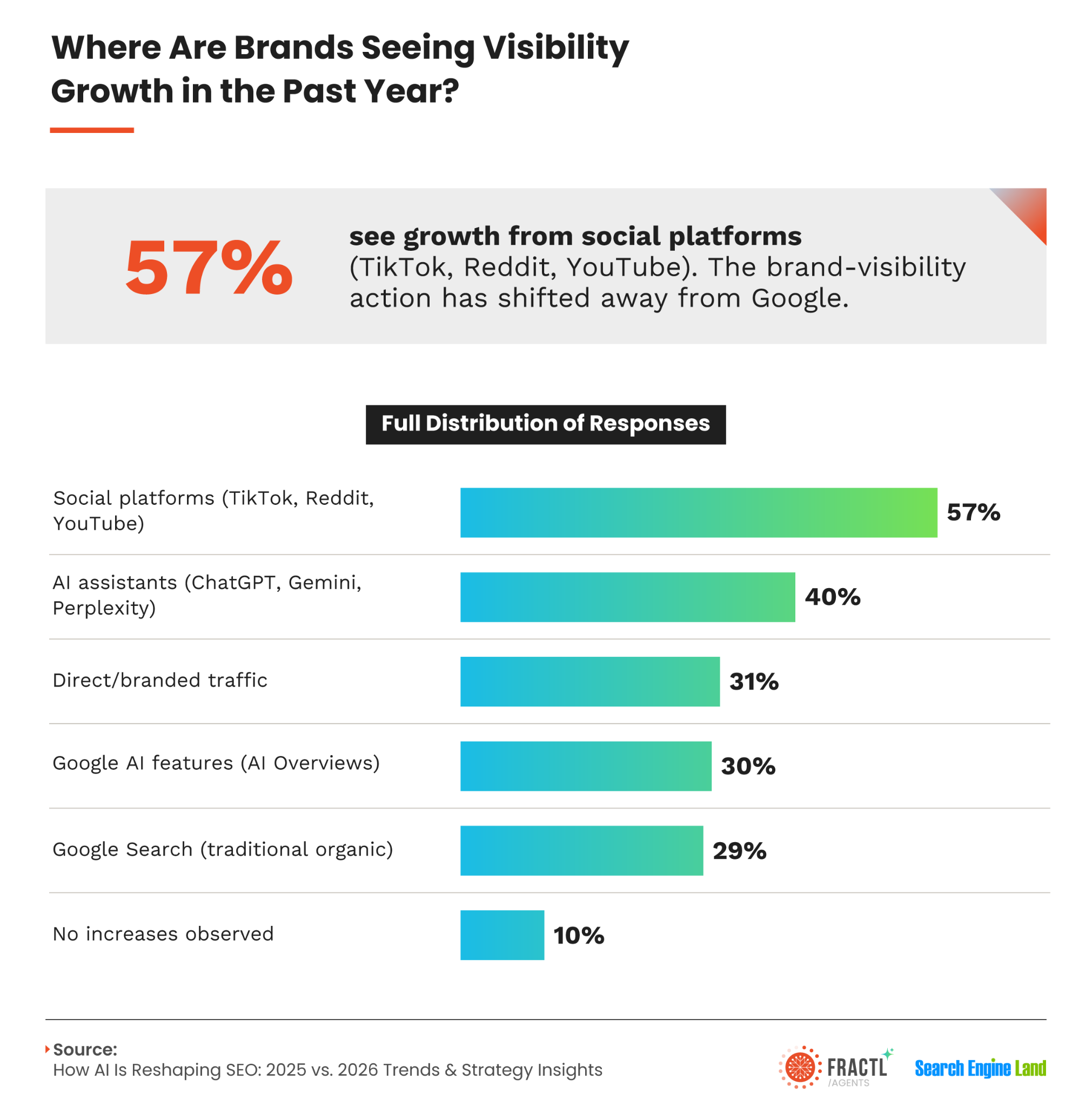

The same marketers reporting organic losses are often finding visibility elsewhere. Fifty-seven percent report growth from social platforms such as TikTok, Reddit, and YouTube. Forty percent see growth from AI assistants such as ChatGPT, Gemini, and Perplexity. Thirty-one percent see growth in direct or branded traffic, while only 10% report no visibility growth anywhere.

That is why I think 2026 brand visibility depends on brand mentions and entity authority across the web, not just individual page rankings in Google.

Marketers are prioritizing the easiest tactics

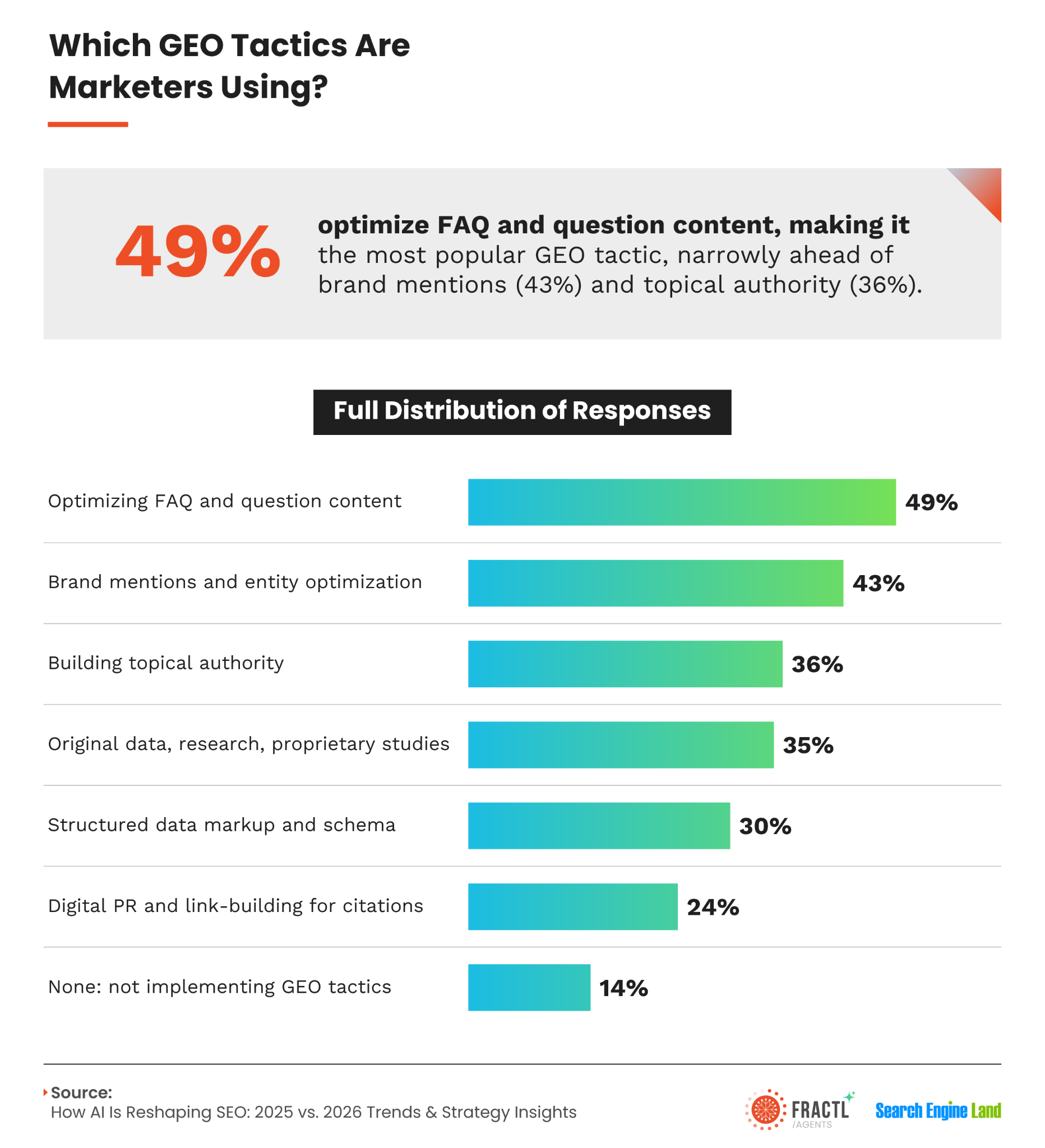

Many teams are moving in the right general direction: community building, earned authority, owned audiences, expert content, and traffic diversification. The most prioritized strategies include building brand presence on social platforms at 59%, GEO and AEO optimization at 54%, and creating authoritative expert content at 44%.

Half of surveyed marketers say organic traffic has fallen since AI Overviews arrived, but the data points to pressure rather than collapse, with 30% reporting no change.

But the least prioritized strategy is original research and data, at only 15%. I see that as a strategic inversion.

Original, proprietary research is one of the hardest content assets for AI to replicate or commoditize. It earns citations, attracts links, builds topical authority, and gives journalists, communities, search engines, and AI systems something distinctive to reference.

In GEO, the same pattern appears. Many marketers are using content-led tactics that AI can easily replicate. Long-tail FAQs can help with AI Overviews, and schema can support structure, but neither one builds credibility by itself.

As organic search pressure grows, marketers are finding brand visibility gains across social platforms, AI assistants, direct traffic and Google AI features, according to Fractl and Search Engine Land.

The stronger moat is entity authority: proprietary data, expert perspectives, topical depth, and third-party validation. These are the assets that make a brand worth citing.

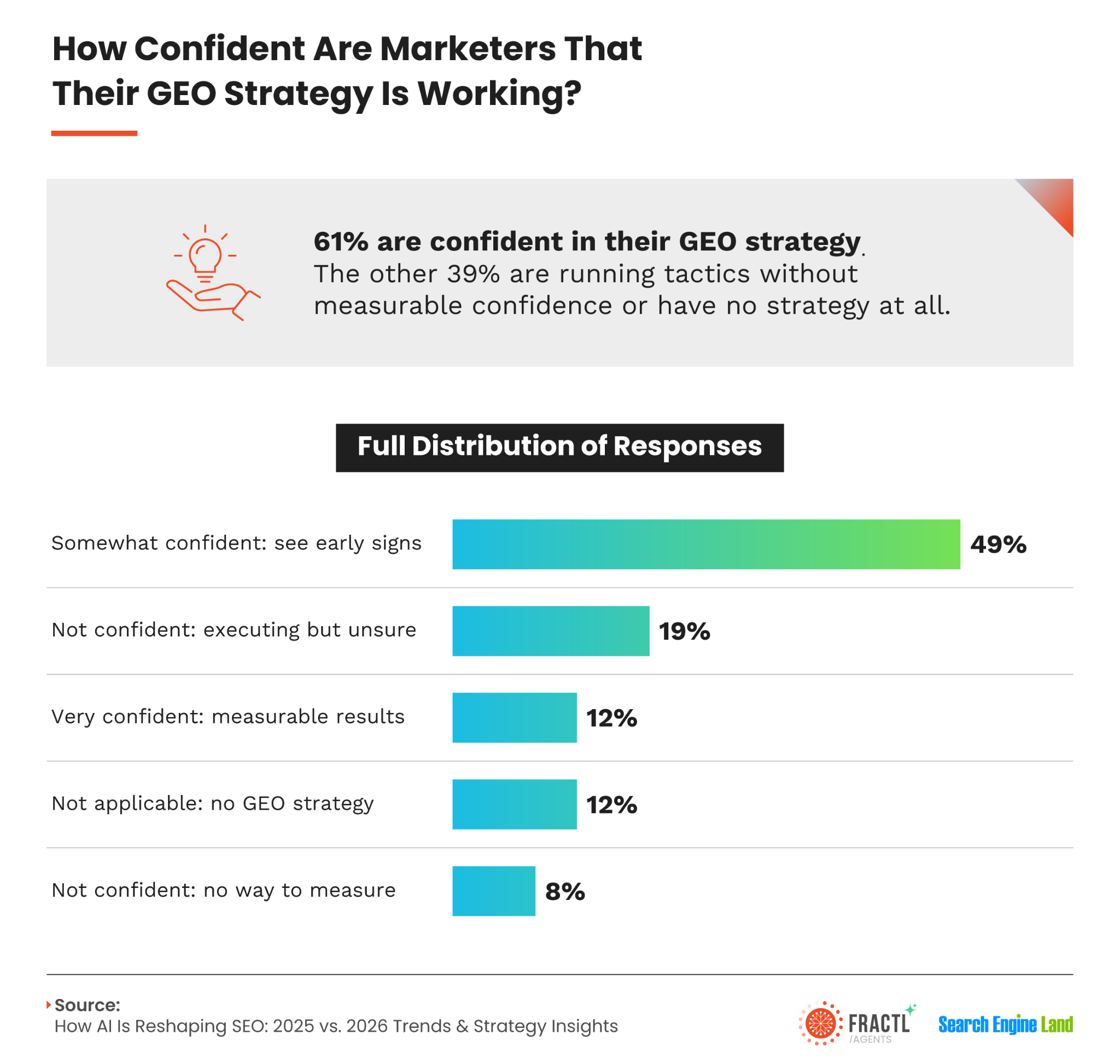

GEO measurement is lagging behind execution

Only a little more than half of marketers are confident in their GEO strategy, and only 12% have measurable results. That is understandable for a newer channel, but GEO is becoming too important to manage casually.

Marketers are leaning into practical GEO tactics, with FAQ optimization leading the pack, while entity authority, original research and citations trail behind.

I believe visibility tracking, citation monitoring, branded search lift, and AI-assisted conversion analysis all need more attention. Teams that can prove GEO ROI will be able to defend and grow investment while others are still guessing.

The main barrier to deeper AI integration is not leadership buy-in. Only 2% cite that as the obstacle. The top barrier is team training and skill gaps at 26%, followed by tool fragmentation at 20%, budget constraints at 19%, unclear ROI at 12%, and legal or compliance concerns at 12%.

For search teams, that means AI literacy, prompt strategy, content quality control, and GEO measurement skills may be more valuable right now than adding another tool to the stack.

Most marketers see early signs their GEO strategy is working, but only 12% report measurable results, highlighting a major gap in AI search measurement.

What I would do for a 2026 search strategy

First, I would audit the brand’s AI footprint. I would query the brand name across ChatGPT, Gemini, Perplexity, and Google AI Overviews, then document what is accurate, what is missing, and what is wrong. Waiting until an AI error becomes a PR issue is too late.

Second, I would invest in entity authority and original research. AI cannot invent legitimate proprietary survey data, named expert perspectives, verified brand facts, or original market analysis. Those assets become more valuable as AI systems get better at rewarding genuine authority.

Third, I would distribute visibility across multiple platforms. Google organic remains necessary, but it is no longer sufficient. A brand needs a consistent presence in Reddit discussions, YouTube content, AI assistant responses, review platforms, and earned media.

Fourth, I would build AI content governance, not just AI content workflows. Consumer demand for AI disclosure ranges from 84% to 91% across formats, while only 20% of brands always disclose. That gap is a reputational liability and may become a legal and regulatory one.

Fifth, I would close the GEO measurement gap. If I can connect AI search mentions to traffic, lead quality, and revenue, I can prove ROI at a time when most teams cannot. That creates a budget and strategy advantage that compounds.

Finally, I would double down on what AI cannot easily replicate: proprietary data, named experts, human-verified claims, transparent sourcing, and a consistent high-quality brand voice. In 2026, the brands that treat quality as a strategic differentiator are the ones most likely to be surfaced, cited, and trusted.

Methodology

Fractl and Search Engine Land surveyed 1,008 U.S. consumers and 150 marketers in Q2 2026. The consumer sample was nationally representative across age, gender, and region. The marketer sample included companies ranging from fewer than 10 employees to more than 5,000 and covered roles in SEO, content, social, analytics, paid media, PR, and marketing leadership.

Where noted, findings are compared year over year against the same questions asked in Fractl’s 2025 consumer study conducted with Search Engine Land.

I think one of the biggest mistakes in AI marketing is positioning a product as a replacement for people. That message can win attention in the short term, but I believe it quietly drains trust over time.

This is a little different from what I usually write about, but it matters. The way we talk about AI shapes how customers, employees, executives, and markets respond to it.

In this memo, I want to focus on three things: why “substitution positioning” feels powerful at first but weakens a brand later, what the data says about whether AI is actually replacing people, and how I think companies should position AI instead.

The cardinal sin of positioning in the AI era is replacement. I call it substitution positioning. It is tempting because it sounds bold, efficient, and disruptive. But over time, it creates anxiety, skepticism, and credibility problems.

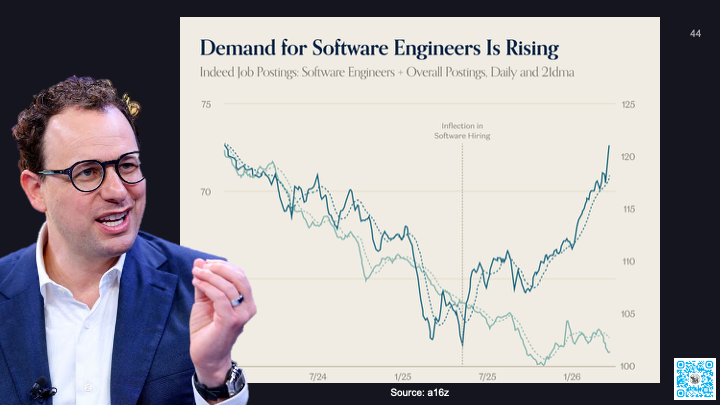

We have seen this pattern already. Anthropic CEO Dario Amodei predicted that software engineering jobs could disappear within 6 to 12 months as models began doing most or all of what software engineers do end to end. Yet demand for software engineers has continued to look strong.

OpenAI CEO Sam Altman also predicted that many customer support jobs would go away because AI could handle that work better. Soon after, customer service hiring began outpacing the broader job market.

I understand why fear works as a marketing tool. The fear of being replaced gets attention fast. It got me, too. When powerful AI models gained traction, I worried about my own future. But when I still see AI companies hiring copywriters, SEOs, engineers, and support teams, I sleep better.

Fear sells because it taps into fight-or-flight. Layoffs make that story even louder. They let companies frame cost-cutting as innovation and make the replacement narrative feel more real than it may actually be.

But I do not think the facts support the clean replacement story. In New York, companies can indicate when mass layoffs are caused by technological innovation or automation. In one reported period, more than 160 companies filed mass layoffs affecting roughly 28,300 workers, and not one chose AI as the reason. That list included companies such as Amazon and Goldman Sachs.

Researchers at Yale also studied employment data from the Current Population Survey over 33 months and found no evidence of job displacement from AI. To me, the pattern looks less like instant replacement and more like the earlier waves of computers and the internet changing how work gets done.

That is why I keep coming back to this point: stop trying to make replacement happen. It is not happening in the simple, dramatic way many AI narratives suggest.

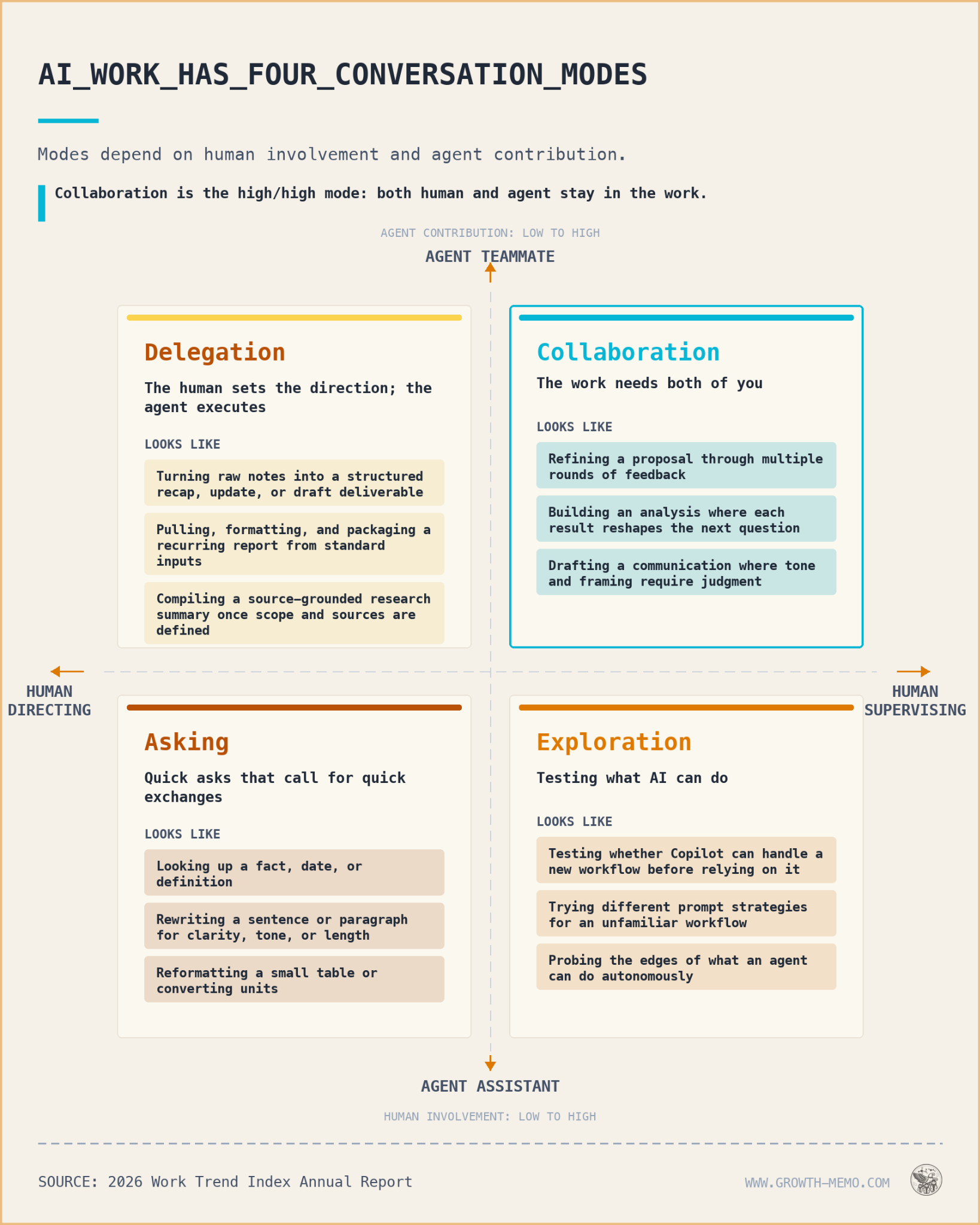

AI is powerful, but it is also inconsistent. In its current form, it can do some tasks better than humans and fail badly at others. That paradox is often called the Jagged Frontier.

The Jagged Frontier idea matters because it explains why some people see AI as transformative while others remain lukewarm. A BCG and Harvard study of 758 knowledge workers found that people get the most value from AI when they understand what it is good at and where it breaks down.

Microsoft reached a similar conclusion in its 2026 Work Trend Index Annual Report. The company found that a small group of advanced AI users, described as Frontier Professionals, were not simply using AI more often. They also knew which mode of AI use fit each task.

That distinction is important. The best AI users are not handing everything over blindly. They are applying judgment. They know when to use AI as a helper, when to use it as a collaborator, when to use agents for multi-step workflows, and when to keep a human firmly in control.

I still do not trust most AI workflows enough to leave them running with no maintenance, review, or quality assurance. The question I ask is simple: would I bet my brand, customer experience, or revenue on a fully automated workflow with no human oversight?

Klarna is a useful warning here. The company publicly promoted the idea that AI was doing the work of hundreds of agents and helping reduce headcount. Later, it reversed course and rehired humans after leadership acknowledged that aggressive cost-cutting had lowered quality and that customers still wanted a human option.

That is the tradeoff I see with substitution positioning. It creates immediate attention, but it can damage long-term credibility. The words often do not match the operational reality.

Replacement positioning could work if customers truly wanted full replacement and if the technology were consistently ready for it. I do not think either condition is true.

Cost reduction is a strong AI argument because it shows up quickly on the P&L. Productivity gains usually take longer. They build inside companies over time and often take even longer to appear across the broader economy.

But when replacement positioning goes beyond cost-cutting and becomes people-cutting, I believe it starts to antagonize the very people companies need to win over.

We have already seen backlash. Duolingo’s AI-first memo drew heavy criticism before the company reframed AI as a tool to accelerate work rather than replace contractors. Surveys have found that some workers refuse to use AI tools because they fear job loss. Pew has reported that many U.S. adults are more concerned than excited about AI in daily life. Reuters/Ipsos polling has shown widespread fear that AI will permanently displace workers.

There is also a quality problem. When employees believe the purpose of AI is to replace them, they may disengage or produce lower-quality work. In my view, that is not just an adoption issue. It is a positioning failure.

Executives often feel more excited about AI than the employees asked to use it every day. That gap matters. If leadership talks about AI as a replacement engine, employees hear a threat. If leadership talks about AI as leverage, employees have a reason to learn.

Token economics also complicate the replacement story. Some companies have bragged about massive AI usage, but token costs are still a real business variable. As those costs normalize, the math may make junior employees look interesting again, especially when human judgment, context, and accountability are part of the output.

So what should replace replacement? I think the answer is enhancement. Instead of positioning AI as a way to remove people, I would position it as a way to make capable people more effective.

AI can be used in two broad ways. A company can try to reduce the number of people, or it can grow output with the same number of people. The data I have seen suggests that productivity gains often create the stronger return.

A National Bureau of Economic Research paper surveyed 750 executives about AI’s impact on productivity and labor markets. Larger firms showed more interest in replacing labor costs, but the highest ROI came from productivity growth.

That is the lesson I take from the research: doing more with the talent you already have is often stronger than trying to remove the talent that knows what good work looks like.

Building products has become easier, but distribution has not. When supply explodes, the scarce thing is not output. The scarce thing is being the product, brand, or service that actually gets chosen.

That is why positioning matters more than ever. Product quality still matters, but the way I frame AI use can determine whether people see it as empowering or threatening.

My takeaway is simple: I would stop selling AI as a people replacement. I would sell it as judgment leverage, workflow acceleration, and creative expansion. Fear can get attention, but empowerment is a better long-term strategy.

This post first appeared on the author’s website and is republished here with permission.

In today’s fast-paced digital world, I’m constantly amazed at how AI is reshaping SEO dynamics. With AI taking over more execution, I’ve realized that enhancing skills in interpretation, prioritization, and performance analysis is key to staying ahead.

The rapid pace of platform changes, AI-driven search engine results pages (SERPs), and evolving measurement models means I must frequently reassess my skill set as a search and performance marketer.

What was effective just six months ago might be obsolete today. This constant evolution is why continuous learning has become essential for SEO performance. Organizations that excel are those that integrate learning into their everyday practices — testing, sharing knowledge, and making informed decisions.

Why Search and Performance Marketing Skills Quickly Expire

I’ve experienced firsthand how search skills can become outdated quicker than expected. In meetings, I’ve seen strategies from 18 months ago falter and work against performance rather than enhance it.

Frequent platform updates, changes in automation, and shifts in user behavior can render once-effective tactics obsolete. Without ongoing learning, I realized how easy it is to fall behind on current best practices.

Misreading data or over-relying on automation can weaken results. To keep up, I must adapt to changes in AI overviews, SEO features, and zero-click experiences.

… [Content continues in a similar manner ensuring first-person narrative and SEO-friendly structure] …

Continuous Learning is Now Part of Performance

As AI propels the pace of change in SEO, I see how critical it is to evolve skills swiftly and rely on sharp judgment, adaptation, and strategic decision-making.

Falling behind often isn’t about lacking tools or data. It’s about clinging to outdated knowledge that no longer mirrors the present SEO landscape.

The leading SEO professionals remain curious, embrace learning, and are always ready to adapt to the evolving digital landscape.

From February to May 2026, I dove deep into the fascinating world of agentic AI adoption. I explored how it’s being embraced by enterprises, mid-market players, and SMBs across the U.S. and worldwide. By gathering insights from top consulting firms like McKinsey, Gartner, and IDC, as well as academic institutions and AI leaders, I pieced together a comprehensive overview of agentic AI’s current landscape.

This report fuses insights from over 30 research efforts and industry surveys, covering 15,000+ businesses. It provides a granular look into how businesses are integrating autonomous AI agents this year, breaking it down by company size, industry, deployment stage, primary use cases, and adoption and abandonment patterns.

*Statistics are based on data up to May 14, 2026, unless indicated otherwise.

While generative AI generates immediate outputs, agentic AI shifts the way systems function entirely. This piece zeroes in on agentic AI’s adoption, defined as follows:

Agentic AI revolves around AI systems autonomously planning, deciding, and executing complex tasks from beginning to end.

The term adoption signifies any case where an organization uses at least one agentic AI system at any stage, from initial trials to full-scale implementation.

Meanwhile, abandonment involves halting an agentic AI program or specific projects. This doesn’t always mean closing an organization’s entire AI operations, as they might continue other initiatives.

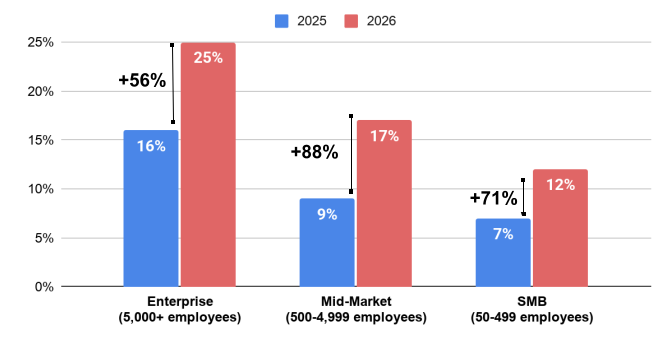

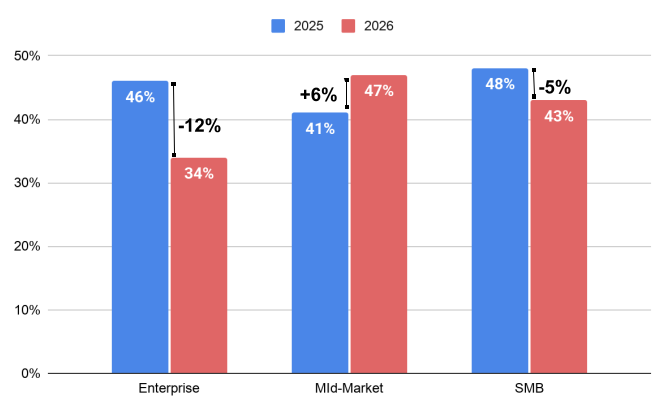

Agentic AI adoption significantly varies by organization size. A breakdown of recent adoption rates across different segments unveils fascinating trends.

As I dug into the data, I discovered enterprises are leading the way with 25% adoption, thanks to their resources and AI budgets. However, smaller sectors, like mid-market firms and SMBs, are catching up fast. Their year-on-year growth rates are even outpacing those of enterprises!

I predict that SMBs and mid-markets will continue adopting agentic AI faster than their larger counterparts. This trend is partly driven by accessible solutions such as Salesforce Agentforce and Microsoft Copilot Studio, which empower companies with tighter budgets. In contrast, enterprises face challenges due to their intricate systems and diverse data environments.

Agentic AI deployment spans various maturity stages, presenting unique challenges depending on available resources. For SMBs, scaling can be costly, making it particularly challenging.

The table showcases deployment stages among adopters, revealing that 62% of enterprises, despite higher resources, linger in the experimentation phase. Notably, only 13% achieve full deployment.

A few patterns stand out from the data:

Firstly, experimentation predominates across sizes, with a 56% average gap to partial deployment. This highlights caution across sectors in deploying agentic AI.

Despite enterprises’ resources, mid-market companies are seeing greater partial deployment rates, likely due to fewer approval bottlenecks and more budgetary leeway compared to SMBs.

Also, scaling correlates with resources. Enterprises, despite early-stage phases, manage full-scale deployment at rates double those of mid-markets.

These patterns reveal that most organizations are still exploring, with few transitioning to production deployment.

It’s not all smooth sailing. According to Gartner, around 40% of agentic AI projects might be canceled by 2027, due to challenges encountered during deployment.

Although abandonment rates generally decline over time, mid-markets still see higher rates due to their broader range of obstacles and fewer resources compared to large enterprises.

Summarizing the common reasons for project failures:

Data quality matters. Without quality data, agents struggle, highlighting a universal need for centralized and uniform data pre-deployment.

Clear expectations are vital. Projects without well-defined success criteria often fail to demonstrate value, risking cuts in resources when results are inconspicuous.

Costs weigh heavily on SMBs. For SMBs, financial constraints dominate abandonment reasons, overshadowing other factors. Mid-market firms display more varied primary drivers.

Such insights explain why full implementation is elusive for many, despite significant investments. Companies need to address multiple challenges concurrently to progress beyond experimentation.

On an industry level, exploring adoption across sectors shows where agentic AI thrives and lags. Regulatory factors, data readiness, and competitive dynamics result in differing adoption levels.

Industries like education, construction, and real estate lag, owing to budget constraints, less advanced data infrastructures, and fewer automation opportunities. Nonetheless, even these sectors demonstrate notable enterprise adoption, signaling a broader reach beyond tech and financial services.

Finally, examining use cases underscores where agentic AI is making headway. Customer service and supply chain coordination rank high due to their structured processes. On the other hand, finance sees lower adoption due to stringent regulatory scrutiny.

If you fancy obtaining a PDF copy of this insightful report or learning more about our work, feel free to reach out here.

For further exploration into agentic AI and its surrounding trends, consider delving into the following reads: